November 9, 2020 10:50 PM

Providing further research confirms the vaccine is safe, the companies will seek emergency use authorisation by year-end, before a potential rollout in 2021. Offshore equity markets for the better part reacted positively. In the interest rate space, U.S. 10yr bond yields rallied 10.5bp, to 0.92%.

The rally in bond yields explaining why the interest rate sensitive NASDAQ bucked the trend to finish the session -2.16% lower. On the other hand, higher yields the catalyst for the European Banks Index to breathe a sigh of relief and finish up over 12% on the day.

A move that is being partially replicated in Australia today. The “Big 4” Australian banks that make up about 20% of the ASX200 are trading ~5.50% higher at the time of writing. Also helping the ASX200, a rise in the NAB business confidence index to its highest level since May 2019 in response to the emergence of Victoria from lockdown and falling COVID19 case numbers.

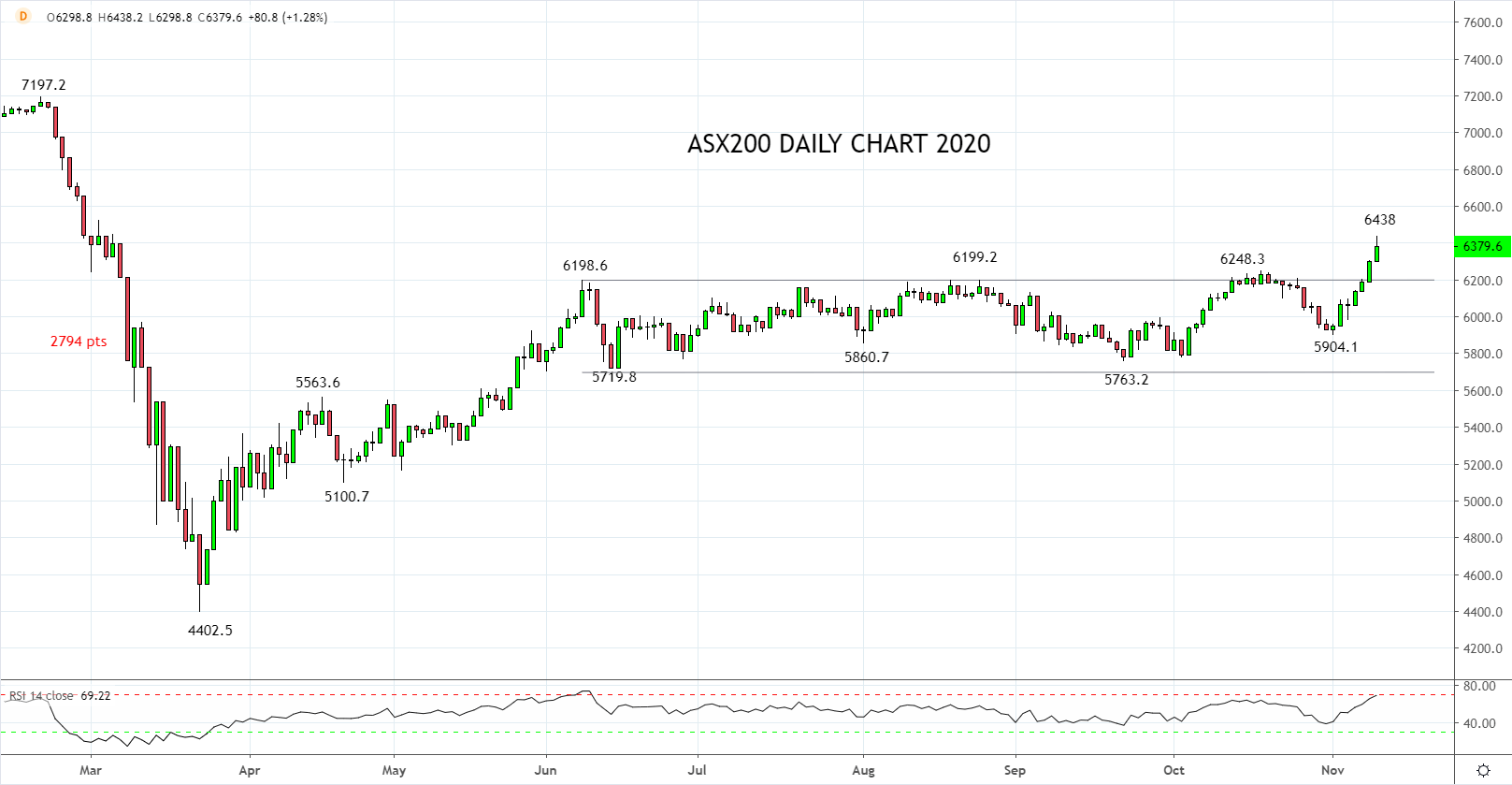

All of this has provided further support to the idea on the ASX200 contained in our last article here where we suggesting adding to core long ASX200 positions in expectation of a test and break above 6200.

With the break above 6200 now cemented, it's an opportune time to return to the chart of the ASX200 from 2017 to gauge how far the rally can run.

In 2017, after breaking out of the top of a five-month range, the ASX200 rallied almost 5% in just under one month. If similar were to occur in 2020 it would project a move towards 6500 by Mid-December, about the time the Santa Clause rally kicks in!

In a nutshell, providing the ASX200 holds above support, formerly resistance 6200/6150 area, supported by a rotation back into the banks, the prognosis for the ASX200 remains bullish into year-end with potential towards 6500 and then 6800.

Source Tradingview. The figures stated areas of the 10th of November 2020. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Yesterday 11:23 PM

Yesterday 10:19 PM

Yesterday 08:00 PM

Yesterday 04:54 PM

Yesterday 01:15 PM

Latest ASX articles

Yesterday 10:19 PM

April 10, 2024 11:24 PM

April 9, 2024 11:02 PM

April 4, 2024 10:28 PM