Brexit bears stalk sterling again whilst investors wait

Six weeks before June’s referendum, markets are hotting up again, but shareholders seem less excited than forex traders, and some investors are sitting prettier than […]

Six weeks before June’s referendum, markets are hotting up again, but shareholders seem less excited than forex traders, and some investors are sitting prettier than […]

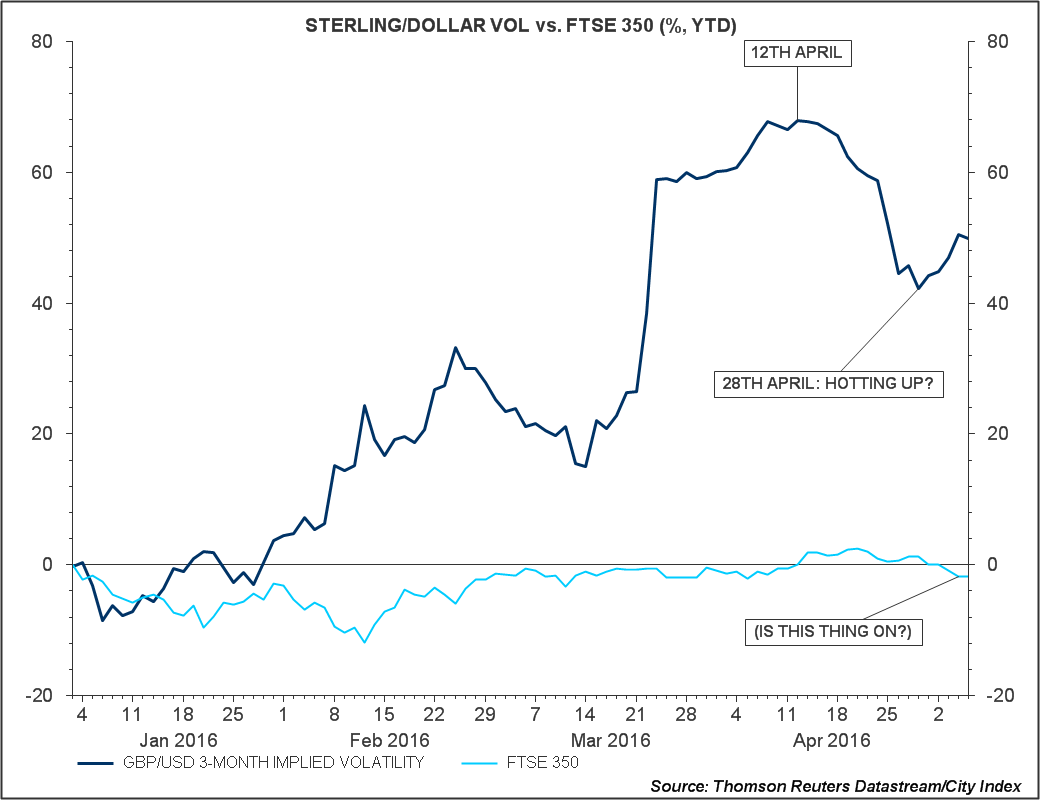

Whilst FX speculators have surged into ‘Brexit’ trades this year, pressuring sterling, stocks have moved far less.

The chart below compares sterling/dollar ‘Implied volatility’—basically the cost of options betting on a weaker pound—with the FTSE 350 stock index. Sterling vol. was still 50% higher for the year on Thursday. Even after a sharp fall last month. The FTSE 350 hasn’t moved as much. It is just a little lower for the year, having slipped almost 10% between January and early February, before recovering.

In other words, rumours of stock market Armageddon have been greatly exaggerated, so far, though that doesn’t mean there haven’t been losers. Shares of retailers and banks have glaringly underperformed the wider stock market since January. We think these sectors have fared worse than average because smart investors have picked ‘defensive’ stocks and sold those perceived to be exposed to the highest Brexit risk.

We single out banks. Whilst big lenders continue to face a host of stubbornly persistent ‘legacy’ woes, the sector is 20% lower this year compared to the FTSE 350’s 3% fall because investors are worried banks won’t be able to ‘passport’ into the EU after a Brexit.

We also point to retailers. They had previous challenges too; from minimum wage to changing shopping habits to Aldi/Lidl and more. However, UK-focused retailers also face one of the clearest exposures to sterling via their sales. And, whilst there’s no proven link between economic uncertainty from Brexit concern and falling consumption, there are compelling arguments. True, UK retail sales rose for the 35th straight month year-on-year in March. But more recently, unemployment rose for the first time in 7 months in April, and the economy turned in an even more anaemic 0.4% growth in Q1 than 0.6% in Q4.

Note that Next Plc., Britain’s biggest clothes retailer, is the FTSE 100’s worst-performer so far this year.

We’ve also spotted a clear recent trend of large banks advising clients to stay ‘defensive.’ In stocks, that usually means pharma, tobacco, utilities and the like. This has played out for Britain’s ‘Big Tobacco’ shares Imperial Brands (formerly Imperial Tobacco) and British American Tobacco. British smoking shares are among only a handful in Europe to set new all-time highs in 2016.

On the other hand, some shares have galloped higher by triple-digit percentages this year for reasons which have nothing to do with Brexit risk. Mining and some oil shares, we’re looking at you.

Well, the answer depends partly on your appetite for risk. If prepared to accept some, we see opportunities in the fact that many of the broad trends outlined above are likely to continue, with two clear exceptions. Those exceptions, in our view, are commodity and to an extent oil shares. After sharp and even eye-watering rallies across these sectors, we think shares have now caught up with the rally in resource prices. We’re also wary of the new clampdown on speculation in China. That means investors will need to become much more selective.

Elsewhere, we think careful selection can also still weed out potential further downside in banks.

RBS last week rounded off a dire first quarter for UK banks, with all of the ‘Big 3’ posting worst profits. Lloyds, RBS and Barclays are unlikely to rebound strongly before the 23rd June referendum date, and the weakest could even fall significantly more, before then. But not all British High St. banks are the same. For those wishing to maintain exposure to the sector, it may soon be time to position for a share price recovery of the strongest, assuming Brexit doesn’t happen, which we think is the likeliest outcome.

We would apply a similar approach to retailers. However for the High St. shops, prospects seem less clear cut, especially with the sector trading only a few percentage points below the main FTSE indices, compared to a 19% drop by the bank sector this year.

For currency traders, the main question is whether sufficient risk/reward remains on the downside for sterling against the dollar whilst GBP/USD is still 13% lower from November highs, though 10% higher since March.

As for trading ‘Brexit’ via the euro, in theory, the logic is sound: the EU also faces significant economic risk from a Brexit because the UK is a net importer from Europe. In practice though, traders have preferred betting the pound against the dollar. The euro was 6% higher against the pound (for the year) at the time of writing even after falling 3% in three weeks. There’s a chance that euro bulls have mispriced risk and may face a rapid unravelling of gains in the event of Brexit, or a pre-referendum sentiment switch.

Either way, we strongly advise traders to use tight stops. Polls and bookies odds suggest voters remain split, but both could turn out wrong. Sharp FX and stock moves are likely immediately before and after the vote, so it makes even more sense than usual to minimise your exposure to risk.

Conclusion

Sterling options volatility has rebounded after falling from highs in April. We interpret that as a return of bearish speculation against sterling, though we suspect the best upside in such trades has passed. We expect stock markets to retain their current defensive stance into the referendum though we also suggest it may be time to become more selective on shares of miners, oil companies and banks.