Mega-cap tech stocks have come roaring back in 2019

That follows a difficult end to 2018, when the group was hammered alongside the broader market on trade and rate-hike worries. Rallies of Facebook, Amazon, Netflix, Alphabet, plus Microsoft, Apple and Twitter, have largely continued since then, even as intensifying regulatory and competition scrutiny have combined to keep them on the defensive.

Scrutiny on Capitol Hill

Their perceived vulnerability hasn’t gone away though. The FANG group alone saw more than £100bn wiped off its value in just one day in June, as fears of a major regulatory crackdown returned. An inflection point was also evident on Wednesday, as a U.S. Congressional Committee grilled Facebook executives on everything from its planned Libra cryptocurrency, to privacy breach remediation efforts. Facebook has also reportedly settled with the Federal Trade Commission with a $5bn fine. Details are sketchy so far, but the risk is that the terms could impose new limits on the sprawling giant.

In perspective

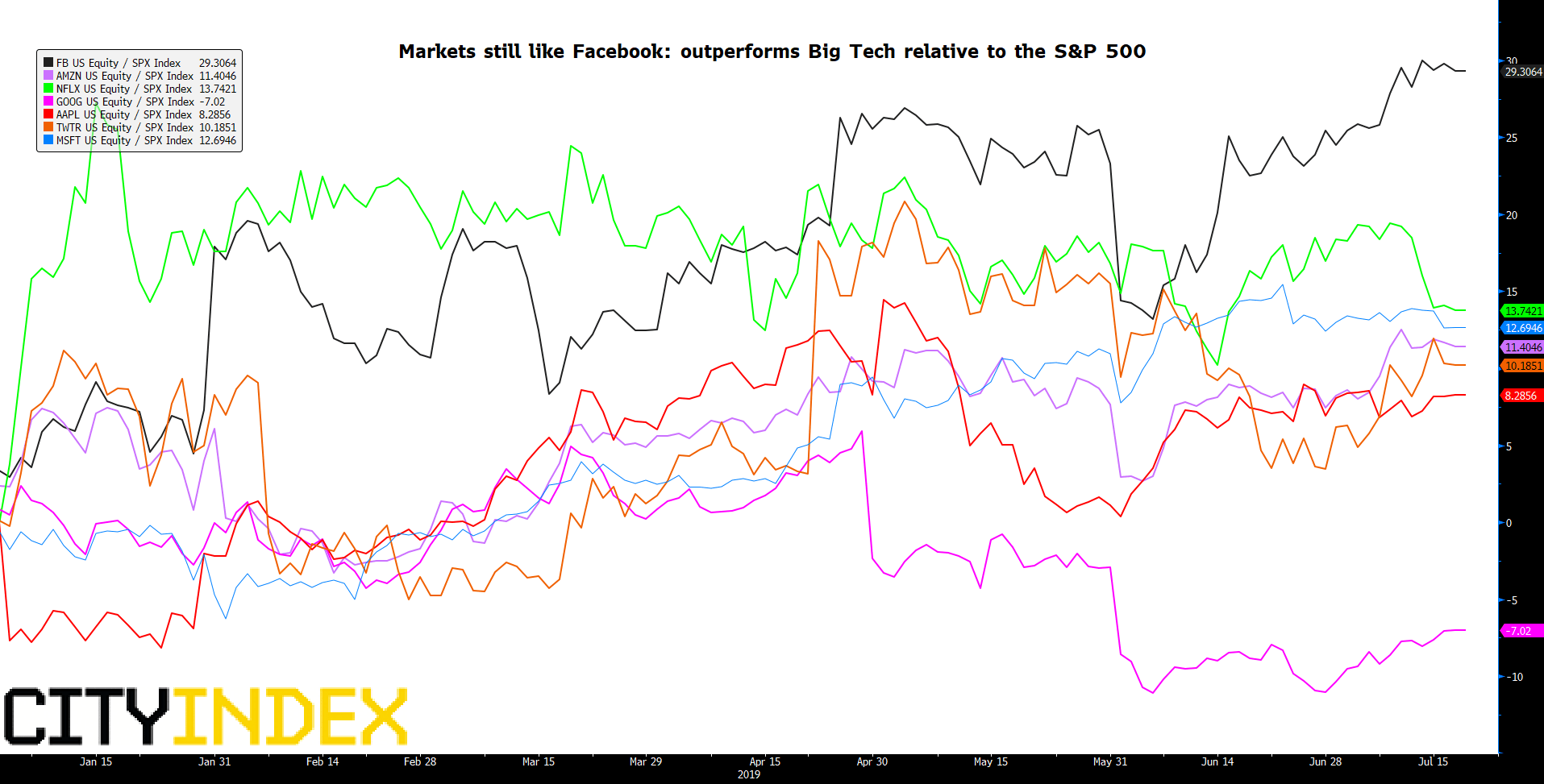

Still, it is telling that Big Tech shares have (excluding Alphabet) continued to sharply outpace the global market again so far this year. Facebook, arguably the lightening rod for a global backlash against Big Tech is actually leading the group, outperforming the S&P 500 by 29%.

