BOE Super dovish Thursday

The big data drop from the Bank of England turned out not to be too difficult for the market to digest, after all: no change […]

The big data drop from the Bank of England turned out not to be too difficult for the market to digest, after all: no change […]

The big data drop from the Bank of England turned out not to be too difficult for the market to digest, after all: no change in rates, only one dissenter and a sharp reduction in the Bank’s inflation rate for this year. Overall, this was considered dovish by the market.

Ahead of Super Thursday we had been looking for a slightly hawkish bias to these minutes, how wrong we were. Yet again the BoE has hinted that rates could rise sooner than the market expects only to back-track down the line. In recent weeks the BoE governor had hinted that a rate rise could happen at the “turn of the year” when a rate hike comes into “sharper relief”, this is a non-distinct period of time, but one would assume January. After today’s Inflation Report, expectations for the first rate hike have been pushed back out to late Q1 2016.

So when will the bank raise rates?

Carney has pulled a Yellen and said that the timing of the first rate hike will be purely data dependent. No matter how hard journalists attending the BoE press conference tried to push Carney, he would not put a date on the first hike, instead saying that the timing of the first rate hike doesn’t matter as much as the trajectory for rates. However, that is not true in these yield-starved markets, and when the first of the major central banks starts to raise interest rates is dominating market consciousness right now.

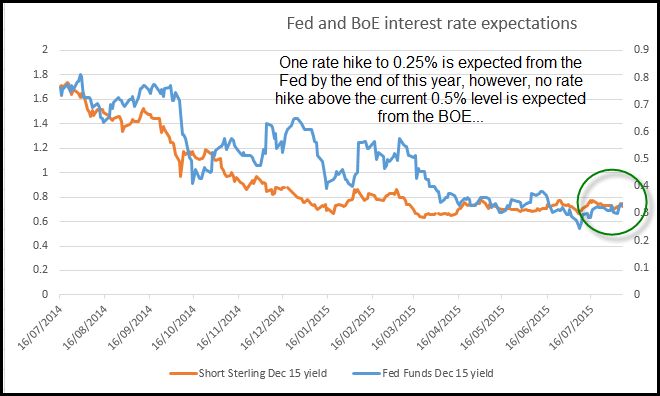

Post Super Thursday the market now expects Carney and co. to hike rates at least three months after the Fed, maybe 6 months if the Fed takes the plunge and hikes next month.

The key takeaways from Super Thursday:

The controversial elements of Super Tuesday:

What this means for the markets:

The main takeaway from the market’s perspective is that the Fed is expected to hike rates ahead of the BOE, as you can see below. GBPUSD took a tumble on the back of declining UK interest rate expectations, the low in cable on Thursday was 1.5468, just above the recent low from 23rd July. Currently GBPUSD is clawing back some losses and is back above 1.55. However, today’s data dump could consign GBPUSD to a long-term range between 1.5385 – the 200-day sma – and the recent high at 1.5650. For now 1.60 looks a long way off as upward pressure on interest rates remains muted. Tomorrow’s US payrolls report is also worth watching, at this stage the only thing that could boost cable would be a weak NFP reading, in our view.

What could have been a game changer for the UK rate outlook turned out to be a damp squib, we don’t expect the pound to find a strong trend in either direction for some time, and if we get a strong payrolls number on Friday then we could see GBPUSD fall to the bottom of the range we point out above.

Watch out for my colleagues’ deeper analysis of Super Thursday and its impact on GBP and the FTSE 100.

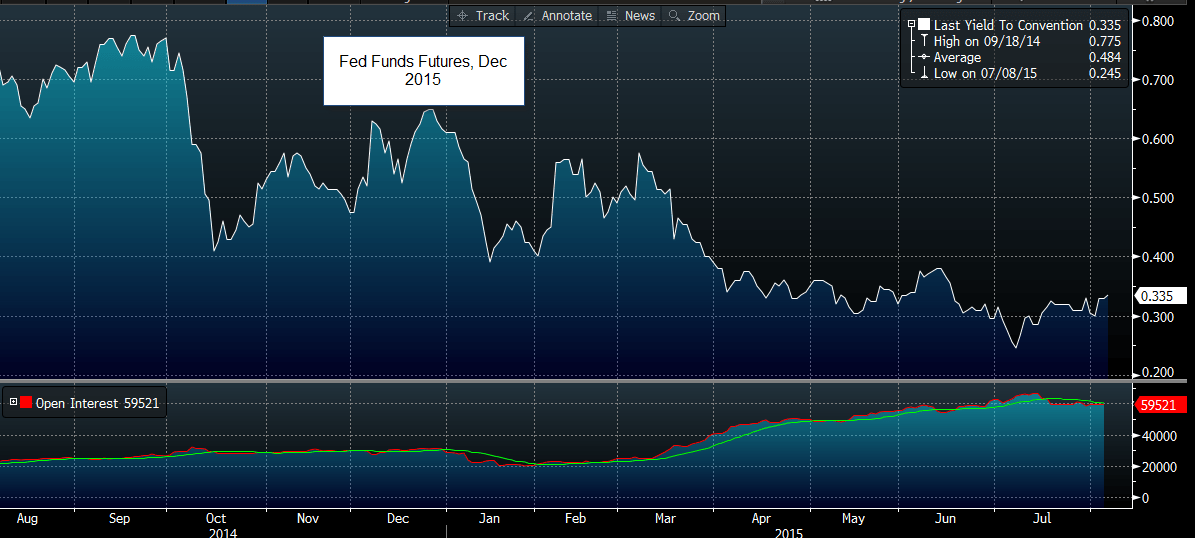

Figure 1:

Source: FOREX.com and Bloomberg

Figure 2:

Source: FOREX.com and Bloomberg