Can rate expectations continue to fuel this GBP rally

This question has now come centre stage for financial markets after Bank of England governor Mark Carney said that interest rates could rise at the […]

This question has now come centre stage for financial markets after Bank of England governor Mark Carney said that interest rates could rise at the […]

This question has now come centre stage for financial markets after Bank of England governor Mark Carney said that interest rates could rise at the “turn of the year”, which suggests that a rate rise is likely in December or January, it could even come earlier if the Bank wants to hike rates at the same time as the November Inflation Report.

Looking for a winter rate hike

This week has seen a sharp re-pricing of the market’s expectation of interest rates for the UK. On Tuesday BOE Governor Mark Carney said that the timing of a rate rise was close, he then followed this up by saying that rates could rise this winter at a speech on Thursday night. The pound has duly reacted to Carney’s “hawkish” stance this week, and GBP is the second strongest performer in the G10 FX space on Friday morning, just behind the kiwi.

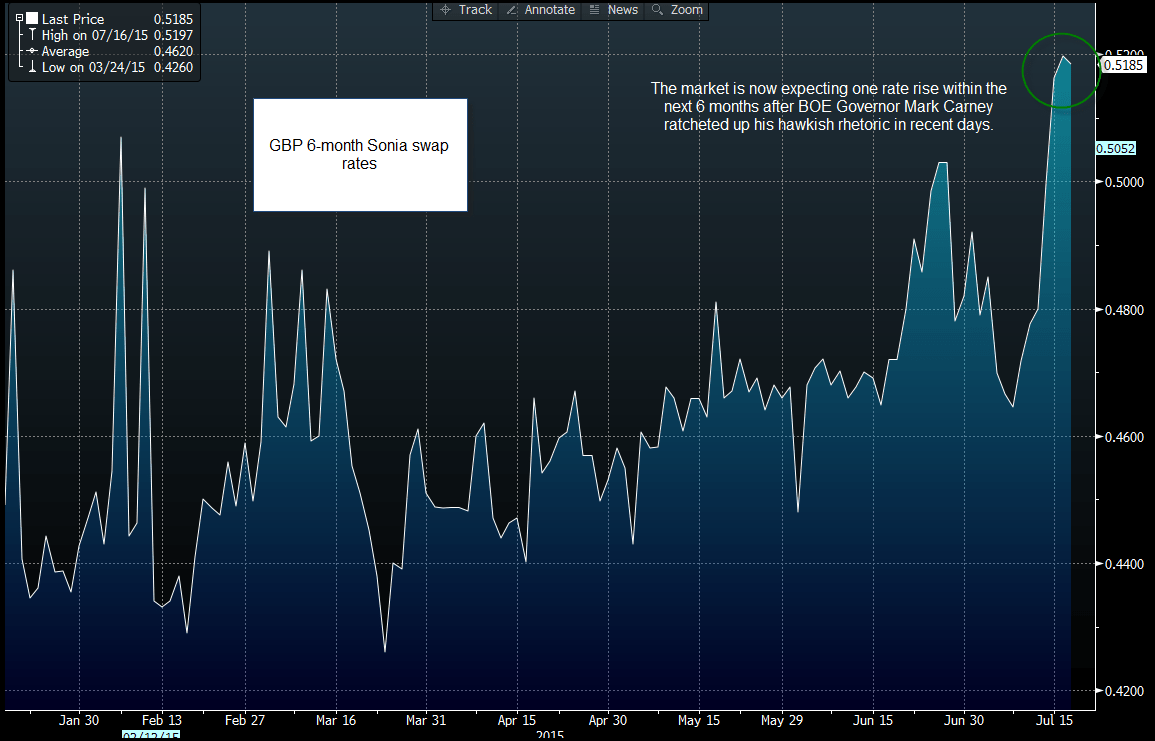

The market is now pricing in one 25 bp rate hike in 6-months’ time (according to Sonia GBP swap rates). The yield on the 6-month Sonia contract is now 51 basis points, its highest level all year (see figure 1). So, after months of uncertainty about when rates would rise, it now looks like some central bankers are willing to put their necks’ on the line and say that rates need to rise, and they will do so relatively soon.

Safety in numbers:

Two events may have fuelled the timing of Carney’s hawkish rhetoric this week: 1, the sharp pick-up in wage growth for May, and 2, hawkish sentiments from the Fed governor Janet Yellen in recent days. Nobody wants to be the first to do something as “drastic” as hike interest rates after a prolonged dovish cycle, so Carney may have felt strength in numbers now that the Federal Reserve is also touting a 2015 rate hike.

