Barclays the new star of the banking sector

The chart below shows a funny phenomenon in the UK banking world. Barclays, the former bad boy of the financial sector and fine-payer extraordinaire, has […]

The chart below shows a funny phenomenon in the UK banking world. Barclays, the former bad boy of the financial sector and fine-payer extraordinaire, has […]

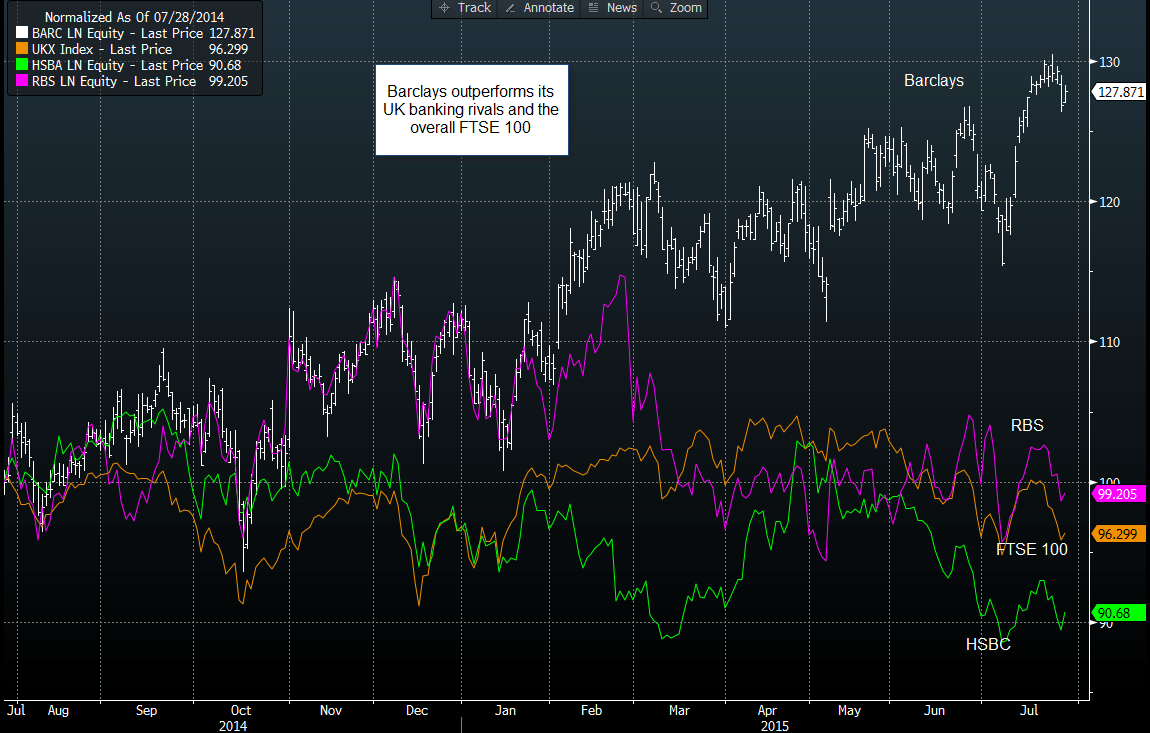

The chart below shows a funny phenomenon in the UK banking world. Barclays, the former bad boy of the financial sector and fine-payer extraordinaire, has turned a corner, at least that’s what its stock price is telling us. Ahead of its first earnings release since the departure of its conservative and retail-focused CEO Anthony Jenkins, Barclays has been outperforming its rivals including HSBC and RBS, and has also outperformed the overall FTSE 100 by a sizeable margin, as you can see in the chart below.

Figure 1:

Source: City Index, Data: Bloomberg

Figure 1 has been normalised to show how these companies move together, and, as you can see, Barclays has been outperforming since October last year. However, the real divergence happened earlier this year in April, when the FTSE 100 peaked, yet Barclays continued to move higher. This also marked the high in HSBC and RBS has pretty much been trading sideways since a sharp fall in February.

Barclays has managed to maintain its dominance in the face of a dramatic exit of its CEO and a strategy shift from a conservative, retail-focused banking business towards the higher risk investment banking of yester-year. Interestingly, this extreme shift in strategy hasn’t stopped Barclays from dominating banking stocks so far this year.

Why is Barclays outperforming?

We believe there are a few reasons:

So, while its rivals decide on things like where to locate its head-quarters and how to placate its government stakeholders, Barclays could stay ahead of the pack and return to riskier business practices after years of having to play it safe post the financial crisis. This was the main reason why CEO Jenkins stepped down earlier this year, and the market has given this shift in focus its seal of approval. Due to this, we think that Barclays may continue to outperform for the foreseeable future, even if we see further declines in the broader FTSE 100 index.

Wednesday’s Q2 earnings may determine the short-term direction of Barclays’ share price, the market is looking for an EPS of 0.06. This seems fairly low, considering that RBS is expected to report an EPS of 0.07. If Barclays’ earnings does slip compared to its peers then we may expect some weakness in the stock price, however, the medium-term direction could be dependent on the tone of the comments coming from Barclays’ high command. Any more detail on the shift towards a higher-risk strategy may continue to be rewarded by the market.