BoJ Decision amp EUR JPY Setup

A knee jerk reaction from traders and strategists to the latest increase in the Bank of Japan’s asset purchases may be to focus on the […]

A knee jerk reaction from traders and strategists to the latest increase in the Bank of Japan’s asset purchases may be to focus on the […]

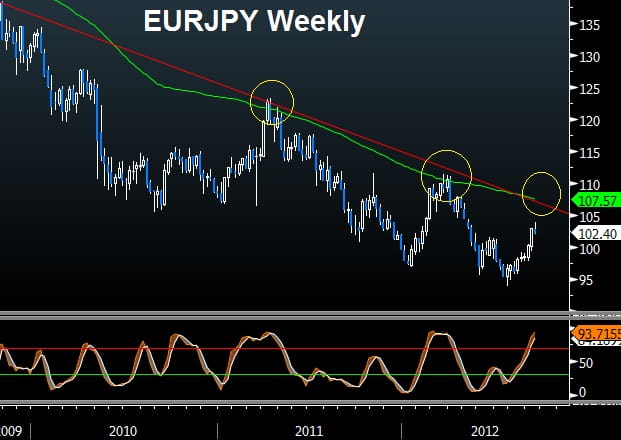

A knee jerk reaction from traders and strategists to the latest increase in the Bank of Japan’s asset purchases may be to focus on the USD/JPY pair, but a more interesting pair is EUR/JPY.

Overnight, the BoJ raised its asset-purchases by around Yen 10tn to Yen 80tn, by splitting the new purchases between short term government bills and longer term government bonds.

Here are four reasons why the BoJ action is seen more favourable to EUR/JPY than USD/JPY (which is most likely to chart another temporary rebound, limited at 80 yen).

1. The impact on equity markets from the triple dosage of stimulus from the BoJ, Fed (unprecedented in prioritizing employment vs. inflation) and ECB (integrating unlimited OMT to conditionality) is seen widely positive over the coming three months. Such developments are seen weighing on JPY and giving back EUR its positive correlation with equities, which it lost in Spring/Summer due to eurozone uncertainty.

2. While all major currencies are characterized by their own fundamental woes, the US dollar may suffer from the Fed’s open-ended QE3—which, unlike previous QE rounds, can be renewed until the central bank decides unemployment has stabilized. That is unlikely to happen any time soon as the term “structural” is becoming a more fitting description of US unemployment (no longer cyclical).

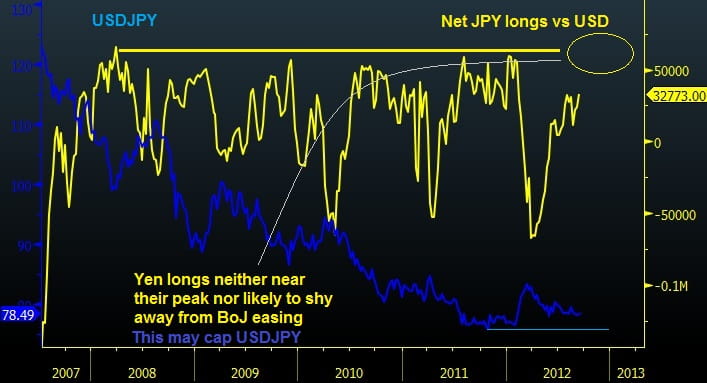

3. The USD is fighting time with the inevitable fiscal cliff. A second credit downgrade from Egan Jones and the latest outlook warning from Moody’s coupled with the monetary “debasement” from the Fed raises the vulnerability of the US currency during the central banks’ market-friendly stimuli. In such a set-up, the yen and the greenback are the least attractive. See CFTC chart of USD/JPY speculative commitments, suggesting further yen longs are in store.

4. Considering the previous pattern of rising global bond yields following QE1 and QE2, the negative correlation between JPY and global yields highlights upcoming yen weakness against non-USD currencies. One of them is EUR.

EUR/JPY may continue well into its four-year trend, but the policy historical double strike from the ECB and the Fed, alongside today’s BoJ action destabilizes the logic of EUR/JPY from remaining near 12-year lows. 104 appears as the interim target, followed by a correction testing 101 territory, before a retest of the 107 by mid Q4.