Interestingly, both Janet Yellen and Mark Carney both mentioned rate hikes even though the global economic backdrop was shaky. Greece still hadn’t secured a third bailout and a Chinese economic slowdown had caused havoc with Asian stock markets.

So why now?

Both Yellen and Carney appear to be of the view that there will never be a perfect time to hike rates, so they may as well go for it. Importantly, both central bank heads also noted that if they don’t start to hike rates soon then they may have to hike at a faster pace than they would like down the line, which could cause more dislocation in financial markets. They both also stressed the slow pace of rate hikes and the fact that rates may not return to pre-crisis levels of approx. 4.5% (according to Carney), during this rate-hiking cycle, so maybe he wasn’t that hawkish after all?

The FX market is more sensitive to Carney

So far, financial markets have taken it in their stride, and both the FTSE 100 and S&P 500 are set to close higher on the week. Overall, stocks have been more sensitive to events in Greece and earnings season rather than the prospect of a single rate rise in the coming months. It is the FX market that has run the furthest with the Yellen/ Carney comments, and even the bond market’s reaction looks fairly muted in comparison.

The pound rose to a 7.5 year high vs. the EUR on the back of this news, and GBPJPY is close to its highest level since 2008. But can the prospect of one rate hike, and a significantly slower rate-hiking cycle than in the past be enough to sustain broad GBP strength?

We think that in the short term some adjustment in the pound was needed as Sonia rates surged to multi-month highs. However, unless we see a sharp rise in economic data, particularly inflation and wage data, then we think that this rally could lose some steam and it may be disadvantageous to go long GBP at these levels.

The technical view:

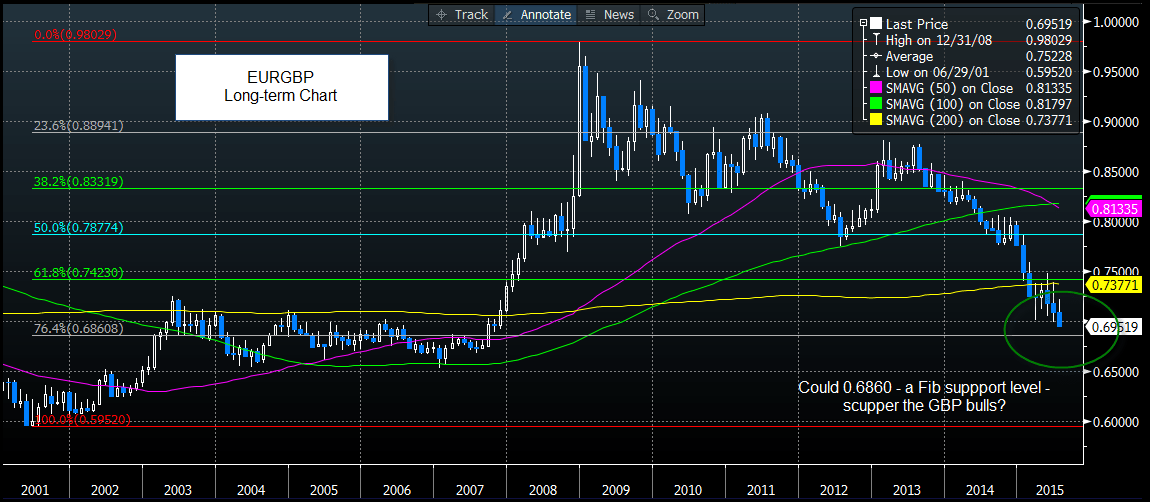

Interestingly, EURGBP is approaching a support level worth noting (see fig 2). EURGBP is close to the 76.4% retracement of the uptrend from 2001 until its peak in 2008, which comes in at 0.6860. Although this is not the most significant of Fibonacci levels, investors may take note of it due to the historical nature of EURGBP’s current level, if we do get to this level it may attract some EUR buying interest.

GBPJPY could also find the June high of 195.85 acts as a sticky level of resistance in the coming days and weeks. Unless we get another bout of even more hawkish BOE rhetoric, or even better economic data, then the market may have already priced in the prospect of a rate hike, which leaves sterling crosses vulnerable to some selling in the short term as they currently look extremely stretched to the upside.

Takeaway:

Figure 1:

Source: FOREX.com, Data: Bloomberg

Figure 2:

Source: FOREX.com, Data: Bloomberg