Burberry shares slip on weak Asia sales FX

Burberry sales in the last half of its financial year slightly exceeded expectations with help from the US and Europe, where revived trading helped to […]

Burberry sales in the last half of its financial year slightly exceeded expectations with help from the US and Europe, where revived trading helped to […]

Burberry sales in the last half of its financial year slightly exceeded expectations with help from the US and Europe, where revived trading helped to offset continuing weakness in major markets like Hong Kong.

The British luxury fashion firm said on Wednesday second-half underlying sales were 9% higher than at the same time last year, and total revenue in the 6 months to 31st March was £1.423bn.

Analysts on average had expected half-year revenues to be £1.39bn, according to a consensus compiled by Thomson Reuters

Like-for-like sales growth in the fourth quarter was up 9% on the same quarter a year ago, in line with my forecast, and ticking one percentage point higher than Q3.

However, not everything was pretty in Burberry’s last trading period of 2014/15.

The low-single digit growth seen in Asia Pacific in the third quarter continued, “with further deceleration in Hong Kong”, the company said.

The years in which Burberry benefited from the above-average spending power of wealthy Asian, especially Chinese, customers, seem to be in the past, amid a raft of pressures including a slowdown in China exacerbated by an official clampdown on real or perceived graft and ‘excess’.

Plus most recently, weak demand in Hong Kong has followed disruptions from protests.

“We anticipate external challenges will continue in the current year,” said Burberry CEO Christopher Bailey, noting that the company had performed strongly in an “uncertain” environment.

One move Burberry announced this morning aimed at curbing that uncertainty was the termination of its long-time licensee agreement in Japan.

This will allow it to bring the business in the country in-house, but the impact on specific licensing revenues in 2016 could be as much as 40%, it warned this morning.

Even so, Burberry’s Licensing business constituted just 4% of total revenues in the company’s full-year that ended in 2014.

So the expected decline in sales from the business (probably temporary) is unlikely to be material to overall revenues.

A potentially more serious headwind for Burberry is the impact from foreign exchange translation effects.

The firm expects retail and wholesale profit for the full current year to be about £25m lower than it would have been at the previous year’s exchange rates.

Burberry in July had reiterated a warning initially sounded in May about about currency headwinds.

However, this morning it looks like the firm has moderated the effect of the total hit to Licensing and Retail of £65m guided in July.

Even assuming Licensing revenues fall 100% this year (from FX and going in-house combined) the foreign exchange impact Burberry forecast last summer is no longer expected to be so severe.

Using constant-currency rates, for fiscal 2016, Burberry expects this reported retail and wholesale profit to be about £50m higher year-on-year.

Wholesale revenues are forecast to stay unchanged in the first half 2016, with sales from its closely watched Beauty segment up by double digits after rising 10% in H2 2015.

A burgeoning market for ‘luxury arbitrage’ has recently given Burberry, and European rivals like LVMH and Patek Philippe, a further headache.

It involves global travellers taking advantage of a large price gap between products sold in Europe and Asia because of the weakened euro.

Such firms have the choice of either raising their product prices in lower-priced regions, like Europe, or lowering prices in more expensively priced places like China.

Chanel earlier this month raised some of its prices in Europe, while slashing them in China,

TAG Heuer said it would cut prices in China.

Obviously, any price cuts will be scrutinised closely by investors, especially amid anecdotal evidence that there is a larger price gaps between Europe and China for Burberry compared with brands like Cartier and Louis Vuitton.

All in, Burberry has unveiled solid trading this morning.

But the combined net effect of the real and potential threats of FX, the Licensing blip, and possible price cuts have given the market pause for thought.

That Burberry’s stock is still sitting on the bulk of its 32% net gain since October, and is little more than 6% off its all-time high, is further cause for caution.

