Key upcoming dates

After months of very little on the Brexit front, Brexit fears have returned with a bang over the past few weeks.

As the clock ticks down not just towards the end of the transition period on 31st December, but perhaps almost more importantly towards the UK government’s self-imposed deadline of 15th October, the markets are starting to tune into the fact that a no trade deal Brexit could be a reality.

Key upcoming dates

15th October UK government self-imposed deadline by which time EU – UK trade deal needs to be agreed. If there is no trade deal by this date, then the UK government has said that talks will end, and the UK will focus on no trade deal Brexit preparations.

Boris Johnson has been clear from the start that he has no intentions of extending the transition period, trade deal or not, covid-19 second wave or not.

Boris Johnson has been clear from the start that he has no intentions of extending the transition period, trade deal or not, covid-19 second wave or not.

26th November any trade deal must be presented to the European Parliament to ensure sufficient time for ratification.

10th December EC meeting by this time it is widely considered too late for any deal to be presented

How close are they and can they reach a deal?

Talks have been deadlocked for months. Progress in talks has been limited with both sides venting frustration at the lack of progress The two sides are still wide apart on several issues, most notably on business regulations which covers the extent to which the UK can support certain industries (the level playing field) and fisheries, access to British fishing waters.

How close are they and can they reach a deal?

Talks have been deadlocked for months. Progress in talks has been limited with both sides venting frustration at the lack of progress The two sides are still wide apart on several issues, most notably on business regulations which covers the extent to which the UK can support certain industries (the level playing field) and fisheries, access to British fishing waters.

Rumours swirled that the British government made some concessions over fisheries in the latest round of talks could have helped. Chief EU negotiator Michel Barnier and EU Commission President Ursula von der Leyen seemed marginally more optimistic saying that they believd that a deal could still be done. The Pound at these levels of around $1.28 is still optimistic a deal will be achieved, perhaps a little too optimistic.

Spanner in the works

British Prime Minister Boris Johnson recently threw a spanner in the works through the Internal Markets Bill. On a broad level this bill aims to keep trade fluid across the 4 countries which make up the UK – England, Scotland Wales and Northern Ireland. However, the bill also undermines some key parts of the Brexit Divorce Treaty, most notable the Northern Ireland protocol.

British Prime Minister Boris Johnson recently threw a spanner in the works through the Internal Markets Bill. On a broad level this bill aims to keep trade fluid across the 4 countries which make up the UK – England, Scotland Wales and Northern Ireland. However, the bill also undermines some key parts of the Brexit Divorce Treaty, most notable the Northern Ireland protocol.

The divergence from the agreed Brexit treaty not only breaks international law (in a limited and specific way according to the British government) but has the potential to derail Brexit trade talks. The bill has made it through the first vote in Parliament, however further amendments are to be voted and a compromise between Boris and the rebels in his part could still be reached.

A watered-down version of the Internal Markets Bill could be acceptable to the EU. However, the EU were clear that the original version had to be changed by the end of the month in order for a trade deal to be agreed.

