Post-election relief may have boosted Christmas trade for the ‘Big 3’

Not everyone liked the result but almost everyone could get behind reduced uncertainty. So goes one train of thought about the impact on the high street of Boris Johnson’s landslide general election win last month. At the very least, with a newly expanded Parliamentary majority, it is already evident that near-term political roadblocks that played a part in bringing UK economic expansion to a grinding halt, have been removed. Johnson’s Brexit deal, cleared the first hurdle in the Commons in late-December, setting up passage in a second vote scheduled this week, after which the bill will progress to the House of Lords. Multiple months over which political logjam halted investment plans, eventually eroding growth, look to be over. Consumer confidence that was sapped during those times is now speculated to be returning. Sterling’s surge in the wake of the election is a big factor. The resilient third quarter reported by clothes retailer Next last week may be a good sign of a similarly successful winter season for the UK’s biggest supermarket operators as they report Christmas and quarterly sales this week.

As welcome as the ‘Boris Bounce’ is, it can’t undo the toll that three years of uncertainty took on an already fragile British economy. Real wages may finally be rising, though gains may not be sustainable. At the same time, unemployment has been creeping higher for months. The threat of joblessness tends to have a more direct impact on consumers behaviour than inflation or other economic data. Furthermore, the political swing is more correctly described as a thaw than a breakthrough. The UK could face another cliff edge in December 2020, given that no comprehensive trade deal has ever been agreed in a year, yet Johnson insists that he would rather allow transitional arrangements to lapse without a deal than seek an extension if no UK-EU trade deal has been agreed by year end. If further retailers report higher than expected retail Christmas cheer, it could yet turn out to be a blip rather than a lasting change.

