Associated British Food shares sour on soggy sugar price

Shares of the owner of high street discount fashion chain Primark weakened today because the holding company continues to be buffeted by exposure to its […]

Shares of the owner of high street discount fashion chain Primark weakened today because the holding company continues to be buffeted by exposure to its […]

Shares of the owner of high street discount fashion chain Primark weakened today because the holding company continues to be buffeted by exposure to its core food commodity business.

It’s arguably another signal to Associated British Foods from the market that the incongruity of core food processing operations alongside a sizeable chain store business is not sitting particularly well with investors.

AB Foods reiterated guidance for the financial year, flagging adjusted earnings per share for the financial year to 13th September to be more than the 98.9p posted in 2012-13.

However ABF’s stock loss approached 6% earlier as the world’s second-largest producer of sugar also said the adverse effect of weak sugar prices and a £50m hit from the relative strength of sterling would cancel out strong operating profits from Primark, and the groceries business and improvement in its ingredients operation.

According to Thomson Reuters, the average price for raw sugar in 2014 is about $0.17 per pound with the data provider noting this is below the average cost of production.

Additionally, a forthcoming removal of quotas in 2017 has stoked competition amongst European producers jostling for growth in new markets.

“We saw a big decline in full-year 2013-14 (sugar revenue and profit); we’re going to see a further decline in full-year 2014-15,” AB Foods Finance Director John Bason told Reuters.

With the sugar division making adjusted operating profit of £435m in 2012-13, it is arguable the market may be beginning to query if sugar in particular, and perhaps food operations broadly speaking, ought to merit less management time and resources in view of their recent returns.

By contrast, AB Food’s Primark chain is expected to produce full-year revenues that are 17% higher than the year before with currency rates stripped out from calculations.

It’s worth pointing out, in the six months to 1st March, ABF’s retail operations accounted for three-fifths of group operating profit versus less than 50% the year before.

In other words, if it were not for the weight from the sugar operations, it’s very possible there would have been no need to warn the market today.

ABF noted its ramped up retail selling space to 1.2m square feet, is expected to help bring an estimated 4.5% rise in same-store sales and a full-year operating profit margin forecast to be in the black.

Growth is also expected to be “good” ABF said in grocery brand operating profit, including Kingsmill bread and Twinings tea; and growth in ingredients will also beat the year before under flat-currency conditions, ABF said.

The group’s pure-play ingredients, sweetener and food rivals are far ahead of it in yield terms with ABF’s prospective yield trailing at 1.1% against the average of 3%.

Cost of capital is already a win judging by debt-to-equity, with ABF’s peers soaking up credit at a rate of 74.2% to equity in the last twelve months, whilst ABF traded on 18.8%.

At the same time, sugar is distorting the market’s perception of the overall group, if we give credence to the forward price-to-earnings multiple now coming out at a near-meaningless 27.2 times, versus general retailer Marks & Spencer’s at 12.8.

It’s easy to wonder what price-to-earnings ratio the market would apply to ABF if it were judged more as a retailer, say against Marks & Spencer, which has posted 12 consecutive quarters of declining general merchandise.

The foregoing may be one reason for an ‘incongruity discount’ on Associated British Foods shares.

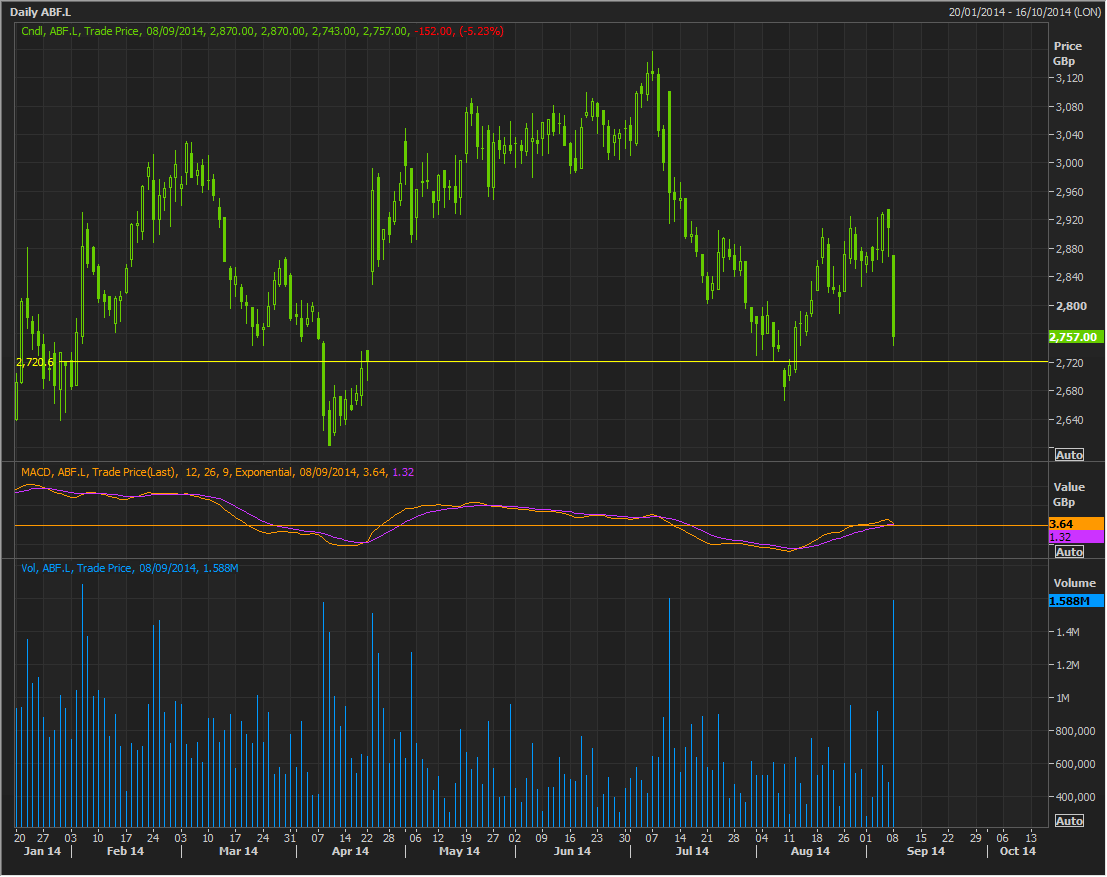

As we can see, today’s fall may have at least a little way to run, going by the obvious means: note the Moving Average Convergence Divergence system is currently heading below the zero line.

I’ve added a line of support at 2720p. It may have some merit by default, given the uptick in sellers today (note the volume bars in blue).

Today’s volume spike may suggest most activity in the name for the near term has already taken place.