No trade deal Brexit hits GBP

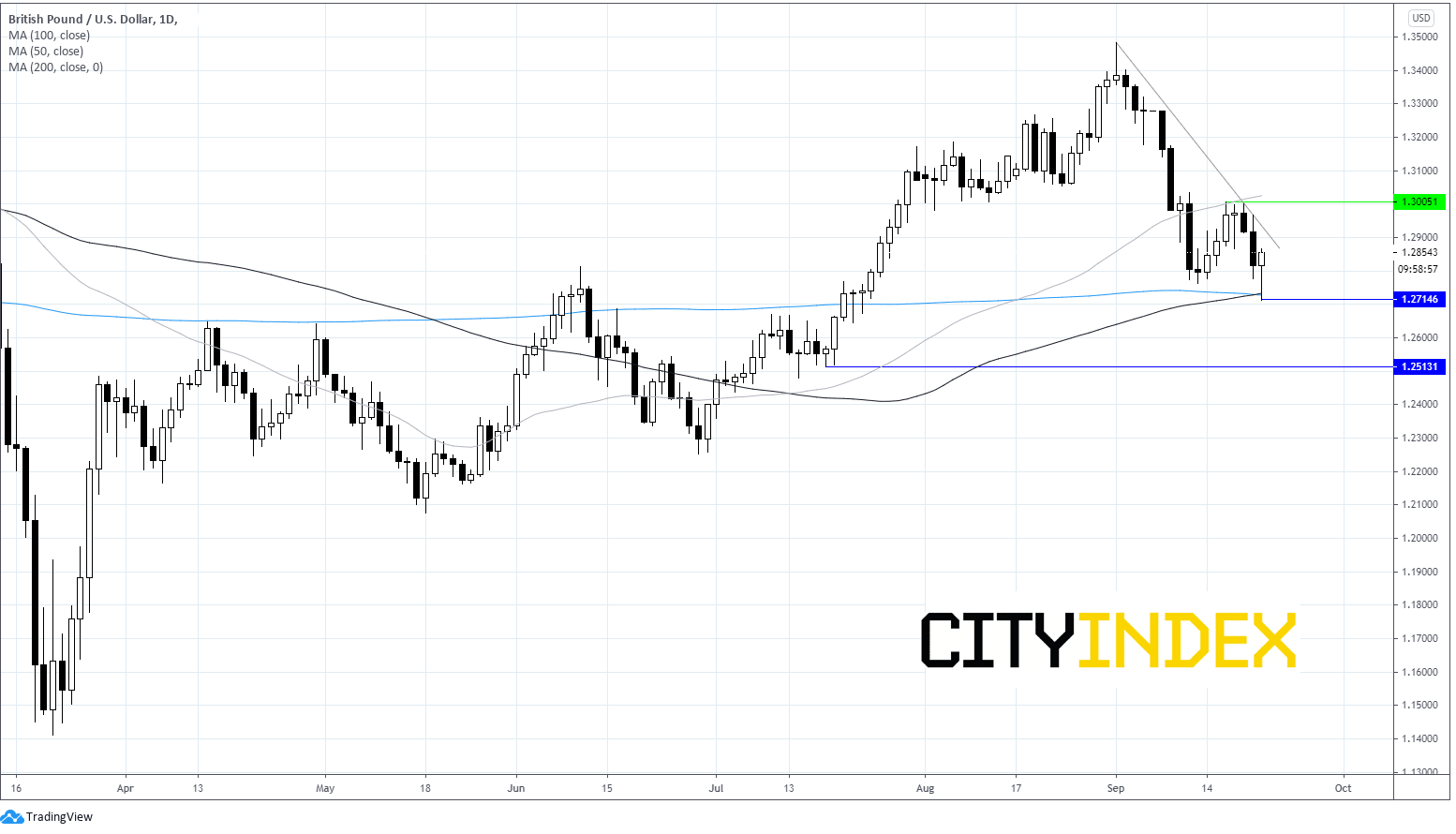

After the covid hit sent GBP/USD to 1.14, its lowest level in around over 3 decades in March, the recovery had been steady, hitting just below $1.35 on the first of September. GBPhas since dropped sharply versus the USD and the EUR since early September as concerns of a no trade deal Brexit started to appear. As fears over a no trade deal Brexit rise, the Pound could weaken further potentially pulling GBPUSD towrds $1.20. Any signs of a breakthrough could boost sterling back over $1.30

GBP/USD trades below its 50 day moving average on the daily chart. It tested its 100 and 200 SMA at $1.2710 today and the support held, for now. A breakthrough this level could see GBPUSD plummet to $1.25.

On the flip side, resistance can be seen at $1.29, the descending trendline, prior to the key psychological $1.30

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest GBP articles

April 3, 2024 02:49 AM

March 29, 2024 10:00 PM

March 9, 2024 04:00 PM

October 24, 2023 02:20 AM