BOC Preview Keep the powder dry for another month

The next 48 hours will be massive for global central banks, with major monetary policy decisions taking place in Canada, New Zealand, the UK, and […]

The next 48 hours will be massive for global central banks, with major monetary policy decisions taking place in Canada, New Zealand, the UK, and […]

The next 48 hours will be massive for global central banks, with major monetary policy decisions taking place in Canada, New Zealand, the UK, and Russia all on tap this week. The first central bank to take center stage will be the Bank of Canada (BOC) tomorrow morning, and it looks like Dr. Stephen Poloz and company will have plenty to discuss.

Just a few weeks ago, many traders were expecting that the central bank would almost certainly cut interest rates from the current 0.50% rate amidst signs of a recession and rock bottom oil prices. Since then though, the data has shown a dramatic improvement in the Canadian economy, to say nothing of the 20%+ surge in the price of crude oil.

To wit, Canada’s June retail sales report showed a 0.6% m/m rise, triple the 0.2% growth expected two weeks ago, and that was followed by a solid 0.5% m/m GDP reading (vs. 0.2% eyed) and a solid 12k growth in employment (against expectations of a -5k decline) last week. The proverbial “cherry on top” of the run of good economic data was August’s Ivey PMI report, which printed at 58.0, nearly five points above the 53.5 reading anticipated by traders and economists. Therefore, while we still believe that the Bank of Canada could still cut interest rates later this year, it will likely prefer to keep its powder dry at tomorrow’s meeting and wait to see how the economy evolves.

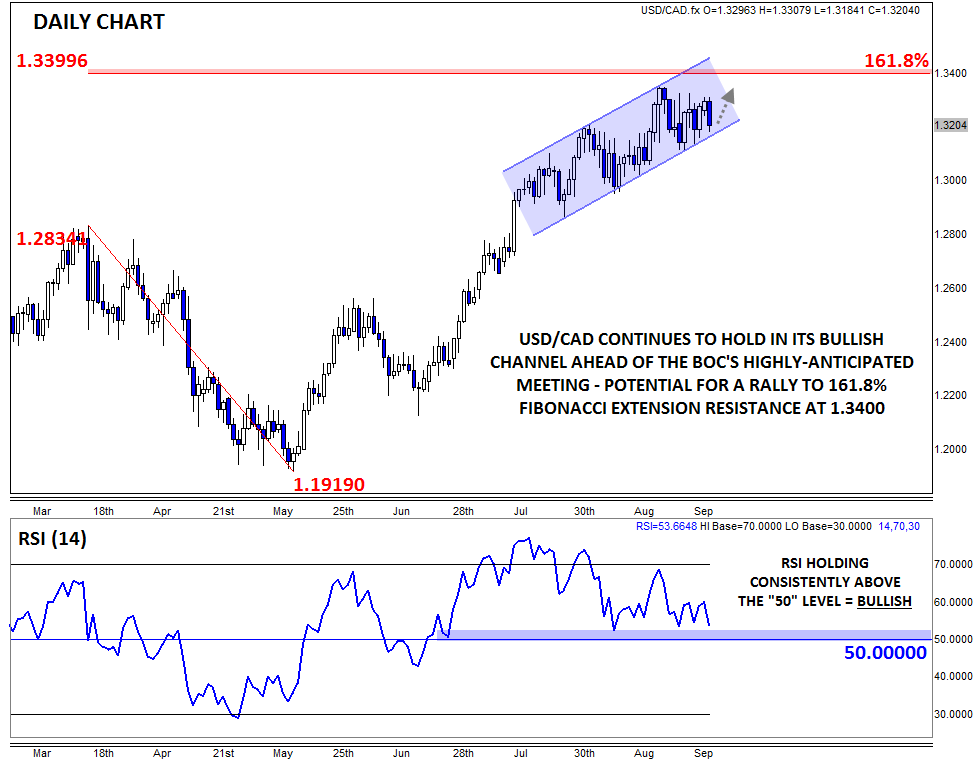

Technical View: USD/CAD

Despite all the firm fundamental data mentioned above, the Canadian dollar has struggled to rally meaningfully over the last few weeks. Since peaking near 1.3350, USD/CAD bulls have certainly took their collective feet off the gas, but bears have been reluctant to step in. As we go to press, the pair is trading near the 1.3200 level, just slightly off the high and still within the recent bullish channel. Meanwhile, the RSI indicator has held stubbornly above the 50 level, indicating that the bullish momentum remains intact.

In our view, USD/CAD’s resilience suggests that the pair is looking for an excuse to rally to the 161.8% Fibonacci extension of the Q2 pullback at 1.3400. Certainly, if the BOC surprises traders by cutting interest rates tomorrow, that could serve as an obvious bullish catalyst, but the unit could also find a bid if the central bank leaves the door open for a rate cut next month. Only if USD/CAD breaks below its current bullish channel around 1.3150 would the near-term bias shift to the downside for a possible dip back to the psychologically significant 1.30 level.

Source: City Index

Source: City Index