Brexit what Brexit UK data continues to confound expectations

After the surprisingly strong UK inflation figures on Tuesday, the jobs and wages data released today confounded expectations once again, albeit to a lesser degree. […]

After the surprisingly strong UK inflation figures on Tuesday, the jobs and wages data released today confounded expectations once again, albeit to a lesser degree. […]

After the surprisingly strong UK inflation figures on Tuesday, the jobs and wages data released today confounded expectations once again, albeit to a lesser degree.

The average earnings index, which includes bonuses, rose 2.4% in the three months to June compared to the same period a year ago. The good news is that it was up from 2.3% in May, but it was slightly lower than 2.5% expected. The unemployment rate was unchanged during this period at 4.9%, but the employment rate hit its highest since records began in 1971.

Meanwhile, the more up-to-date data for July showed that claims for unemployment benefits fell by a good 8,600 applications. This was a big surprise in that not only did it easily beat expectations for a rise of 5,200 expected but more importantly it was a rise in the month after Brexit, when things were supposed to turn bleak.

Don’t jump into conclusions

So far, the evidence therefore suggests that Brexit isn’t having much of an impact on the jobs market. In a way this is not surprising because everyone knows that it will be at least two years before the UK actually leaves the EU. But it is early days to gauge even the near-term impact of Brexit, while it is also possible that the data is simply an outlier. So we shouldn’t jump into any conclusions, the Bank of England certainly wouldn’t.

Market reaction

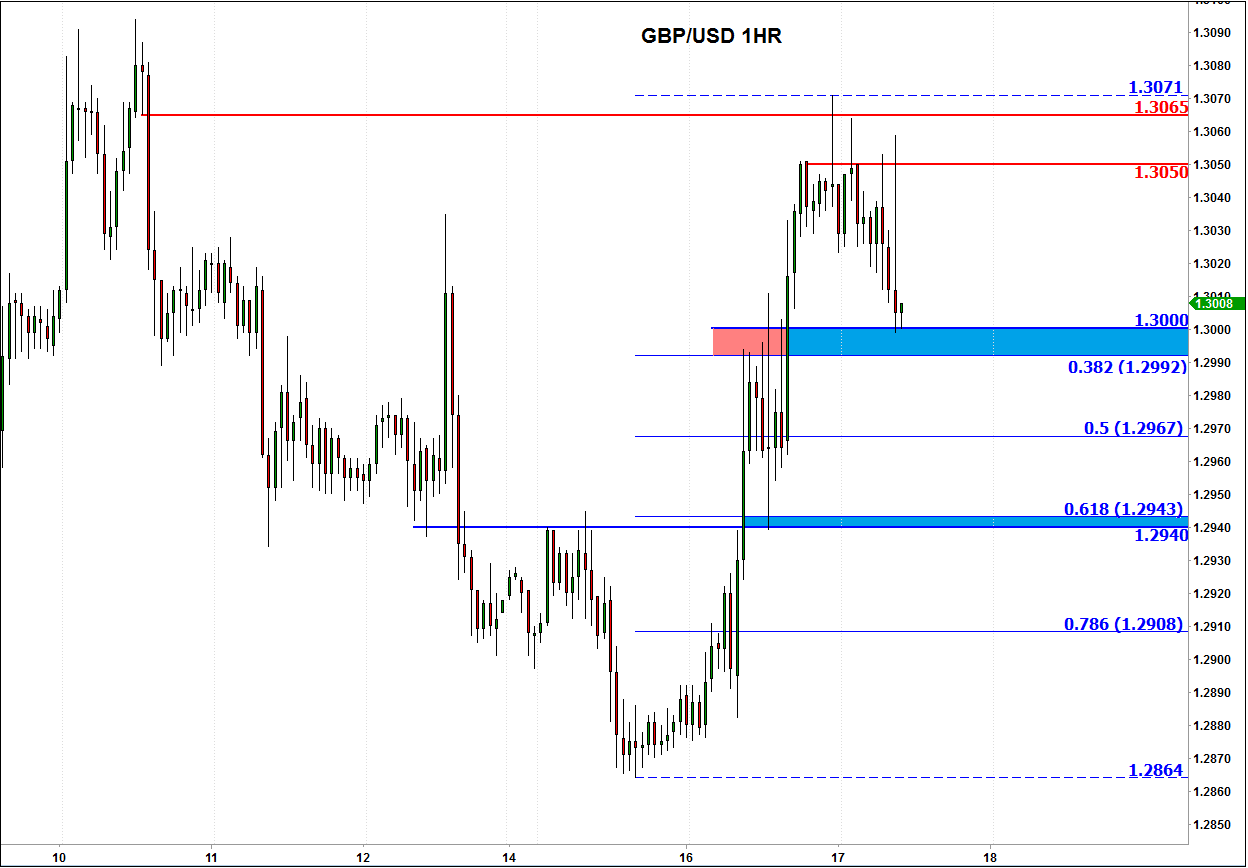

Indeed, that is how the markets took the news, judging by the behaviour of price action immediately after the data was released. The GBP/USD briefly neared its overnight highs, before starting to drift back from 1.3060 to trade at 1.3000 at the time of this writing. Against the euro, the pound also relinquished most of its early advance. But the pound may be able to regain its poise later on today for two reasons.

First, the FOMC’s last meeting minutes may reveal a dovish message, although if we go by what William Dudley, president of the New York Fed, said yesterday – that a rate rise next month was still possible – the minutes may not be dovish after all, causing the GBP/USD to slump.

Secondly, the short-term technical outlook on the Cable has turned bullish following yesterday’s rally, so we may see dip buyers emerge at these slightly lower prices, especially given the fact that the jobs figures were stronger-than-expected. Indeed, the Cable has been putting in a couple of higher lows and higher highs on its intra-day charts over the past 24 hours or so. Thus, we may see a technical rebound at around 1.3000 support or further lower at 1.2940/5 (both areas shaded in light blue on the chart). These levels were previously support and converge with Fibonacci retracement levels. The short-term bullish bias would be confirmed on a potential break above yesterday’s high of 1.3070. However, if yesterday’s low breaks down conclusively then that would invalid this bullish outlook. Today’s price action will therefore be very important.