Aussie fiscal tightening will pave way for RBA cuts

The Australian Treasurer, Wayne Swan, today released the final budget outcome for the financial year ending 30 June 2012. The good news is the budget […]

The Australian Treasurer, Wayne Swan, today released the final budget outcome for the financial year ending 30 June 2012. The good news is the budget […]

The Australian Treasurer, Wayne Swan, today released the final budget outcome for the financial year ending 30 June 2012. The good news is the budget deficit was slightly lower than expected, the bad news is that it has still managed to double to A$43.7bn. No surprise in the market though as this is largely a backward looking number that has been factored in. The commitment to maintain a surplus in 2013 is perhaps more important. The surplus has no bearing on Australia’s credit rating and is largely a token measure, rather than a real effort to reign in the economy. It is an election promise, one which is becoming harder to achieve but the government knows very well that its core strength is economic management and a departure from the surplus pledge would be near fatal politically.

Swan reiterated a 2013 surplus whilst acknowledging that tumbling tax receipts are still taking a toll on the budget. The recent fall in bulk commodity prices in particular means that the government assumptions going into the 2013 financial year and outcomes for receipts are likely to show many large discrepancies. Not only are prices below their highs, but they are below the assumptions used to compile the 2013 numbers in May. So it is ‘back to the drawing board’.

What does the Treasurer do if the income side of the equation is not performing and the net outcome needs to be maintained, mainly for political reasons? Cut the expenditure – this was reaffirmed by Swan today. The cuts need to be large enough to balance the books, we will get a better idea of where they are targeted in the mid year review due sometime in November. With the government cutting back its expenditure, the Reserve Bank of Australia is better placed than ever to provide more monetary easing. Next month’s meeting is shaping up to be very interesting – not only will the RBA have to acknowledge the impact of mining related expenditure being pushed back, but also a very firm government commitment to cut spending in order to achieve a surplus budget outcome.

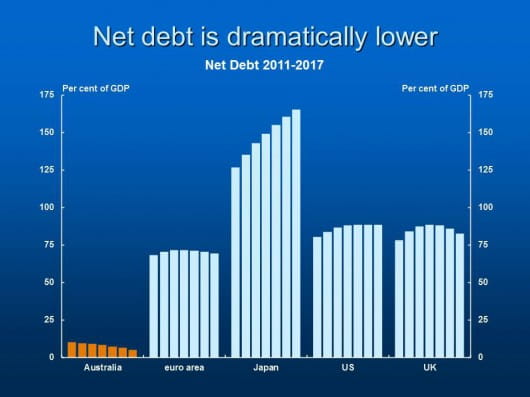

Despite all the noise around the budget outcome, Australia still enjoys some of the most attractive public credit metrics when taking the size of its economy into consideration. While the rest of the northern hemisphere struggles to contain spiralling sovereign debt, yet alone strive to balance budgets, Australia’s debt is likely to peak at around one tenth of the major advanced economies before falling near zero by the end of this decade. The chart below was published by Swan today on his official Twitter feed (@SwannyDPM). At first glance it provides comfort for Australians in general to see their debt situation in context. But on deeper consideration, one can’t help but wonder at what advantage low debt really comes, if the sovereign problems of the others on the chart will always have an impact on the Australian economy.