Centamin share spike comes at a high price

Centamin Plc. was top performer on London’s main market for most of Monday, after a surprise move that made it the best dividend payer among UK-listed […]

Centamin Plc. was top performer on London’s main market for most of Monday, after a surprise move that made it the best dividend payer among UK-listed […]

Centamin Plc. was top performer on London’s main market for most of Monday, after a surprise move that made it the best dividend payer among UK-listed gold miners.

The 29% fall in full-year core earnings was disappointing, but obviously well trailed, given the commodity (‘spot’) gold price remains about 40% lower than its 2011 peak.

It’s also a given that Centamin, like all miners of any scale in recent years, has been attempting to combat falling materials prices by fiercely removing production costs.

It reached an inflection point at the third-quarter mark in November last year, when it said it managed to squeeze out 10% more production year-on-year despite a 1.5% tick down in cash cost.

Centamin shares rallied 60% from that date to late January this year.

But the stock then subsequently went on to lose about half of that amount up until Friday’s close as investors increasingly wondered what its strategy for growth would be, having removed, on a net basis, probably as much cost as practically possible for the foreseeable future.

Investors got an answer today—Centamin has basically ended capital project development for the foreseeable future.

Full-year production cash cost in 2014 was revealed today to be $729 per ounce, but with key guidance for 2015 all-in-sustaining cost (AISC) of US$950/oz. margins remain precarious, with spot gold at $1142/oz. and still in a monthly down trend.

It’s therefore worth querying how Centamin intends to fund the policy it announced today that would see it return about 15%-30% of its free cash flow to shareholders.

(Note the policy would appear to give Centamin a notional yield of about 3.6% compared to essentially zero on average from its peer group.)

Centamin has $162.8m in cash, it said today.

It also had “bullion on hand, gold sales receivables and available-for-sale financial assets as at 31 December 2014”, the company announced on Monday.

Even so nominal coverage of just 5.31 times the pay-out for 2014 would exhaust the current net cash position, even under the generous assumption that dividends don’t rise from the $0.0286 per share for this year.

Perhaps on that basis it’s therefore little surprise that Centamin also backed today’s dividend policy announcement by stating that “No capital expenditure for expansion or project development is planned for 2015”.

That would leave sustaining and expansion capex at an average $100m per annum, with no more than $30m of that allocated to its main Sukari asset in Egypt.

Net cash could then feasibly sustain the current dividend policy, if (perhaps the biggest ‘if’, under current circumstances) gold at least managed not to depreciate any further than approximate spot prices.

Growth would remain another question entirely.

There is even less margin for error in this scenario than the foregoing suggests.

The Egyptian state and others on whom Centamin is reliant due to its prospects being located in their countries have been demanding a share of net cash that is forecast to break the £100m level by the end of the 2015 financial year.

In short, there is little margin for anything at Centamin.

