Centrica shares plumb depths as review may unearth nasties

Updated 1600 GMT Centrica shares hit their lowest levels in more than five years after adjusted full-year operating profit came in 35% lower. Its new […]

Updated 1600 GMT Centrica shares hit their lowest levels in more than five years after adjusted full-year operating profit came in 35% lower. Its new […]

Updated 1600 GMT

Centrica shares hit their lowest levels in more than five years after adjusted full-year operating profit came in 35% lower.

Its new CEO today attempted to draw a line under the gas giant’s recent missteps, but the company still faces an uncertain year, at least, so safety-seeking investors sold the stock hard.

The consumer-to-wholesale-energy provider which is also a downstream exploration & production company has been hit by the multiple whammies of crude oil price collapse, increasing regulatory restrictions, legal penalties, and others.

A profit warning by Britain’s largest utility company in November, triggered by weaker commodity prices, lower nuclear output and warmer-than-usual weather, was followed by a fine of £11.1m against its retail arm in December, for missed environmental targets.

In November, the firm had cut forecast FY earnings per share to 19p-20p from 21p-22p.

In the event the full-year EPS came in at the lower end of that range, with Centrica reporting 19.2p.

These and a number of other misfortunes contributed to a 35% fall in adjusted operating profit for 2014 and have forced the British Gas owner to announce a series of moves aimed at shoring up its business which is looking increasingly beleaguered.

The dividend cut was “to make sure the company has a solid credit rating going forward,” Conn told reporters on Thursday.

There was “no certainty” oil prices would rebound to previous highs, said Conn, the former head of marketing and refining at BP.

However, during a conference call with investors, he suggested Centrica was unlikely to need to cut its dividend again, after it completed the planned strategic review of the business by July.

Centrica said the review would specifically look at:

In conjunction with the CEO’s comment that dividends are unlikely to require further cuts, there is more than a suggestion that the outcome of Centrica’s review could lead it to decide to continue attempts to dispose of the non-core assets mentioned above, and perhaps others.

Segments like Centrica Storage Ltd.—which operates the Rough gas storage facility in the North Sea and the Easington onshore gas processing terminal in East Yorkshire—could be on the block.

Storage contributed just 0.7% of the group’s total revenue in 2013.

Simple estimates suggest the facilities could fetch between £2.2bn-to-£3bn and perhaps more, if Centrica agreed to lease back the facilities to accommodate its own storage needs.

On the issue of operating capability and efficiency, Centrica will at some point have to address the situation of inactive assets, including Accord Energy Trading, which has been a ‘dormant’ business since the end of 2013.

Centrica rolled its energy trading activities into new subsidiaries under the Centrica Energy umbrella in 2011, but the Accord shell still carries liabilities of £23.2m, according to filings published by financial data provider DueDil.com.

There’s no way of telling whether such essentially ‘off-balance sheet’ entities will inevitably lead to write-downs (AKA written-off losses) but such uncertainties are unlikely to be tolerated by shareholders for much longer.

Sorting out such loose ends may eventually enable Centrica to improve its Return on Assets (ROA, a gauge of capital efficiency) from a meagre 3% on a trailing 12-month basis.

Centrica’s ROA places it close to severely regulated water utilities like Severn Trent, but below their peers Pennon, which managed 4%, and United Utilities at 7.1%.

The most immediate issue is that whilst pay-out cuts were in all probability unavoidable, annual dividends—yielding an impressive 6.79% at last tally, might well have been the bulk of Centrica’s buy case for many investors.

Today’s announcements suggest pay-outs will effectively be cut in half eventually—sending Centrica to the bottom of its European regulated utilities group on yield.

