AUD CAD testing 2 5 year bear trend

The AUD/CAD may not be on the watch list of many traders, but this cross may have formed a major low and about to make […]

The AUD/CAD may not be on the watch list of many traders, but this cross may have formed a major low and about to make […]

The AUD/CAD may not be on the watch list of many traders, but this cross may have formed a major low and about to make significant gains in the days and weeks to come. It has been supported not only by continued weakness in the CAD, owing to weaker oil prices and disappointing Canadian data, but also due to a stronger AUD. The Aussie was the only major currency last month that rose against the US dollar, as my colleague Matt Weller reported earlier. It has been underpinned by stronger Australian data and after the Reserve Bank of Australia dropped its previously dovish stance to turn neutral. Overnight, the RBA kept interest rates and forward guidance effectively unchanged from the previous meeting. We also had some stronger Australian data as building approvals unexpectedly rose 3.9% in October. Meanwhile the latest manufacturing and non-manufacturing PMI data out of China were mixed and this helped to alleviate concerns about the health of the world’s second largest economy, which also happens to be Australia’s largest trading partner. In contrast, the Canadian GDP was abysmal: it showed a month-over-month contraction of half a per cent, no less. The Bank of Canada is still unlikely to cut interest rates tomorrow, though it may prepare the market for future rate cuts after the unexpectedly sharp contraction in GDP.

Canada has another problem: crude oil, which has continued to be sold at the start of this week in a very volatile intra-day manner. The extreme volatile price action is understandable given that the OPEC meetings are just a few days away now. No one wants to be caught on the wrong side of a big move, so both the buyers and sellers are evidently booking quick profit each time the oil market makes money available to them. But the overall feeling is that the OPEC will not make any changes to its production quota on Friday, meaning that the global surplus will remain in place for some time yet. For that reason, oil prices are generally drifting lower and the selling could accelerate in the likely event that the OPEC maintains status quo. So the outlook for the Canadian dollar remains pretty much bleak.

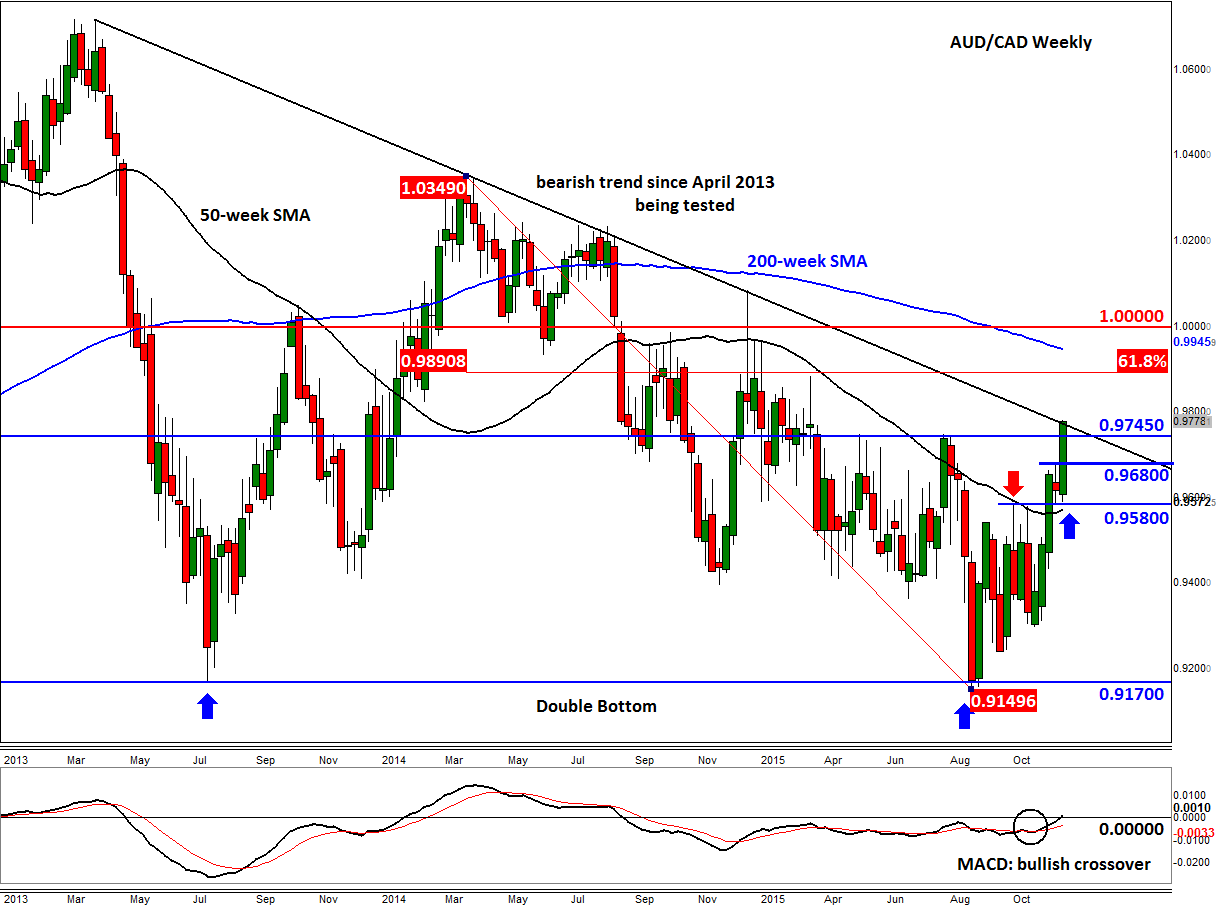

And things could go from bad to worse for the AUD/CAD bears should a 2.5-year bearish trend break down now. As can be seen from the weekly chart, the trend, which has been in place since price made a top in April 2013, comes in around 0.9800. It is important to note that a break above this trend line would validate the double-bottom pattern that was established at 0.9150/70 at the end of the summer. So it will be a significantly bullish development.

The AUD/CAD has already broken above the previous highs of around 0.9745 today. This level could turn into support upon retest. Further supports come in around 0.9680 and then 0.9580: levels that were previously resistance. On the upside, the next potential resistances are at 0.9890, the 61.8% Fibonacci retracement level, followed by the 200-week moving average, at 0.9945, and then parity (1.0000). But given the abovementioned technical developments, I wouldn’t be surprised if the AUD/CAD goes a lot higher than parity over time, especially if the crude oil weakness persists.

For the bullish technical outlook to become invalid, the AUD/CAD will first and foremost need to hold below the bearish trend on a weekly basis. Then the bears must push it below key supports at 0.9745, 0.9680 and then 0.9580. For 0.9580 to break down, it would probably require oil prices to stage a significant rally this week (which is possible of course) or the Bank of Canada to sound surprisingly hawkish tomorrow (unlikely in our view).