AUD USD Light on the horizon for long term bulls

Because we’re entering what is historically one of the quietest periods for markets, we’ll be taking the opportunity to take a longer-term view of many […]

Because we’re entering what is historically one of the quietest periods for markets, we’ll be taking the opportunity to take a longer-term view of many […]

Because we’re entering what is historically one of the quietest periods for markets, we’ll be taking the opportunity to take a longer-term view of many major FX pairs and markets over the next two weeks, starting with AUD/USD today.

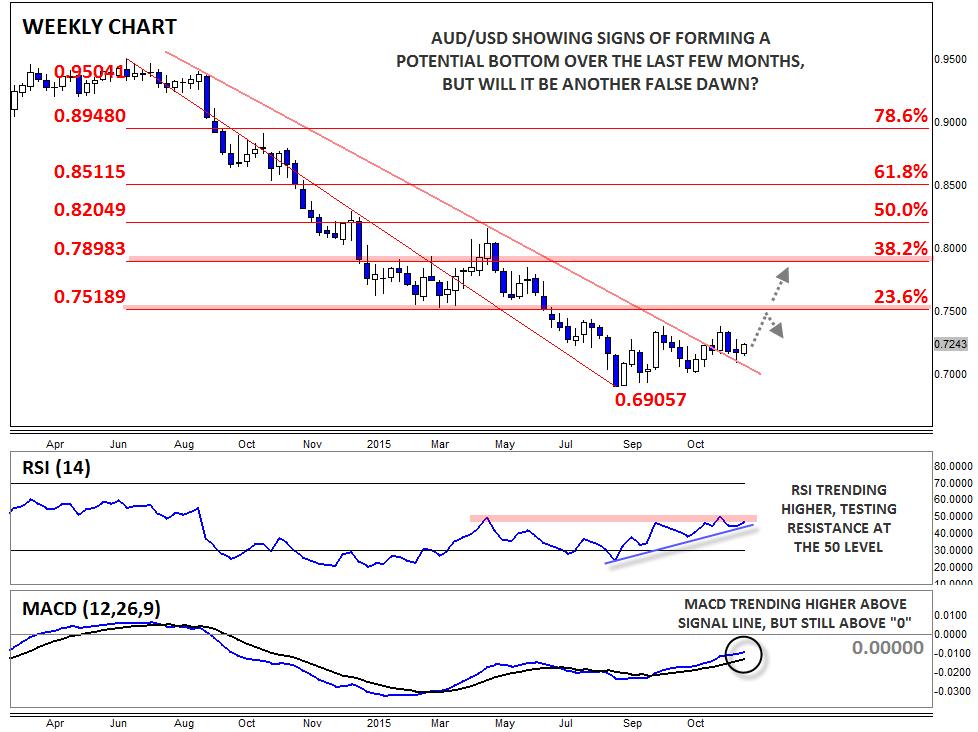

AUD/USD has no doubt had a rough couple of years, with rates falling from a high near .9500 all the way down to a low below .7000 in early September. From a fundamental perspective, the driving force behind the drop has been a fall in the price of key commodities (mainly industrial metals) as a result of an economic slowdown in China.

For instance, the price of copper recently hit its lowest level since the Great Financial Crisis around $2.10/lb, while iron ore dropped its weakest level since 2007. The impact of these collapses cannot be overstated: they’ve led to major terms of trade and labor market troubles Down Under and forced the Reserve Bank of Australia into a more dovish posture. Given the challenging backdrop for commodities, the weakness in the Aussie over the last 24 months is no surprise.

That said, we’ve actually seen the AUD/USD show signs of forming a potential bottom over the course of Q4, creating a faint light on the horizon for beleaguered Aussie bulls despite the ongoing weakness in the metals markets. The pair has rallied nearly 500 pips from trough to peak and has now put in three higher lows over that period. Crucially, rates have now broken back above the 15-month bearish trend line running through the high from the last rally in Q1. After breaking above that barrier, rates dipped last week to retest the trend line from above, but buyers were able to defend that key level, confirming that the previous resistance level has now become support.

At the same time, the secondary indicators on the weekly chart have turned more optimistic than at any point in 2015. The RSI has formed a mini bullish trend and is now pressing against key previous resistance at 50, while the MACD is also trending upward above its signal line and approaching the “0” level.

As we move into 2016, the key area to watch on AUD/USD will be from .7400 to .7500. This corridor represents resistance from the four-month high and the 23.6% Fibonacci retracement of the entire 2014-2015 drop. If bulls can push rates above that key barrier early next year, another leg higher into the upper .7000s or even the 38.2% Fibonacci retracement near .8000 could be in play. Of course, we saw a similar false dawn at the beginning of last year, so bulls should be prepared to jump ship if September’s low near .6900 gives way at any point in 2016.