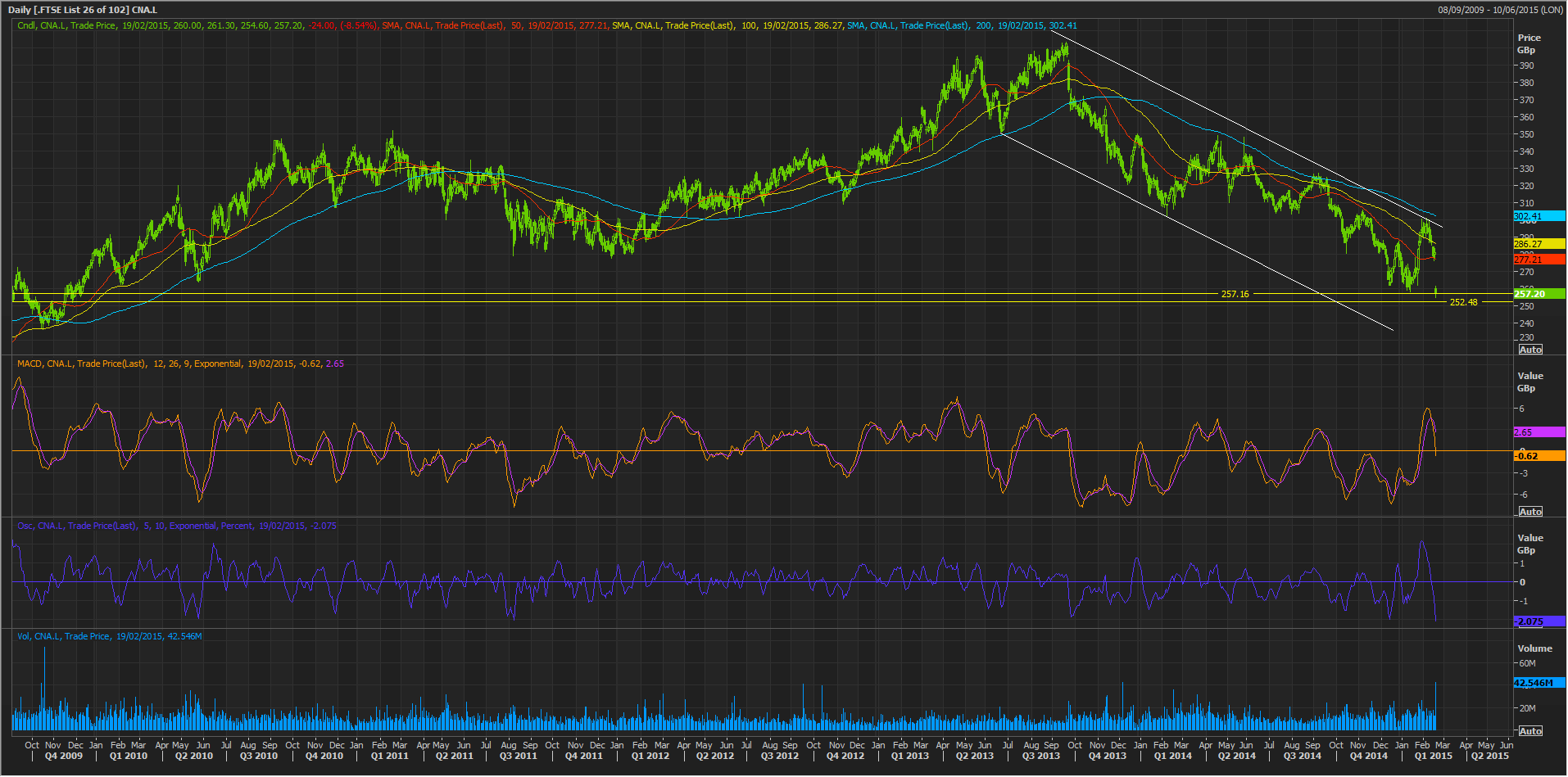

With the shares skirting a 10% loss for most of the Thursday, the market has made its view of the cut clear.

The current half-decade low in the stock would carry an implicit measure of support, even if there seems to be ample slack in downside momentum.

But continued reductions by shareholders in the medium term seem likely, before Centrica’s intrinsic strengths reassert themselves, probably after the strategic review is published in July.

