Balfour warns again shares lose 25

Balfour Beatty hasn’t managed to stop the rot. It’s announced its third profit warning in less than five months, lopping more than 20% off its […]

Balfour Beatty hasn’t managed to stop the rot. It’s announced its third profit warning in less than five months, lopping more than 20% off its […]

Balfour Beatty hasn’t managed to stop the rot.

It’s announced its third profit warning in less than five months, lopping more than 20% off its share price this morning.

The firm set itself a major challenge to convince the market of its strengths as a stand-alone entity when it decided last month to reject a merger offers from Carillion.

So far, it’s not doing particularly well with that challenge: it said today profit from its UK Construction unit would be £75m less than expected due to persistent problems on engineering projects in London and a raft of building works that led to contract losses and write downs.

Balfour’s strategy has been to try to re-position itself as an integrated construction and services firm with a particular focus on the US.

To that end, it has agreed to dispose of its US-based Parsons Brinckerhoff engineering unit for about £830m. Proceeds will partly be used to pay down net debt of around £500m.

Before this latest warning from Balfour market forecasts for the full year expected pre-tax profit of £133m.

Now, Balfour says this year’s final dividend and future dividend coverage are under review.

Trading across the rest of the group and full-year expectations remained in line with forecasts, the group said.

It’s continuing to repeat its mantra of the summer that it has faith in its stand-alone strategy in being capable of delivering value to shareholders in the medium term.

Even so, the stock has continued its recent downtrend and was about 25% lower at one point earlier on Monday, its biggest one-day drop ever taking the shares to 11-year lows.

The stock has lost more than 40% year-to-date.

Senior executives may be voting with their feet too: the departure of Balfour’s non-executive chairman Steve Marshall was announced today as well. He took the reins of the firm in May when CEO Andrew McNaughton stood down with immediate effect.

The firm said the process of appointing a new chief executive was at an advanced stage.

Marshall is expected to hand over responsibilities to a new CEO and await the identification of a new non-executive chairman before leaving.

“This latest trading statement is extremely disappointing”, conceded Marshall in a statement. “There has been inconsistent operational delivery across some parts of the UK construction business and that is unacceptable.”

Marshall said Balfour had appointed accounting firm KPMG to undertake a thorough review of the contract portfolio of Construction Services UK.

Investors will of course wonder if today’s update from the FTSE 250-listed firm marks the bottom, for Balfour after its recent troubles.

The fact management has decided to call in an external auditor to look at its construction business may or may not indicate internal worries about deeper problems there.

The scope of the review seems broad though: KPMG will look into commercial controls, completion costs and contract value forecasting.

Current executive chairman Marshall said the independent review was required to “give investors the assurance they need”, although Balfour had “made full allowances for everything we know about”.

The write downs were mostly related to projects the group had already warned about, the group said. Many of these would end in the current financial year, it added.

Even so, perhaps potential control risks might need to be added to the broad question of scale Balfour faces in its attempt to compete with closest UK peer and former potential merger partner, Carillion.

The question we grapple with following today’s news is this: even if we assume zero contribution from UK Construction at this point, will that be the end of the matter?

The only fair answer is ‘maybe, but definitely not yet’.

That’s because Balfour like many large construction businesses, not only has many contracts in the works, but other obfuscating factors in the mix like corporate deals pending completion too (Parsons is the latest big one.)

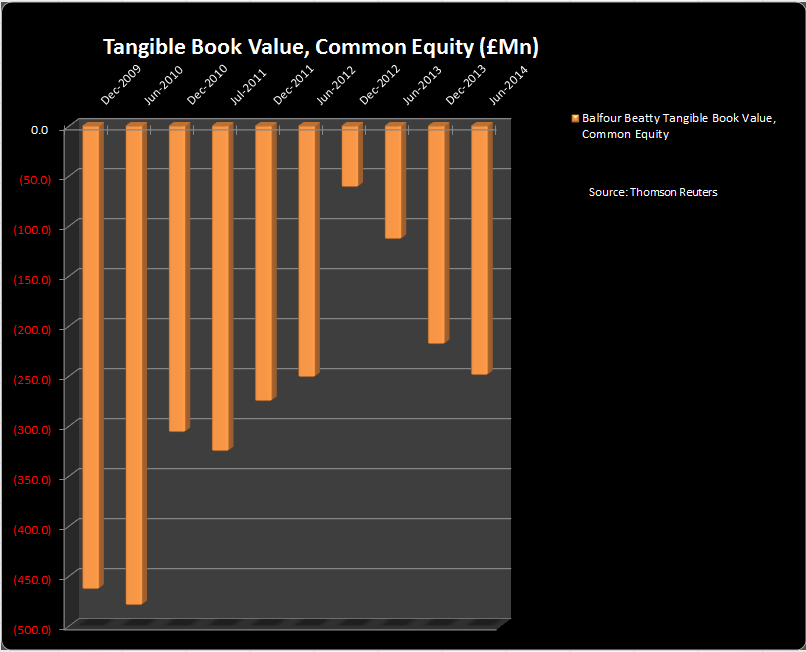

Getting an accurate idea of carrying value isn’t easy. ‘Tangible Book Value’ might be a fairer measure. The trend isn’t particularly encouraging.

The reportedly ‘aggressive’ margins in contracts signed by the group appear quite well represented. Whilst Balfour’s attempts to reverse the implied poor returns are also evident, a respectable recovery seems unlikely in the medium term.