Bank of England to put brakes on rate cut

At 1200 GMT on 2nd February the Bank of England will announce its latest policy decision, it will also release its first Inflation Report of […]

At 1200 GMT on 2nd February the Bank of England will announce its latest policy decision, it will also release its first Inflation Report of […]

At 1200 GMT on 2nd February the Bank of England will announce its latest policy decision, it will also release its first Inflation Report of the year, and at 1230 GMT Governor Mark Carney will give a press conference.

The market is expecting interest rates to remain on hold tomorrow, in fact not one of the 57 economists polled by Bloomberg expect rates to change. Due to this, the economic forecasts contained within the Inflation Report have the biggest potential to move UK asset prices.

The key things to look out for in this IR include:

Growth forecasts: after the Bank of England’s chief economist said that the Bank’s own forecasts for growth after last year’s Brexit vote were too pessimistic, we expect GDP to revised higher, at least for the first quarter of this year. UK growth in 2016 was a solid 2.2%, spot on the BOE’s 2016 forecast. There is a chance that the Bank will revise up its 2017 GDP forecast, which stood at 1.4% back in November, as momentum seems to be boosting the economy at the start of the year. However, we expect the Bank to remain cautious on the economic outlook as problems could arise once Article 50 is triggered next month. Mark Carney may sound concerned about the UK’s economic reliance on a stretched consumer, and how adverse outcomes from the Brexit negotiations could hurt consumer confidence. The Bank may also revise down its business investment forecast, which was revised higher back in November, as fears of a hard Brexit cause UK-based corporates to put their spending plans on hold. Thus, we only expect a mild upward revision to the BOE’s GDP forecast to 1.8% or 1.9% for 2017; but alongside any GDP upgrade we would expect a hefty dose of downside warnings about the economic outlook from the Governor.

Inflation worries: There is a risk that the bank will, yet again, be forced to increase its inflation forecast for this year. In November the BOE expected inflation to rise to 2.8% in 2017, however, since then we have seen even more inflation pressures start to build. The UK 10-year inflation-linked bond yield is at a 9-year high. UK factory prices also rose at their fastest ever pace in January, suggesting that the impact of the weak pound is finally starting to bite. Wages are rising sharply, and the outlook is for further gains as an immigration clampdown could lead to labour market shortages, putting even more upward pressure on pay packets just as the economy starts to slow. It will be interesting to gauge the BOE’s tolerance for higher levels of inflation, even as the outlook for growth deteriorates. It is worth noting, that towards the end of 2016, Governor Carney signalled that patience with rising prices could wear thin at the Bank of England.

The future for monetary policy: We think that further policy loosening from the BOE is off the cards, and we look for the Bank to suggest that it is on hold for long-term. If the inflation forecast is revised substantially higher, say to 3% or above in the next 12 months, then we could see the market start to price in the prospect of a rate hike before end of 2018. Right now the Overnight Indexed swaps market is pricing in a 35% probability that rates will rise to 0.5% by the end of next year. Market expectations could shift sharply if the BOE strikes a less neutral and a slightly more hawkish tone on Thursday.

The impact of Trump: While we don’t think that the Governor will comment directly on the new US President’s unconventional policy decisions or on his team’s comments about the euro being under-valued, he might say that uncertainty around the Fed’s fiscal policy needs to be taken into account, as it could impact global growth next year.

Brexit: The Governor is likely to avoid discussions about the potential pitfalls from the Brexit negotiations once Article 50 is triggered, however, the BOE’s concerns are likely to be reflected in the growth forecast. A limited upgrade to GDP in 2017, and subdued forecasts for 2018 and 2019 suggest that the BOE is predicting a Brexit-inspired slowdown for the UK economy.

The impact on the pound:

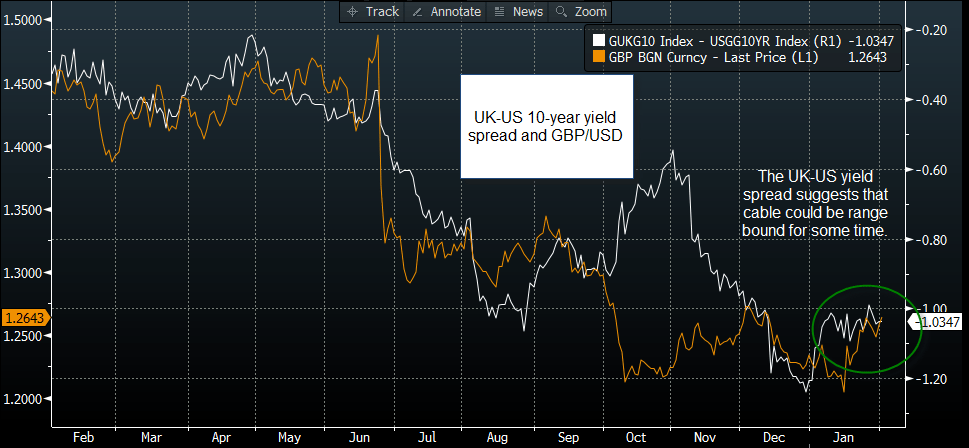

The pound has rallied into this Inflation Report and is the strongest performer in the G10 so far this week. The rally comes on the back of some better than expected economic data, a positive reaction to the Parliamentary debate on Article 50, and a general weakness in the dollar. The break above the 100-day sma at 1.2478, was a bullish development for GBP/USD, however, the yield spread between the UK 10-year yield and the US 10-year yield suggests range bound price action in GBP/USD for the foreseeable future (see chart below).

It could be a case of buy the rumour, sell the fact, and a positive GDP upgrade, along with signs that the BOE has shelved plans to cut interest rates further, could already be priced in. Thus, any hint of dovishness from Carney and co. could be met with a bout of GBP/USD weakness.

On balance, we think that the IR is likely to be constructive for cable, the dollar is struggling this week and even if we do see a pullback in GBP/USD it may be used as a fresh buying opportunity. We think that GBP/USD upside could have further to go, and may trade between 1.2420 – the Ichimoku cloud cloud base and a key support level – and 1.30 – the highs from October in the coming weeks.

Figure 1:

Source: City Index and Bloomberg