Burberry shares collapse but valuation still luxurious

Burberry’s plans to corner the market for upper-bracket fashion in Asia continue to unravel. The iconic British clothier confirmed on Thursday it had not escaped […]

Burberry’s plans to corner the market for upper-bracket fashion in Asia continue to unravel. The iconic British clothier confirmed on Thursday it had not escaped […]

Burberry’s plans to corner the market for upper-bracket fashion in Asia continue to unravel.

The iconic British clothier confirmed on Thursday it had not escaped the economic chill in China, which triggered this summer’s stock market crash.

With Chinese shoppers accounting for 30%-40% of the trench coat, accessories and perfume maker’s sales, Burberry has long sought to master China consumer trends.

But with key retail sales in six months to 30th September growing just 2%, after 8% in Q1, it appears Chinese shoppers are several steps ahead.

In response, Burberry said it was accelerating moves to control costs.

It expects this to minimise the impact on profits in its current financial year, enabling Burberry to meet updated analyst forecasts.

These currently suggest pre-tax profit of £446.3m, about 2% lower than in 2014-15.

Whilst damage limitation ought to cushion the sales fall of the year so far, more extensive action seems necessary for the longer term.

That’s because recent market research data suggests Chinese luxury consumers are spending more on ready-to-wear and new labels.

That’s a nuanced change in fashion taste of the biggest international spenders from the country, but one that luxury goods sellers can’t ignore.

Whilst overall global luxury sales growth dipped 5% in 2014 after 7% in 2013, well-heeled Chinese have largely sidestepped such thrift.

Data from tax-refund firm Global Blue indicates international spending by Chinese tourists rose 65.6% in August, and 73% in July year-on-year.

Crucially, the most recent research suggests two thirds of luxury purchases by Chinese buyers are now done overseas, mainly in hotspots like Paris, Milan, London, New York and Tokyo.

Jet-set shopping offers savings of more than 50% compared with China prices, thanks to foreign exchange rates, tax refunds and other discounts.

Unfortunately for Burberry, it has ramped up mainland China store openings in recent years, launching its 75th by early 2014, with plans for 100.

It appears to have 17 established stores in Hong Kong.

The latter are undoubtedly profitable.

But with APAC sales having declined for at least a year, and HK’s tanking in double digits, that pocket of Asian profitability could be shaky.

It bodes ill for the Westminster-headquartered company’s retail sales growth, which slipped into single digits in its last financial year, having been at 13% in 2013.

Burberry is also now less certain to meet the average annualised profit growth forecast for the UK luxury apparel sector.

The industry is currently expected to book profits that are on average 5% higher, according to Thomson Reuters data.

Burberry’s rose 5.7% in the year ending in March.

Investors have already begun to look elsewhere.

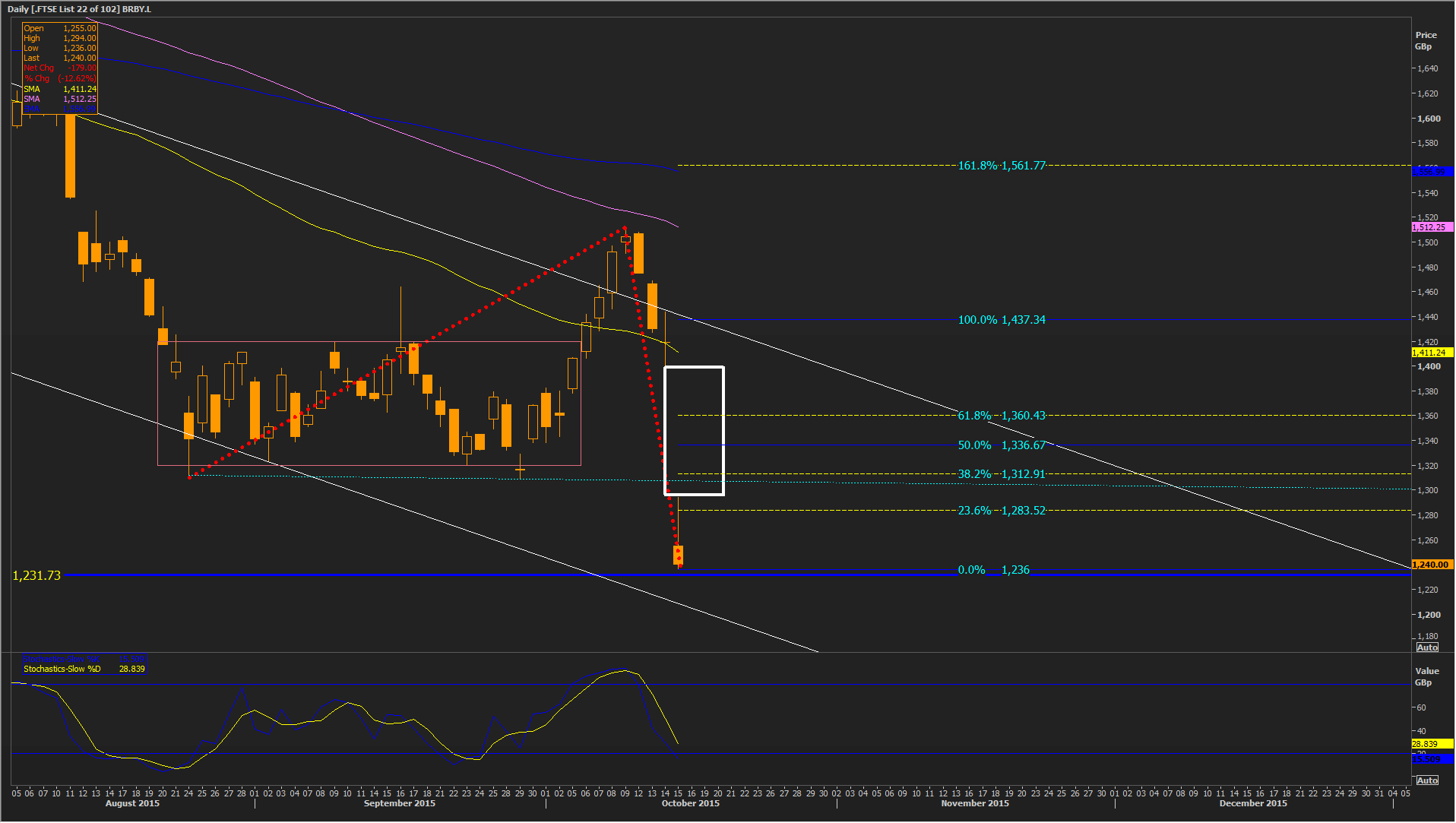

The down-trend in Burberry’s shares since February had already wiped 32% off the price by September.

With the stock collapsing by as much as 13% more on Thursday, its deepest drop for three years, it’s even possible selling has gone too far.

However, signs of the inflated valuation that took the stock to peaks above 1920p in the spring remain.

With a share-price-to-free-cash-flow reading of 25.34 at last count, Burberry is rated on par with Swiss behemoth Richemont, which at a market value of £25bn, is five times larger.

Burberry stock had fallen to within pennies of 1247p/1266p support, by online time, levels last seen during April 2013.

However, many investors who got (and stayed) on board the failed rally during late August to October, probably had second thoughts on Thursday.

Check out the gap between Wednesday’s close and Thursday’s open.

The area of consolidation seen late in the summer which spans quite a bit of that gap should prevent it from being filled in the near term.

With shares also having failed to escape the straits of a descending channel that has confined them since February, bargain hunting of this luxury name seems unlikely any time soon.

Please click image to enlarge