Normalised chart: FB, AMZN, NFLX, GOOG, AAPL, TWTR, MSFT relative to S&P 500 – year to date

Source: Bloomberg/City Index

Such worries as applied to other tech leaders haven’t overridden demand for their growth and innovation stories. Markets are gambling that giant techs are adequately resourced to fight off the most onerous demands from Washington, Brussels and beyond, whilst absorbing the impact of any unavoidable sanctions. This assumes that calls to break-up the likes of Facebook, Alphabet and Amazon will go nowhere in a hurry.

Facebook, Google shrug off multi-billion fines

For Facebook, which has been in regulatory crosshairs since the Cambridge Analytica scandal, even a $5bn fine ranks as small fraction of its annual revenue. Alphabet’s multibillion-euro fines from the European Union have also been assessed by investors in relation to Google’s enormous revenues, profits and spending power. More broadly, global official sanctions on Big Tech companies’ size, market dominance, and more, appear to be too distant a prospect for investors to react to, let alone hedge. Furthermore, regulators don’t exist in a vacuum. Big Tech is known to have ramped spending on legal defence teams as well as lobbyists as an earlier stage of defence.

Focus eyes later quarters

As such, the most recent quarter for the likes of the FANG and beyond has largely been one where the focus has returned to previous challenges and successes around growth, plus the same worries that hang over other global industries—trade and the health of the world economy. Overall, most dominant U.S. consumer tech groups have or are on track to stabilise recent growth downturns, making for a largely steady quarter, with much investor focus on the second half of the year.

Here are the key watch points ahead of earnings from Netflix, Microsoft, Facebook, Amazon, Alphabet, Twitter and Apple

1. 17-Jul-2019 Netflix Inc Q2 2019 Earnings, 21:00 BST

After solid Q1 subscriber additions a strengthening content pipeline is expected to support the group’s ambition of maintaining global share and increasing scale. The watch will be on whether U.S. churn after price hikes, calms down, compared to Q1. Revenues are seen as flat vs. a year ago at $4.93bn. (Also see our preview on Netflix’s earning’s here.)

2. 18-Jul-2019 Microsoft Corp Q4 2019 Earnings, after U.S. market close

The corporate IT spending environment remains robust, meaning the closely watched cloud business is only likely to disappoint those seeking the highest possible double-digit percentage growth. Adjusted EPS is forecast to rise 7.3%, slower than the 19% seen in Q3. Revenues could also slow to an 8.9% pace vs. 14%

3. 24-Jul-2019 Facebook Inc Q2 2019 Earnings, after U.S. market close

Libra could continue to steal the limelight. The thinking is that Facebook’s crypto gambit could activate Instagram monetisation, enabling the group to tap the $1.4 trillion e-commerce market. First though, a likely $3bn-$5bn regulatory fine may get another airing, and ad price falls will be scrutinised. Underlying earnings per share will rise by a somewhat slower 8%, according to consensus, with revenue up 24.7% after a 26% lift last time

4. 25-Jul-2019 Amazon.com Inc Q2 2019 Earnings, after U.S. market close

Underlying EPS could still be up a creditable 10.5% in Q2, after exceptional items created a massively positive print in Q1. Revenue could show real growth too, at 18% vs. 17%. The move to one-day free shipping by Prime will be the hot topic. But the caution is that it will accelerate the cloud and ecommerce giant's already humongous spending, pushing out an expected operating profit goal in 2019 to 2020 at the earliest

5. 25-Jul-2019 Alphabet Inc Q2 2019 Earnings, after U.S. market close

After the White House’s Huawei backtrack, investors will want more details about where Google stands now with respect Play store sales to the Chinese handset giant. Either way, with Q1 bringing the slowest paid click growth in three years, revenue growth is forecast to tick down to about 17.6%

6. 26-Jul-2019 Twitter Inc Q2 2019 Earnings, before U.S. market open

One-off effects that doubled EPS in Q1 will be absent, leaving adjusted income up 11% and revenue growth of 16.8% compared to 18.4%. The best advance in daily active users for years, seen in Q1, is unlikely to be repeated as questions about slowing underlying user growth continue

7. 30-Jul-2019 Apple Inc Q3 2019 Earnings, after U.S. market close

A solid Q2 sets Apple up for a year that could surprise to the upside, especially with worst-case trade outcomes beginning to recede again. Continued strength in all non-iPhone categories is expected to keep the group on course for a return to strong growth in 2020. For now, sales are is seen coming in largely flat at $53.35bn. That would still be better than the 5% fall of Q2. EPS is expected to fall 8.4% year-on-year to $2.10

Latest market news

Today 08:15 AM

Latest Abe articles

October 24, 2023 09:00 AM

October 19, 2023 01:42 PM

October 11, 2023 02:28 PM

April 25, 2023 02:36 PM