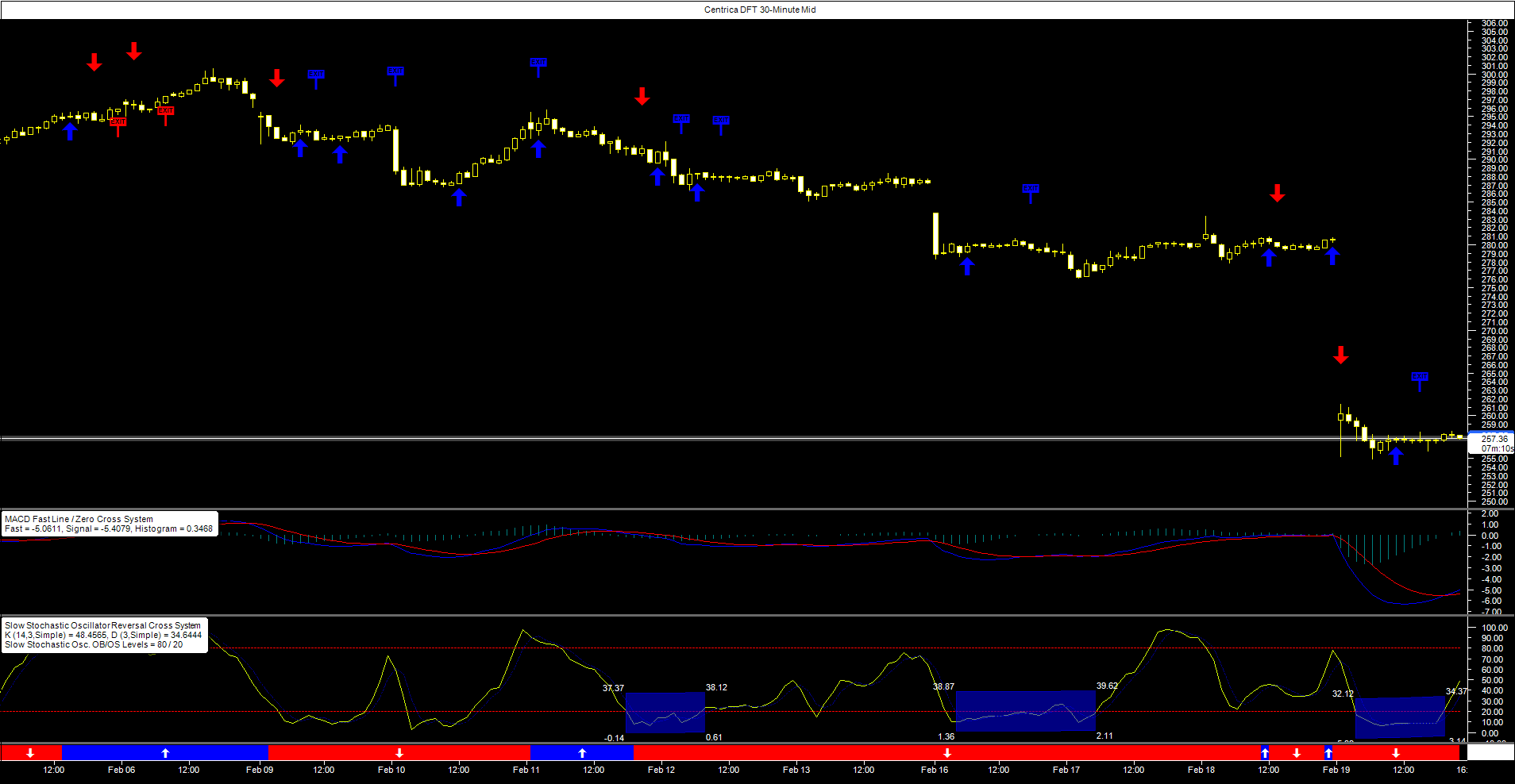

For the even shorter-term, the sell-off is predictably overdone for the moment, as can be seen in a half-hourly view of Centrica Daily Funded Trade offered by City Index.

Strictly speaking, our Slow Stochastic Reversal Cross system is right to have triggered a long entry earlier on Thursday afternoon, as it diligently applies classic stochastic concepts.

That meant an ‘exit’ from the long was signalled not too long afterwards, since classically, it’s time to close when the slow moving average (blue line) crosses below the fast one (yellow).