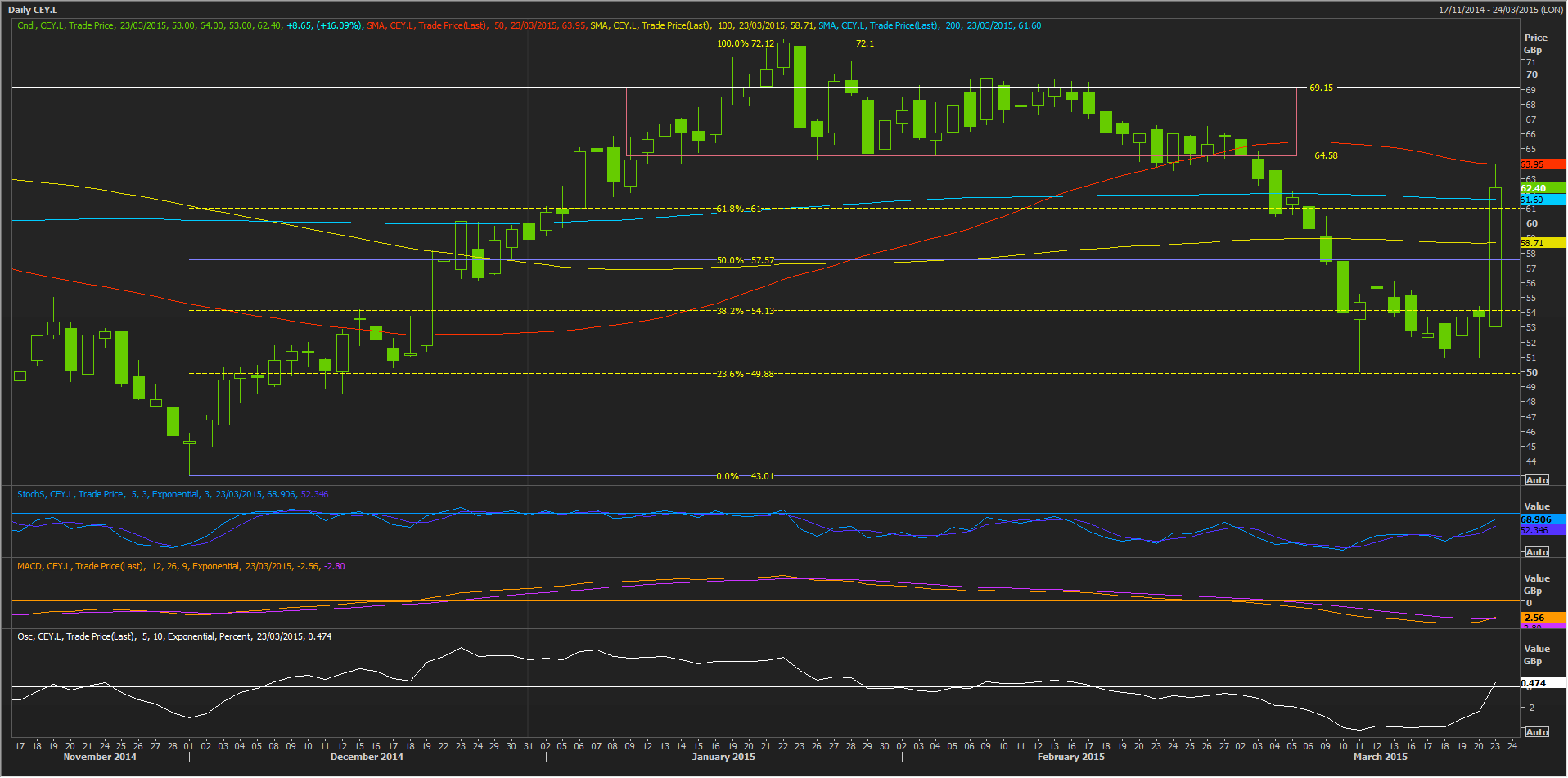

Whilst all the above logically doesn’t preclude the share heading back to the c.72p highs achieved in January—the shares will need to wade through the pivot area between 64.58p and 69.15p that presented such a challenge in the run-up.

A stalling of the share price progress made today could find a confluence of support at the 200-day moving average and an important retracement mark based on 1st December low, or it would face the same region as resistance, if support were to give.

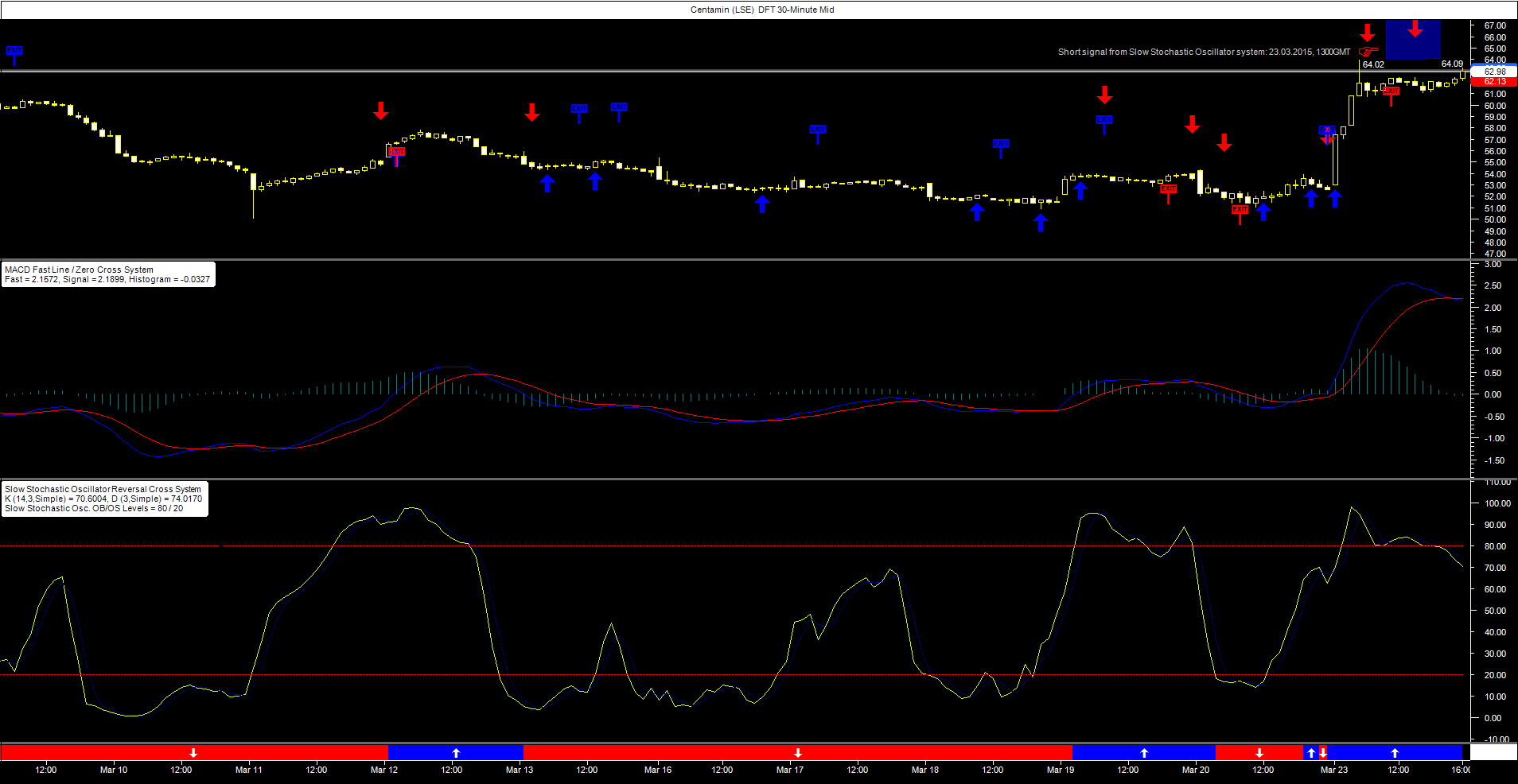

In the nearer term, we note some moderate divergence between momentum measured by the slow stochastic oscillator and the trade level of Centamin Daily Funded Trade offered by City Index.

A trading system based on this indicator issued a short sell signal due to the ‘overbought’ state of the title at the time.

Though as the stochastic moving averages are now back within the system’s prescribed boundaries, the likelihood that a near-term exit from the short trade could be triggered–when the ‘slower’ (blue) line crosses below the ‘faster’ yellow line–has increased.