Barclays 8216 cost under control 8217 boast comes back to haunt its shares

The Fed’s equivalent of a ‘hawk raid’ last night— more by omission than commission (see dropped reference to ‘global risks’) stripped away the FTSE 100′s […]

The Fed’s equivalent of a ‘hawk raid’ last night— more by omission than commission (see dropped reference to ‘global risks’) stripped away the FTSE 100′s […]

The Fed’s equivalent of a ‘hawk raid’ last night— more by omission than commission (see dropped reference to ‘global risks’) stripped away the FTSE 100′s thin veneer of risk seeking on Thursday.

That exposed the index to disappointing blue-chip interim reports.

The reaction of Barclays’ shareholders to its third-quarter report was among the most striking.

The bank missed a string of targets.

Some of them were relatively trivial—leverage ratio increasing to 4.2%—others more serious, like the lack of Tier 1 Capital progress; the reading was flat on the prior quarter at 11.1%.

Barclays’ boast at the half-year that it had “costs under control”, whilst not entirely negated, rang more hollow on Thursday, as cost guidance unexpectedly rose.

£1bn will be spent on ‘ring-fencing’ its retail side from riskier businesses, it said.

It also set aside £290m as compensation for mis-sold foreign exchange products.

It looks like the lack of a CEO for the entire quarter is showing.

At the very least, expedited installation of former JPMorgan exec Jes Staley (who’s been in the CEO frame more than once) could have improved timing and execution during a tricky quarter.

Instead, there’s been no progress on Risk Weighted Assets and a hastily moved ROE goalpost for 2016—it’s now 11% from 12% before, despite robust comments on returns at the half year.

This has revived the spectre of a potential capital hike that was thought to have been banished in July.

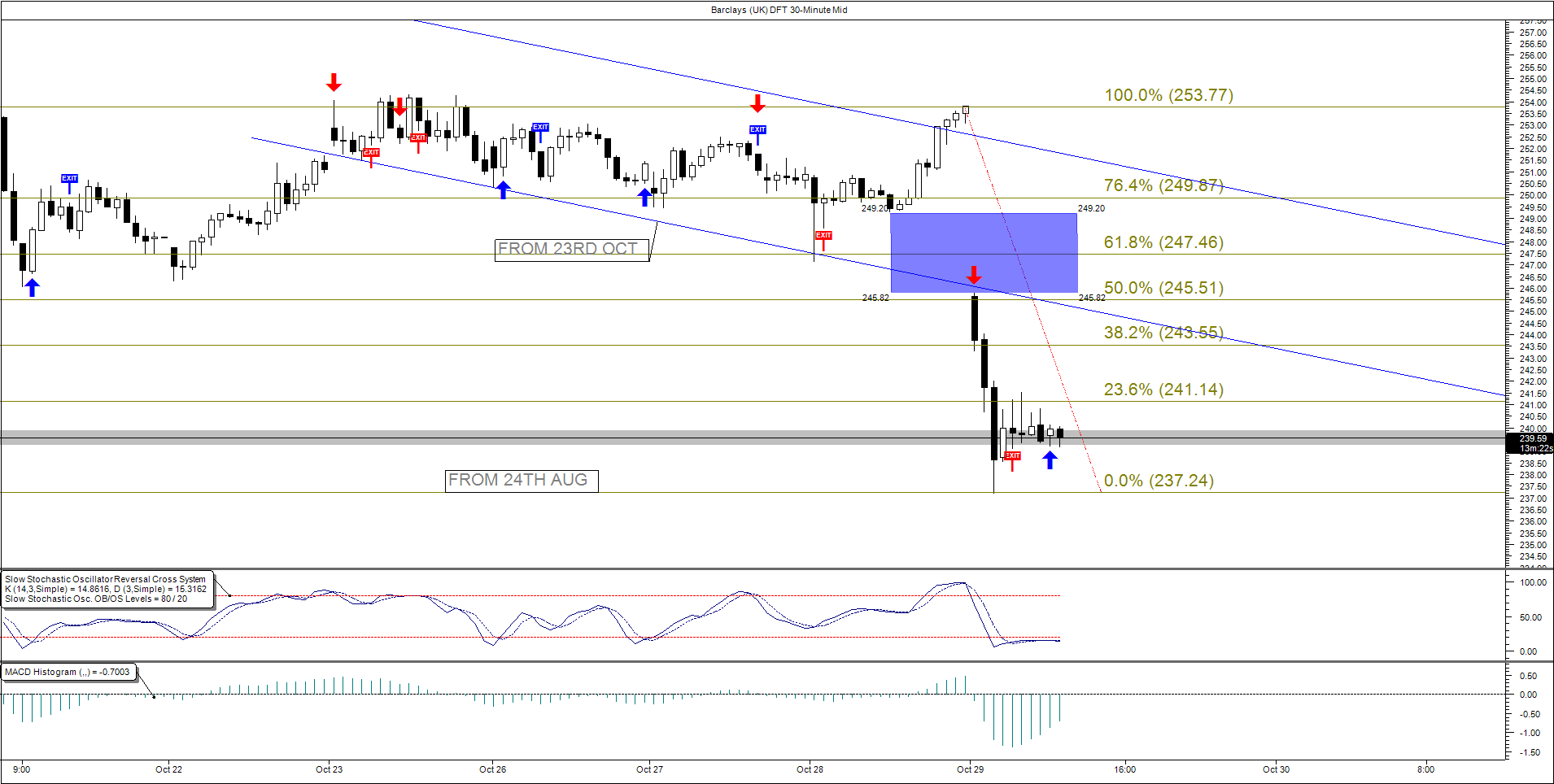

Barclays’ shares consequently slumped to near the bottom of the FTSE 100, losing as much as 6% on the day.

Short-term trading in City Index’s Barclays Daily Funded Trade showed some mid-session consolidation at online time.

The stock had bounced from support that successfully proved its worth during the sharp slide of global equities in late August.

However, short-term bounces will probably struggle to get above descending trends that commenced just under a week ago.

A price gap at Thursday’s open spanning 249-245.8 (the latter corresponding with 50% of Thursday’s slide) should also prevent a easy rebound in the near term.

The attached stochastic oscillator/trading system emitted a ‘long entry’ system a short while ago—the trade is certainly oversold in the half-hour time frame.

But the signal was almost immediately superseded when a ‘long exit’ was triggered, as conditions of the long entry lapsed.

This suggested selling pressure continued to dominate.

Corroboration was seen in the descending histograms of the second indicator, a MACD (bottom sub chart).

Their shortening trend needs to be watched closely as it could mark the reversal of the stock’s sell-off.

Please click image to enlarge