Can the bond market predict when the equity rally will come to an end

2017 has been a mixed year for the dollar. After peaking in December, it is 300 pips off of its highs, and it is worst […]

2017 has been a mixed year for the dollar. After peaking in December, it is 300 pips off of its highs, and it is worst […]

2017 has been a mixed year for the dollar. After peaking in December, it is 300 pips off of its highs, and it is worst performer so far this year versus the other G10 currencies. The Trump reflation trade seems to have stalled for the greenback, and understanding the reason for this could give an interesting perspective on the ongoing rally in the equity market.

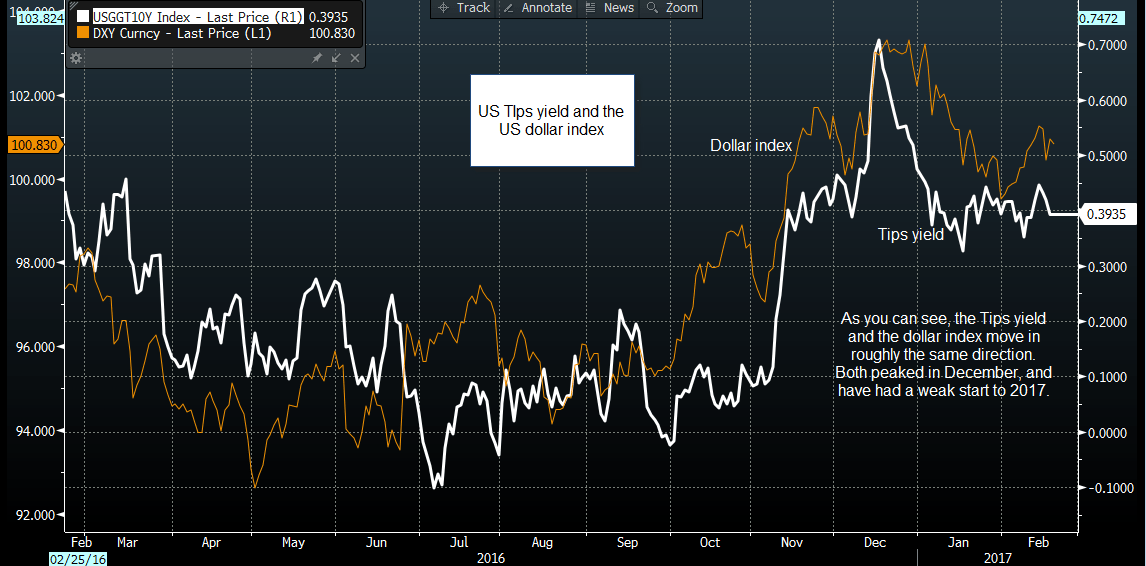

The chart below shows the 10-year US Treasury Inflation Protected (TIPS) bond yield and the dollar index; as you can see, the two generally move in the same direction. The TIPS yield has fallen dramatically as bond investors are slow to price in Fed rate hikes even though the inflation rate is rising.

Why Trump’s tail is wagging the Fed’s dog

So, why is the bond market slow to price in the prospect of a rate rise, even though the Fed chair Janet Yellen was considered hawkish during her testimony to Congress last week? The reason could be Donald Trump. The US Federal Reserve has been pushed into a corner by President Trump’s promises to boost fiscal spending and overhaul the US tax system. If he does this, then logic would suggest that inflation should rise and the Fed should hike interest rates, however, what if Trump fails to deliver? If the big Trump reflation story turns out to be a myth then the Fed is likely to back away from rate increases later this year. The bond market is currently having to deal with an unusual set of circumstances: Trump’s tail is wagging the Fed’s dog.

Bond market scepticism:

There is a divergence in the markets’ attitude towards Trump’s economic plan. While the equity market is still hopeful that Trump can cut corporate taxes and boost fiscal spending, the FX and Treasury markets seem more sceptical. Reports that House Republicans are divided on the issue of the border tax – or import tax – which is necessary to fund a planned corporation tax cut, has left bond and FX investors in some doubt as to whether a deal will be passed, and if the tremendous fiscal spending Trump keeps banging on about will ever come to fruition. However, the irony is that this scepticism is weighing on bond yields, and the low cost of capital is also driving the equity market higher.

So what can the fall in bond yields tell us?

We think this is one of the key reasons that volatility has been subdued of late, even while chaos reigns in the Trump administration. The Vix may have broken its three week streak of closing the week under 11, however at 11.5 it is still subdued. This is mostly due to the low level of bond yields, in our view, which, as mentioned above, are helping to drive this rally in equities.

Equity traders should watch yields

This means that where bond yields go next could be a key driver of equity prices. There are two potential outcomes:

If Trump fails to deliver on his economic promises, a short, sharp sell-off is to be expected, however, this makes it more likely that bond yields will remain low and interest rates won’t rise, which could cushion the fall.

Figure 1:

Source: City Index and Bloomberg