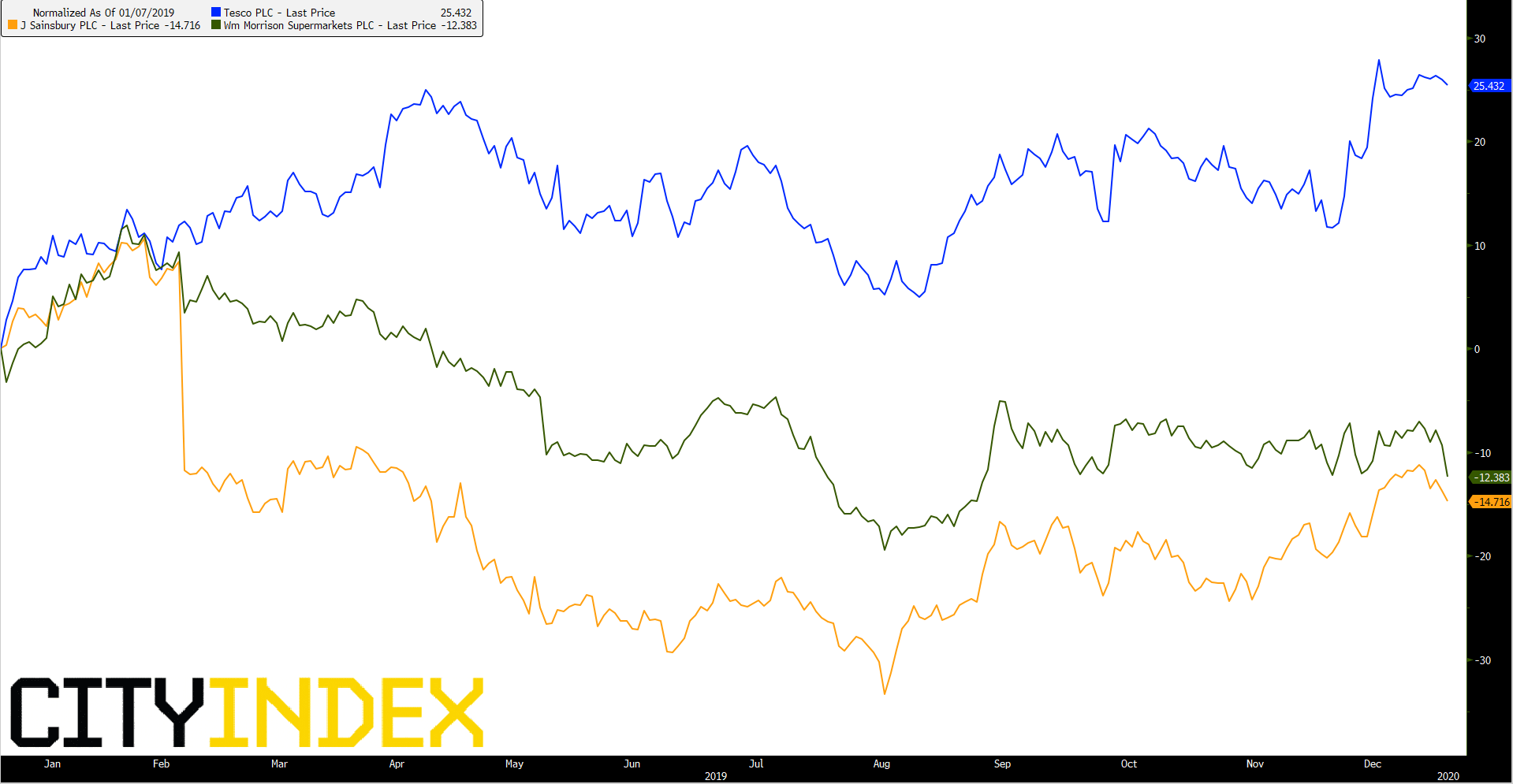

In the meantime, for most of the Big 3, resurgent seasonal sales ought to play particularly well for Sainsbury’s and Morrisons, given the wide divergence between their share price performance over the past year relative to Tesco shares. Consensus forecasts continue to point to an ‘ugly contest’ among the key operators. Investors still expect to choose between the least-worst. Consensus forecasts point to sales at stores open more than a year excluding fuel, also known as like-for-like sales, as declining at all three supermarket chains. Positive growth surprises should therefore have a disproportionate effect on shares of all three operators.

Normalised - J. Sainsbury Plc., Tesco Plc., Wm Morrison Supermarkets Plc. 07/01/2019 to 06/01/2020 19:00:53

Source: City Index

Below, we summarise the key points to watch on Britain’s key supermarket groups this week.

WM Morrison Supermarkets Plc. Q3 2020 Trading Statement, 07:00 GMT, Tuesday, 7th January

The UK’s third-largest grocer may offer early confirmation of a high street boost after December’s elections. If so, Q3 like-for-like sales may avoid a widely expected 1.9% slump, year-on-year. Attention will also fall on any updated guidance for 2019/20 growth. It is currently expected to improve to 0.5%. Morrison’s multi-channel – though relatively small vs. its rivals’ – online strategy is also in focus. Meanwhile, investors have been eyeing how soon Morrisons can widen a store-closure programme that aims to cut costs, as it also integrates a further 80 Argos units into supermarket space, whilst expanding convenience stores.

J. Sainsbury Plc. Q3 2020 Trading Statement, 07:00 GMT, Wednesday, 8th January

It was a bruising 2019 for Sainsbury’s. Chiefly, the UK’s Number 2 retailer failed to purchase Asda after the competition regulator ruled that doing so risked giving the enlarged group an unfair price advantage. During the fallout, it became clear that Sainsbury’s had no plan B to speak of. Furthermore, the impression grew that management had focused entirely on M&A at the expense of initiatives to maintain market share. Sainsbury’s subsequently launched a campaign to refocus on ‘entry-price’ food, with good results in ‘core categories’ in Q2. It also did less-badly than Morrisons in the December quarter, according to industry data. Analysts expect a 0.2% same-store sales slide in Q3, steady with Q2. Even if SBRY achieves or beats that, investors are likely to remain wary unless it adopts a more urgent stance on debt. Leverage began to creep higher last year, with net debt equating to 2.5 times Ebitda by late September vs. an average 1.5 times over the past 5 years. Higher leverage tends to argue against the group making much headway in terms of dividends this year.

Tesco Plc., Christmas and Q3 2020 Trading Statement, 07:00 GMT, Thursday, 9th January

Tesco’s key sales fell the least vs. rivals in the December quarter according to industry surveys. A possible bigger than average seasonal high street lift should therefore benefit Britain’s biggest retailer most. Like-for-like sales may fall 0.9%, looking at forecasts. Investors are also eyeing a cash flow boost as Tesco prepares to dispose of its $7bn business in Asia. As well, Tesco is quite the opposite to Sainsbury’s in terms of leverage, seeing credit rating upgrades over the last two years as improved cash generation helped reduce debt. With excess cash flow of £2.5bn eyed in the 2019/20-year, potential exists for dividends to increase as well as getting further ahead of pension and other obligations. Further positive comments on cash flow should offer Tesco shares the chance to participate strongly in any seasonal sector cheer, perhaps more than its main UK rivals, given its advantageous market share and more advanced state of financial repair. Meanwhile, CEO Dave Lewis is on his way out, to be replaced by lesser-known Walgreens Boots Alliance exec Ken Murphy at an as yet unspecified time this summer. Further outright details as to the transition may be sparse, but they could still impact the shares.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM