BHP Billiton unveils potential asset spin off ahead of earnings

BHP Billiton does not seem particularly inclined to keep a low profile ahead of the mining multinational’s much anticipated full-year earnings next week. News reports […]

BHP Billiton does not seem particularly inclined to keep a low profile ahead of the mining multinational’s much anticipated full-year earnings next week. News reports […]

BHP Billiton does not seem particularly inclined to keep a low profile ahead of the mining multinational’s much anticipated full-year earnings next week.

News reports have been circulating for a few days suggesting the Anglo-Australian company is poised to embark on a wide-ranging reshuffle of its interests that would probably result in a spin-off of aluminium, manganese and nickel assets into a separate listed company, shares of which would then be offered to existing BHP shareholders.

The world’s largest resources company in market-capitalisation terms confirmed on Friday (15th August) a decision to de-merge the unwanted assets could be made as early as next week.

Assets might be worth around $14bn in total

Media reports suggested a potential release of $14bn worth of value.

According to the Australian Financial Review newspaper, plans for the spin-off were well advanced and would probably include its Nickel West unit, which BHP has had on the block awaiting a sale for some time. BHP was also debating whether to spin off its coal assets in New South Wales, according to the Australian newspaper.

BHP made no comment on Friday regarding the timing of an eventual de-merger, its likely value, or whether the coal assets would be included. It also declined to say how the dual-listed nature of its current market capitalisation would impact the distribution of news shares to be issued in the event of a spin-off.

However, it stated: “A de-merger of a selection of assets is our preferred option”, with its aim being to “generate stronger growth in cash flow and a superior return on investment”.

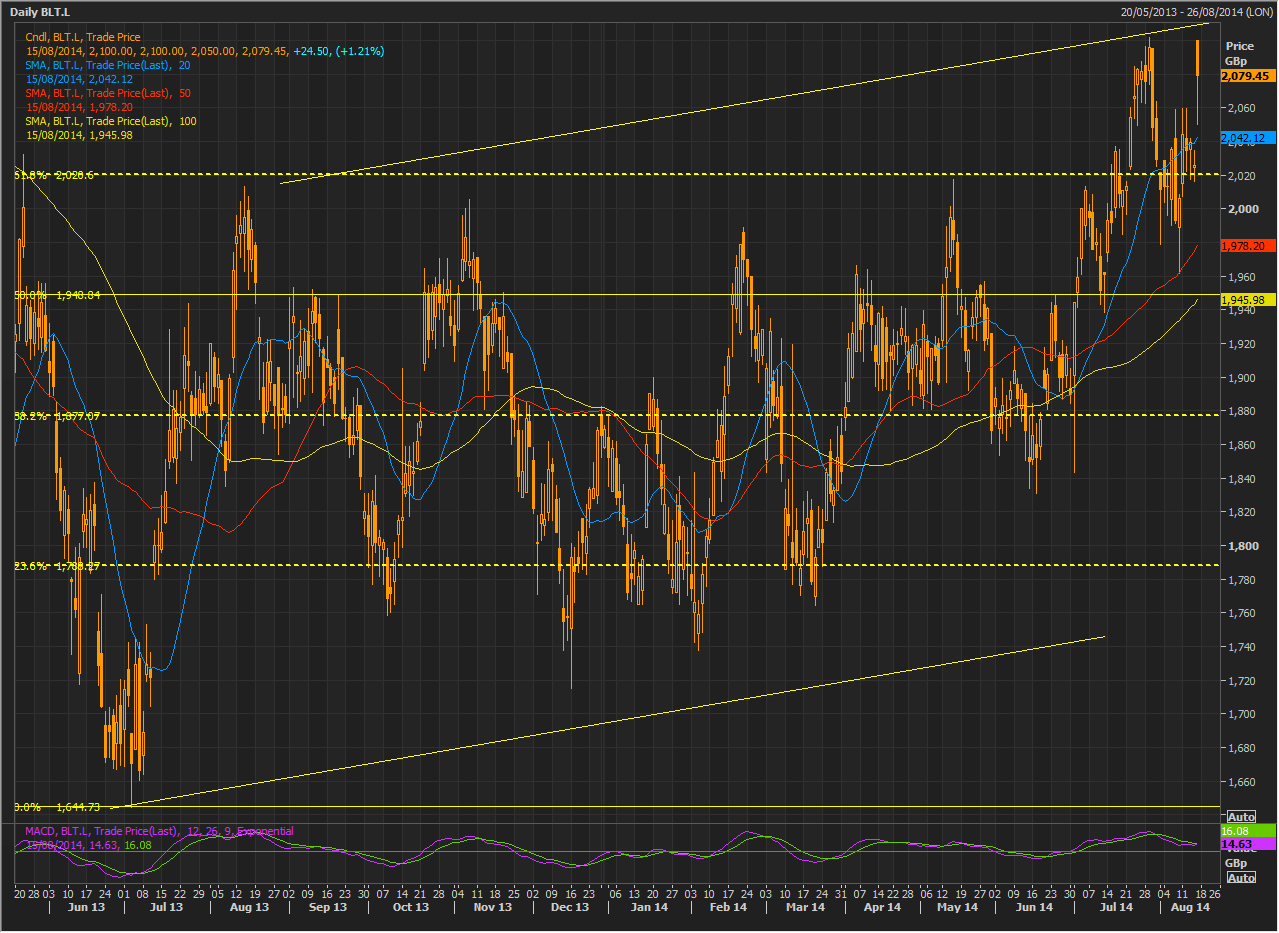

Either way, the news, coming ahead of the company’s preliminary full-year earnings announcement, has been taken by investors well, who sent the stock as high as 2100p, almost 3.7% higher on the day.

Investors appeared to be signalling their approval of BHP’s capacity to improve visibility into core assets previously obscured by unwanted businesses.

Additionally, the expectation of improved capital discipline inherent in a focused operational set and of course potential for increased shareholder remuneration, were also welcomed.

Potential spin-off assets didn’t produce that much profit

This was despite the fact that whilst the spin-off would be positive, the assets to be de-merged barely contribute to the earnings of the $185bn-capitalised conglomerate, in their current state.

The value of the assets and the capital strength of any new firm to be created by BHP are important qualifications for investors to consider.

Additionally, BHP is expected to load up the spin-off with between $1bn and $2.5bn in debt.

Finally, although, the company is clearly trying to wring the maximum public impact from news of its corporate actions, it’s worth remembering BHP already sold billions of dollars’ worth of assets in the last two years as part of its operational reorganisation plan.

As for next Tuesday’s earnings, BHP is depending on iron ore to bulk up 2014 income given BHP already beat its own guidance for full-year iron ore output, producing a record 225m tonnes.

Net profit is expected to rebound to $13.86bn for the year to June, a 27% hike from the year before.

Traders will react to the extent, if any, of the outperformance of net profit expectations, by playing within and perhaps slightly above the stock’s recent trend channel implying prices as high as 2112p.

Any downside shock in earnings (unlikely) or if further announcements suggest that today’s promising news was an attempt to butter the market up for an upset, could certainly send the stock back to Friday’s lows of 2050p or into the gap created by the difference between Thursday’s close and Friday’s open: 2017p to 2050p.