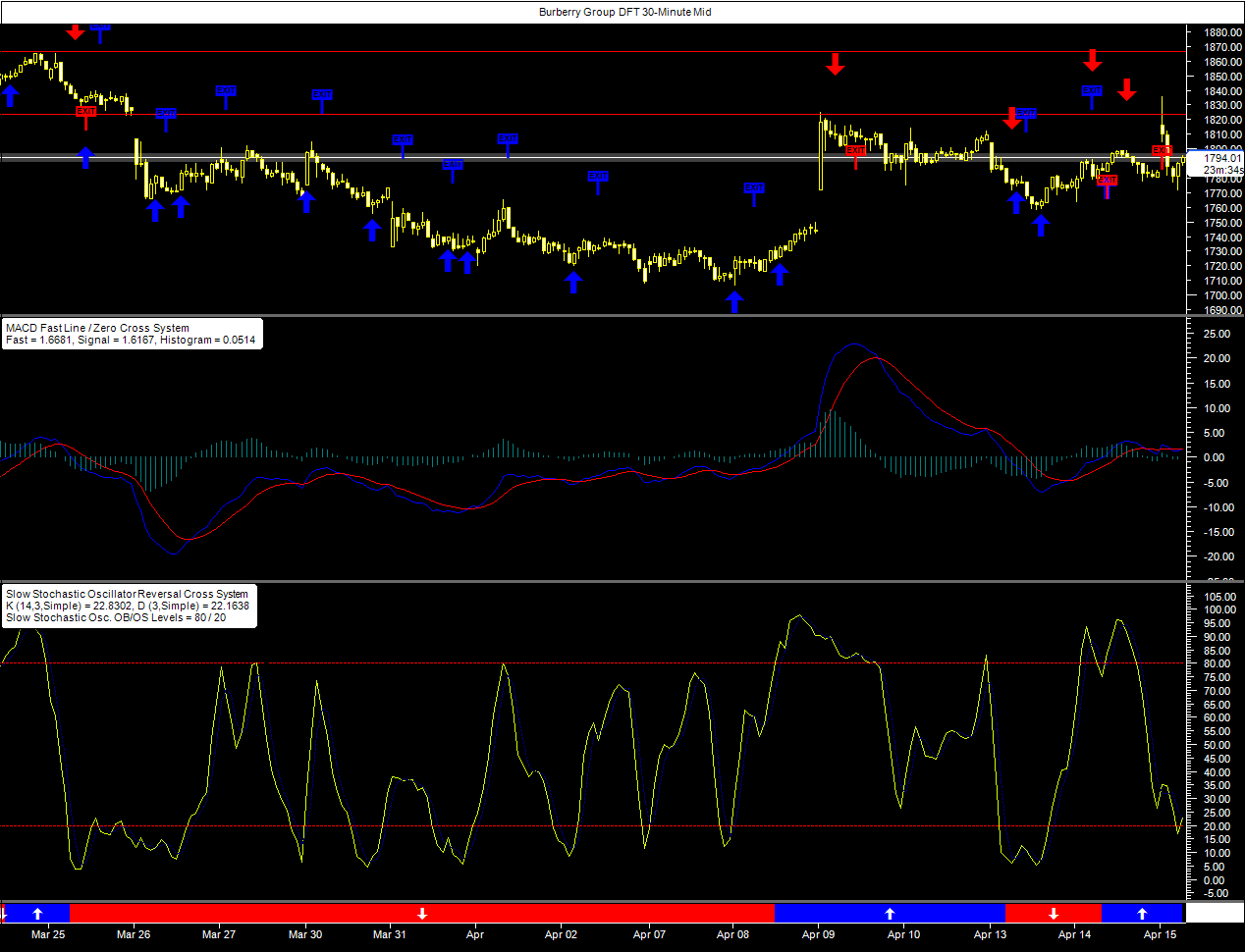

In the meantime, City Index’s Burberry Daily Funded Trade in a half-hourly timeframe has exhausted the short-term downside and the title is oversold and may bounce.

However, the trade is currently being challenged by a clear pivot line at the approximate equivalent of 1823p.

Amid current business uncertainty for Burberry, it remains to be seen if investors will discover new factors that are favourable enough to lift the stock much higher in the near term.