AUD NZD Home home on the range

We’re seeing mixed performance in the foreign exchange market today, with the greenback rallying against most of its rivals (prominently including pound sterling and all […]

We’re seeing mixed performance in the foreign exchange market today, with the greenback rallying against most of its rivals (prominently including pound sterling and all […]

We’re seeing mixed performance in the foreign exchange market today, with the greenback rallying against most of its rivals (prominently including pound sterling and all of the commodity dollars) but drastically trailing its biggest rival, the euro. Until this muddled performance shakes out into a one-sided trend for the greenback, some traders may want to explore other currency crosses, including AUD/NZD.

Over the last three months, the antipodean pair has been clearly rangebound in the 500-pip range from 1.0900 to 1.1400 as traders weigh the differences between to the two closely related economies. Of course, both Australia and New Zealand are heavily dependent on China, the region’s powerhouse. With that country slowing, both the Australian and New Zealand dollar are taking it on the chin against other currencies, but the most recent data from the CIA World Factbook (2013) suggests that Australia sends 33% of its exports into the maw of the Red Dragon, while New Zealand only ships 20% of its exports to China.

China Verdict: Bearish for AUD/NZD

Other factors to consider when comparing the Aussie against the kiwi include monetary policy and the prices of key commodities. As it currently stands, the RBA is maintaining a dovish posture, though traders are only pricing in a 7% chance of a 25bps cut at the October meeting, according to the ASX’s RBA Rate Tracker. In contrast, the RBNZ is widely-expected to cut another 25bps in its October meeting on the back of slow growth and weak inflation data. On the monetary policy front at least, markets appear to be favoring the Australian dollar.

Monetary Policy Verdict: Bullish AUD/NZD

When it comes to commodities vis-à-vis AUD/NZD, the key ones to watch are industrial metals (for Australia) and dairy products (for New Zealand). With China seemingly slowing across the board and the US dollar rallying, it’s not surprising that each of these major commodity classes have been walloped of late. Iron ore prices are down close to 60% over the last 18 months, hurting Australia’s terms of trade dramatically, though iron shows signs of stabilizing in the $50-60 region over the last six months.

Meanwhile, diary prices have seen a similarly precipitous drop, though each of the last three semimonthly Global Dairy Trade (GDT) auction results have shown 10%+ rises in dairy prices. If maintained, these recent moves moderately favor the kiwi, though we’re hesitant to read too much into such a volatile data release.

Commodity Price Verdict: Moderately Bearish AUD/NZD

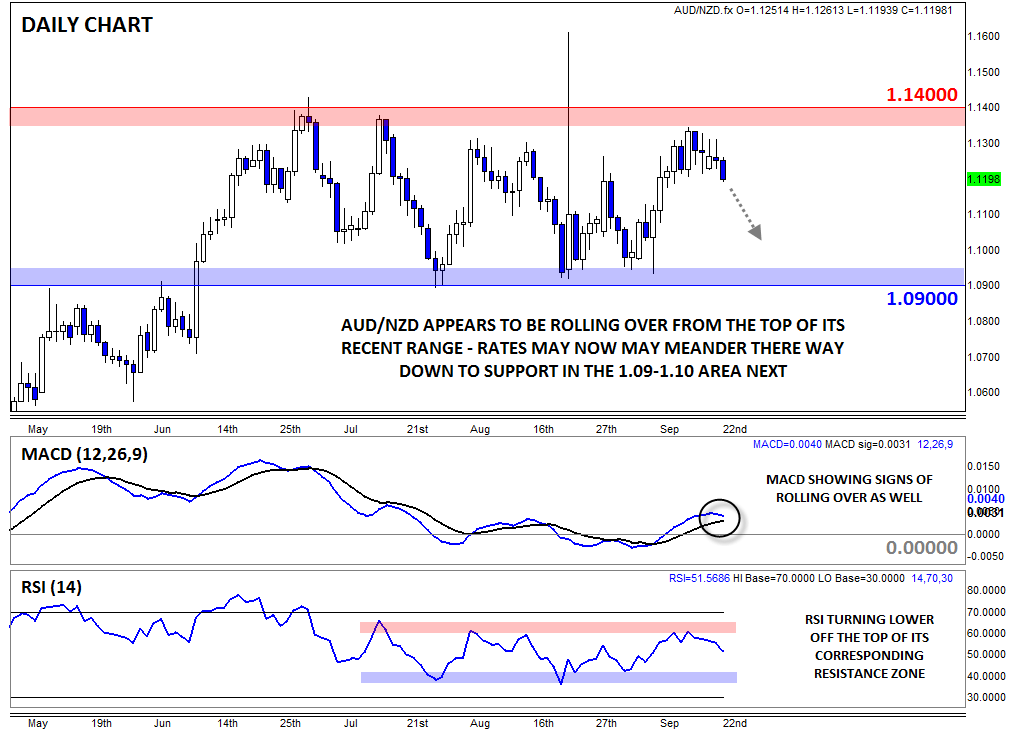

So bringing these three fundamental factors together, we have a fairly mixed picture of outlook for AUD/NZD. In the long-term, we could certainly make a case for AUD/NZD to head lower, but in the here and now, price action will remain key. On that front, the pair appears to be rolling over after nearing the top of its range in the 1.13-14 zone, a move reflected in both the MACD and RSI indicators as well. Therefore, we wouldn’t be surprised to see AUD/NZD meander its way down to the bottom of its recent range in the 1.09-1.10 region over the next few weeks.

Source: City Index

Source: City Index