ASOS shares spike on low cut expectations

Updated 1403 BST ASOS stock is enjoying one of its infamous spikes on Wednesday, after beating fairly easy expectations. The online-based purveyor of affordable fashion […]

Updated 1403 BST ASOS stock is enjoying one of its infamous spikes on Wednesday, after beating fairly easy expectations. The online-based purveyor of affordable fashion […]

Updated 1403 BST

ASOS stock is enjoying one of its infamous spikes on Wednesday, after beating fairly easy expectations.

The online-based purveyor of affordable fashion sashayed past The City’s average EPS forecast of about 14.6p with earnings of 17.6p.

But as has been the case for as long as I can remember, ASOS’s bottom line looks great when you first take it out of the wrapping, but less so on closer examination.

So for instance, a consensus forecast of H1 2015 half-year pre-tax profit, compiled by Thomson Reuters, showed the average expectation was a lenient £16.3m.

ASOS beat this by coming in at £18m.

But that is still 10% lower than the same period a year ago.

On even closer inspection, it becomes apparent that even this relative outperformance needs to be taken with a pinch of salt.

ASOS revealed elsewhere in its statement that an insurance reimbursement for the warehouse fire last year in fact accounted for £6.3m of its first-half profit before tax.

Therefore, the underlying fall in pre-tax profit was a much more difficult to downplay 41.8% to £11.7m

Make no mistake, I have warmed a great deal to ASOS CEO Nick Robertson and his long-standing management team, who more than proved their mettle during a horrendously challenging 2014 for the firm.

And much of the delayed profit growth ASOS displays can partly be explained by continued recuperation and laudable investment in distribution, systems and other long-term advantages.

However, such initiatives as the “continued investment in our international price competitiveness gaining traction” Robertson boasts of in today’s statement just bring me back to where my misgivings start.

The impact from this ‘investment in price’ (cuts) in the half year was a 230 basis point gross margin contraction, with the increased investment in distribution capacity also weighing, though how much should be attributed to each factor isn’t made clear.

But whilst Robertson looks past this softness, instead taking “confidence in the outlook for the second half”, the timeframe over which we should expect these sorts of initiatives and ASOS overall to show sustainable profitable growth remains unspecified.

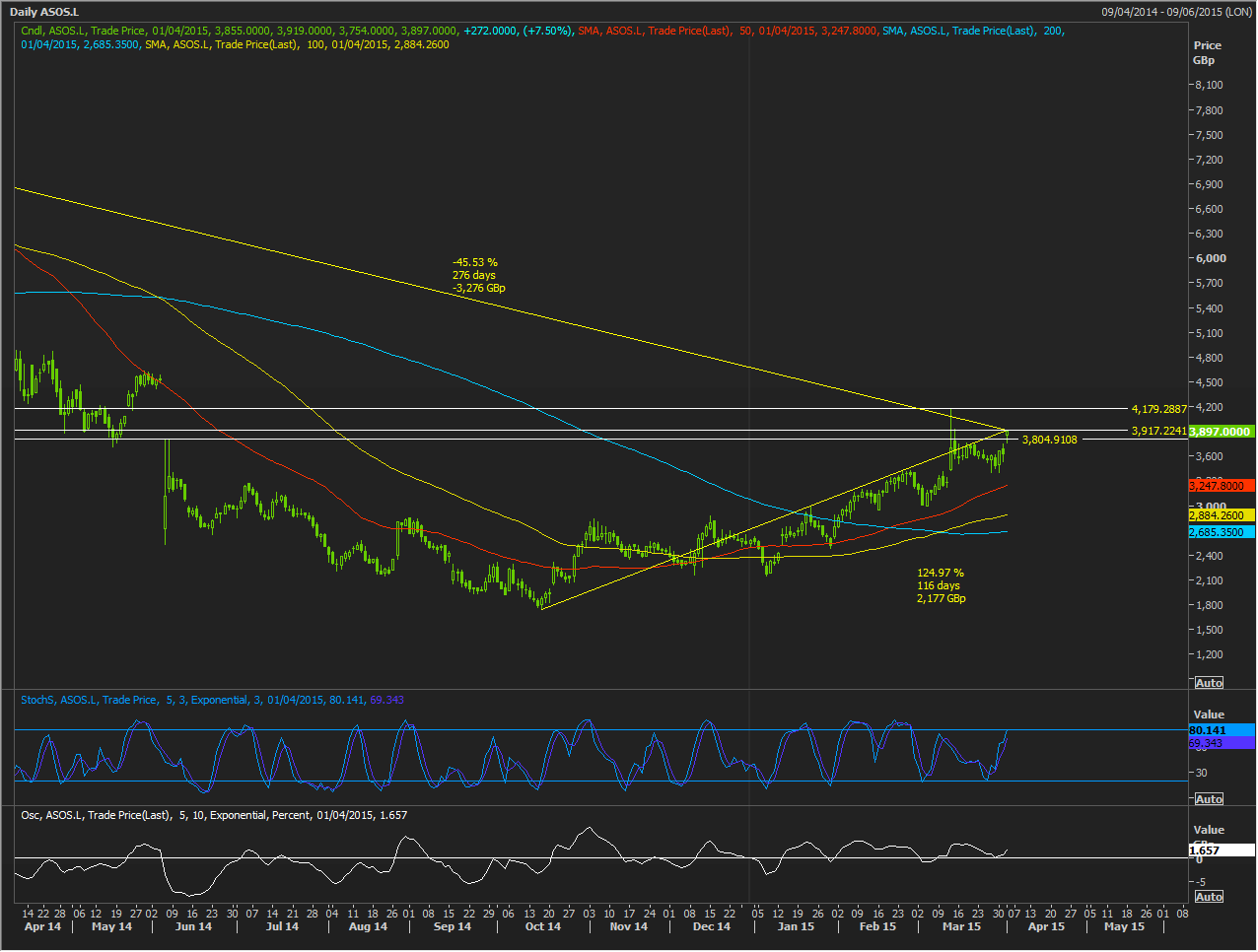

In a nutshell, that’s why ASOS is a wild high-beta stock matched on that metric over 5 years by few comparable retailers, save for Ocado.

