Carney Hands off as GBP Nears 1 60

Fresh 9-month lows in the UK unemployment rate were not enough to boost average earnings (pay), but continue to convince bond traders in pushing up […]

Fresh 9-month lows in the UK unemployment rate were not enough to boost average earnings (pay), but continue to convince bond traders in pushing up […]

Fresh 9-month lows in the UK unemployment rate were not enough to boost average earnings (pay), but continue to convince bond traders in pushing up market rates even as the Bank of England insists on containing its base rate at 0.50% for another 2 years.

Sterling hits 7-month highs against the USD and 8-month highs in trade-weighted index (calculated by the BoE).

Unlike previous episodes of pronounced strength when the currency was boosted by a general advance in risk-on dynamics (robust market optimism, improved growth in G5 and BRICS) the current phase of sterling rally is primarily driven by UK-specific factors across manufacturing, construction and services sectors. The marked improvement in labour markets fails to have any notable impact on wages but maintains market rates at 2-year highs.

Sterling is now the best performing currency among the 11 most actively traded currencies over the last 6 months, rising 5.8% against the US dollar, and hitting 4year highs against the yen.

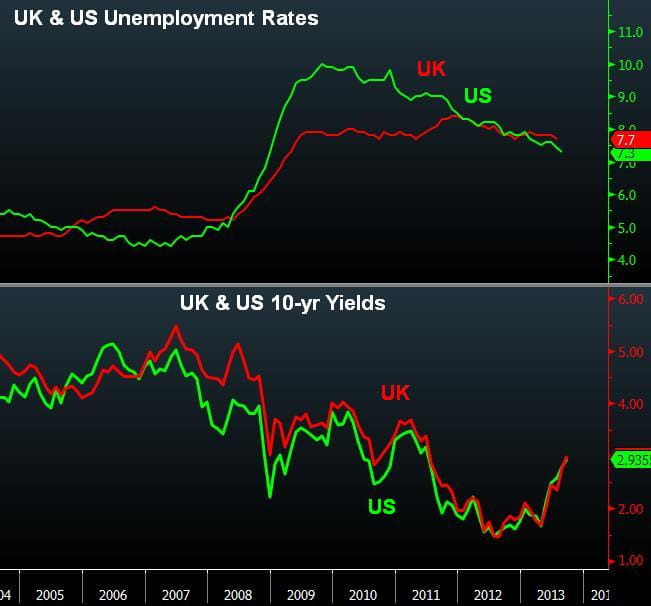

The UK unemployment rate (ILO measure) fell to 7.7%, hitting its lowest level since November, which also matched the lows in April 2011, September 2009 and May 2009. The ONS’ claimant count unemployment rate hit 4.2%, its lowest level since February 2009. Jobless claims fell by 32,600, marking the 10th straight monthly decline and accumulating a net decline of 177,000 in unemployment claims since November. But the 3-month average of weekly earnings fell to a 4-month low of 1.1% y/y from 2.2%.

Yields on 10-year gilts hit a fresh 2-year high at 3.05%, or 0.06% above their US counterparts, the highest differential in 6 months.

GBP also Boosted by Britain’s Isolation

So far, the market implications of a strike on Syria have been generally binary; whereby a looming attack weighs on equities, risk currencies (primarily the euro) to the benefit of the US dollar. Sterling has been spared from the sell-off in risk currencies due to Britain’s isolation from the crisis following the anti-strike vote in British Parliament. The positive impact on USD from a looming strike stems from the equities-currencies chain of reaction.

Combining next week’s FOMC decision of asset purchases into the Syria equation, the US dollar may be in for further losses on the following rationale: The threat of an immediate strike on Syria is averted and the Fed announces a maximum reduction of $10 bln in bond purchases, an outcome that is well priced in the market. Thus, anything less than $10 bn may be deemed as dovish and USD-negative. There is also the possibility that the Fed will use next week’s FOMC meeting to announce a tapering in October or December.

GBPUSD’s path to $1.60 appears increasingly viable after the rate has breached above the 100 and 200-week moving averages, while remaining supported above the trendline from the July lows. Tomorrow’s speech from BoE governor Carney, next week’s FOMC decision as well as the release of the MPC minutes should lead to volatility (noise), serving as an entry possibility to ride further gains towards $1.60, followed by $1.6220.