The US dollar slid sharply late last week due in part to President Trump’s announcement of impending U.S. import tariffs on steel and aluminum, sparking fears of global trade wars on the horizon. On Monday, however, the dollar steadied as markets calmed down and rebounded, and better-than-expected non-manufacturing PMI data from the U.S. indicated continued expansion of the critical services sector. Overall, the US dollar remains weak against its major counterparts, but was in the midst of a tentative rebound prior to Trump’s announcement of tariffs late last week.

Against the Australian dollar, the US dollar has shown particular strength since late January. AUD/USD has been biased to the downside in part due to rising expectations of higher interest rates from the Federal Reserve, while expectations of monetary policy changes from the Reserve Bank of Australia (RBA) have remained stagnant. On February 6th, the RBA left interest rates unchanged as widely expected, marking a full year-and-a-half without any rate changes. The central bank is not expected to raise interest rates until either late this year at the earliest, or possibly next year. The RBA’s recurring concerns about a strong Australian dollar is one of the factors precluding a more immediate rate hike.

Tuesday brings a slew of key data releases from Australia, including another RBA policy decision, that could have a significant impact on the Australian dollar and AUD/USD. First up is Australian current account data (expected at -12.3B for Q4 2017), which includes trade balance information, a timely data release given recent concerns over possible trade wars sparked by Trump’s announcement of US tariffs. Also to be released around the same time will be Australian retail sales data for January, expected to have grown by +0.4% month-over-month after December’s disappointing -0.5% decline.

As noted, the RBA also reports its latest monetary policy decision on Tuesday, and the consensus is that it will leave the cash rate on hold at 1.50% and refrain from making any significant policy changes at this time. The central bank is also expected to indicate that rate hikes are unlikely to occur on the near horizon. The RBA, as mentioned, is not expected to raise interest rates until either late this year at the earliest, or possibly next year. If this is indeed the tone of the RBA on Tuesday, the Australian dollar could continue to weaken against the US dollar. If, however, the central bank indicates a more hawkish stance or a potentially sooner rate hike, the Australian dollar could receive a sharp boost.

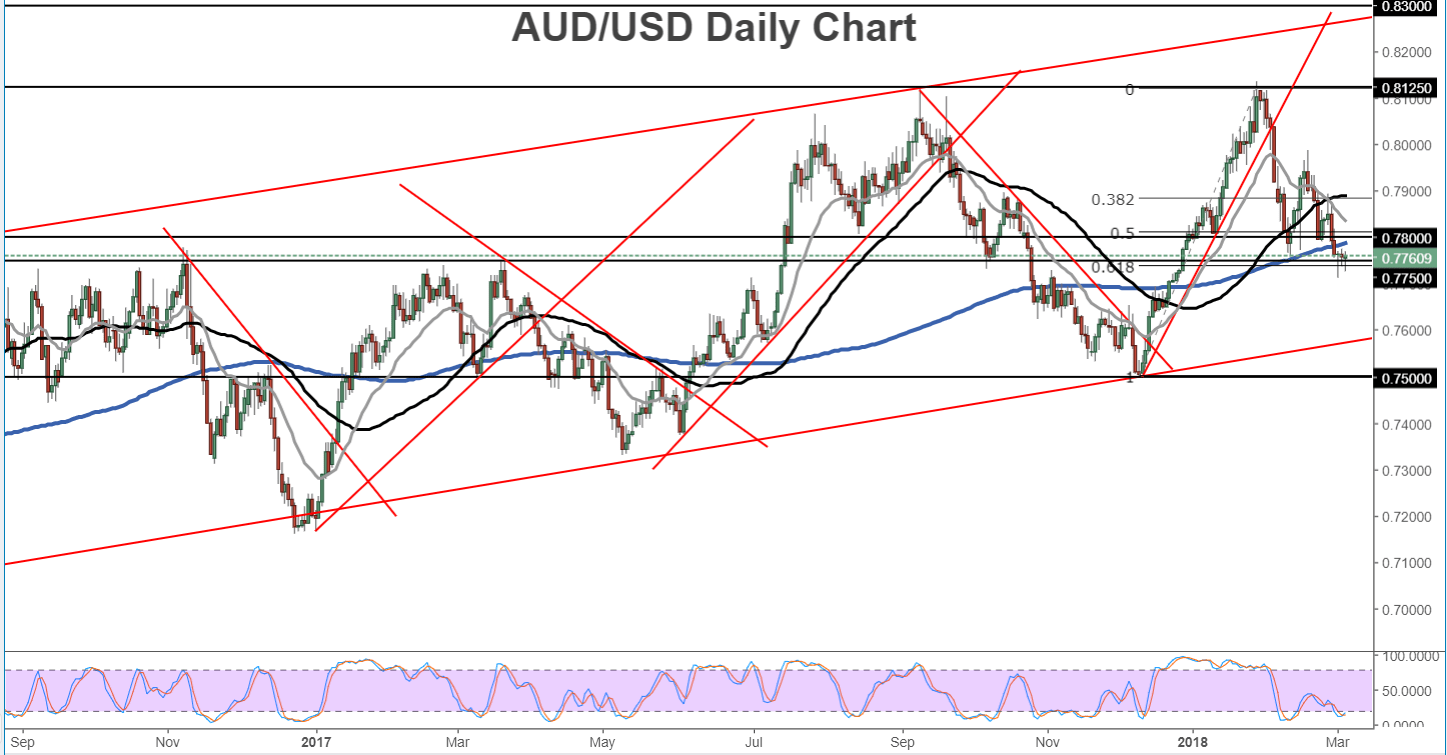

From a technical perspective, AUD/USD has dropped down to fluctuate around the key 0.7750 support area, which is also around the 62% Fibonacci retracement of the December-January bullish run. With any continued downside momentum amid Tuesday’s Australian releases, as well as Friday’s potentially critical US jobs report, a further support breakdown for AUD/USD could begin pressuring the currency pair towards its next major support target around 0.7500.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Dollar articles

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM

February 2, 2024 02:00 PM