This high volatility has left the stock 45% lower than its high in February 2014, even after it bounced by more than 125% off a bottom hit in October!

In an alternative world, such instability ought to burst the market’s inflated optimism on ASOS stock, measured by a price/earnings ratio that swerves in the high 80s.

Within a raft of similar high street and superhighway fashion merchants, ASOS leads average PE by 90%.

Instead, we know the real world is in fact the ‘alternative’ universe (for more conservative investors).

And it’s one in which for some ‘growth stocks’, optimism needs little fundamental basis, especially in the face of real wins of the like ASOS reported today—H1 retail sales ascending 17%, stripping out currency effects, and international sales up a solid 10%.

On such days, the gap to the stock’s next visible challenge looks do-able, even if the give-back is typically as easy as ASOS’s returns policy.

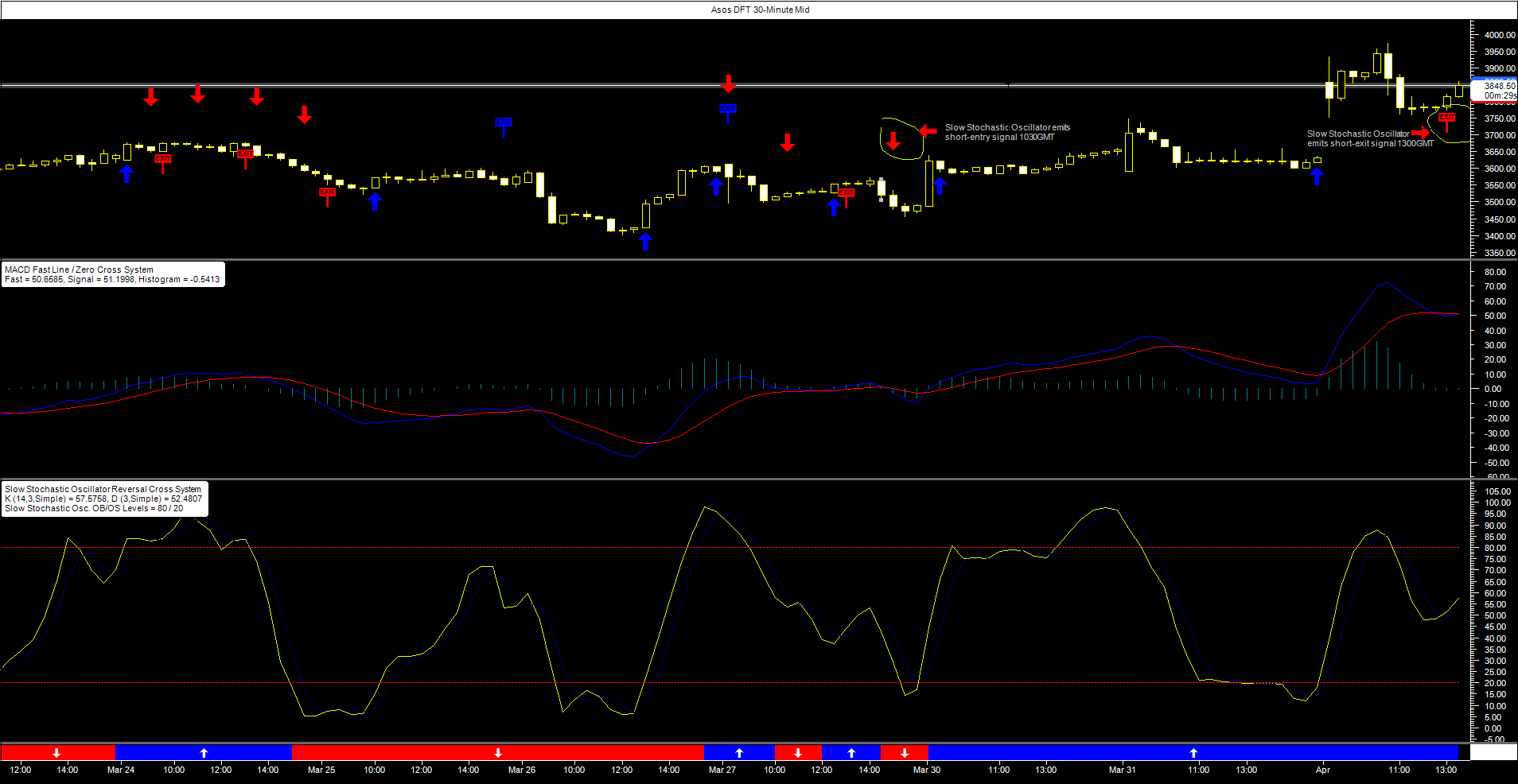

However, more than half way into Wednesday’s session, the Slow Stochastic Oscillator trading system attached to a chart of City Index’s ASOS Daily Funded Trade, emitted a signal to exit short positions.

This negated a ‘sell’ signal issued by the system during the half-hourly interval between 1030 and 11 AM.

The system’s moving average lines were well within acceptable bounds and pointing upwards, providing reasonable grounds for further short-term strength in the title.