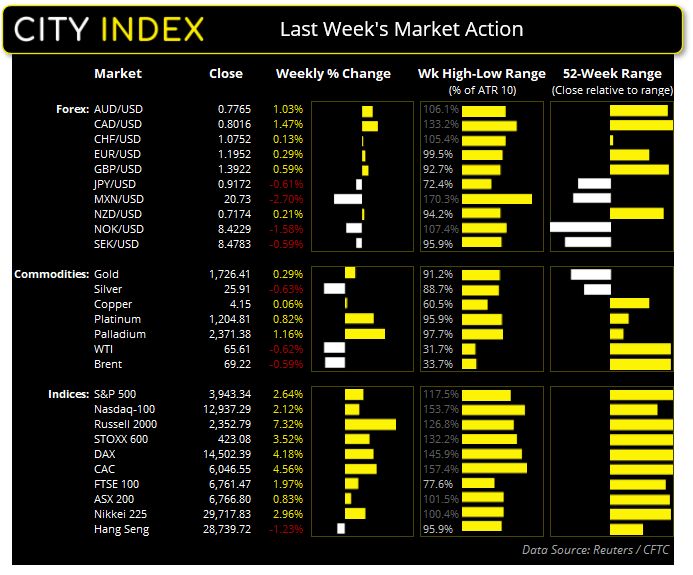

Asian Futures:

- Australia’s ASX 200 futures fell -3 points (-0.04%), the cash market is currently estimated to open at 6763.8

- Japan's Nikkei 225 futures fell -60 points (-0.2%), the cash market is currently estimated to open at 29657.83

- Hong Kong's Hang Seng futures rose 43 points (0.15%), the cash market is currently estimated to open at 28782.72

European Friday close:

- UK's FTSE 100 index rose 24.51 points (0.36%) to close at 6761.47

- Europe's Euro STOXX 50 index fell -12.28 points (-0.32%) to close at 3833.36

- Germany's DAX index fell -67 points (-0.46%) to close at 14502.39

- France's CAC 40 index rose 12.79 points (0.21%) to close at 6046.55

US Friday close:

- The Dow Jones rose 293.04 points (0.9%) to close at 31,496.30

- The S&P 500 rose 4 points (0.1%) to close at 3,943.34

- The Nasdaq 100 fell -115.606 points (-0.9%) to close at 12,937.29

Indices:

It was a strong finish for equites overall last week, even if the technology sector did have its ups and downs. Small caps led the surge with the Russell 2000 closing at a new record high and rallying over 7% amid its second most bullish week this year.

The S&P 500 couldn’t quite manage a new high but closed just beneath it, having found support above 3,900. And, if sentiment allows, it could test 4,000 this week.

The Nasdaq 100 remained a slave to rising bond yields, closing just under -1% on Friday but held support at 12,726. Still, it held up well considering the new highs across the yield curve, and that we have seen the index fall over 4% recently under similar circumstances.

Australia’s ASX 200 has remained in a 200-point range for the past three weeks. To trend traders that’s extremely boring. But mean reversion traders, who seek to sell at highs and buy at lows, have no doubt had a blast and may well continue to do so until it inevitably breaks out of said range. Going into this week, daily support sits around 6,658 and resistance around 6,860. A break below 6,658 brings the 6,6511.40 low into focus, but we wouldn’t look to be too bullish on the daily timeframe until prices clear above the 2021 high at 6,338.

Forex: 100-day eMA comes to the dollar’s rescue

The US dollar index (DXY) close on its 200-day eMA and found support at 91.40, and we expect it to be a pivotal level this week. The weekly candle was also a bearish spinning top which suggests a hesitancy to continue its counter-trend rebound. A break beneath the candle’s low suggests we could then see AUD and NZD go on to break to new highs.

The Canadian dollar was the strongest major last week. It was already performing well but the strong employment report on Friday gave it another boost heading into the weekend. The Australian dollar was the second strongest major and the Japanese yen was the weakest.

- AUD/JPY and AUD/CHF have both paused near resistance levels (the May 2018 and April 2019 highs respectively).

- AUD/USD held above 0.7622 support and closed with a bullish inside week. Friday closed on its 20-day eMA with a bearish bar, so perhaps there’s room for a retracement before retesting its 0.7820-27 resistance zone.

- NZD/USD produced a bearish outside candle on Friday and closed beneath its 50-day eMA. A break below 0.7096 suggests the decline from the 0.7465 high is set to continue and brings 0.6940 support into focus.

- NZD/CHF continues to coil within a symmetrical triangle after Thursday’ false break higher. Whilst the bias is for a bullish breakout (in line with the daily trend) a downside breakout can make an equally good setup as it catches traders by surprise as it unravels with a deeper correction.

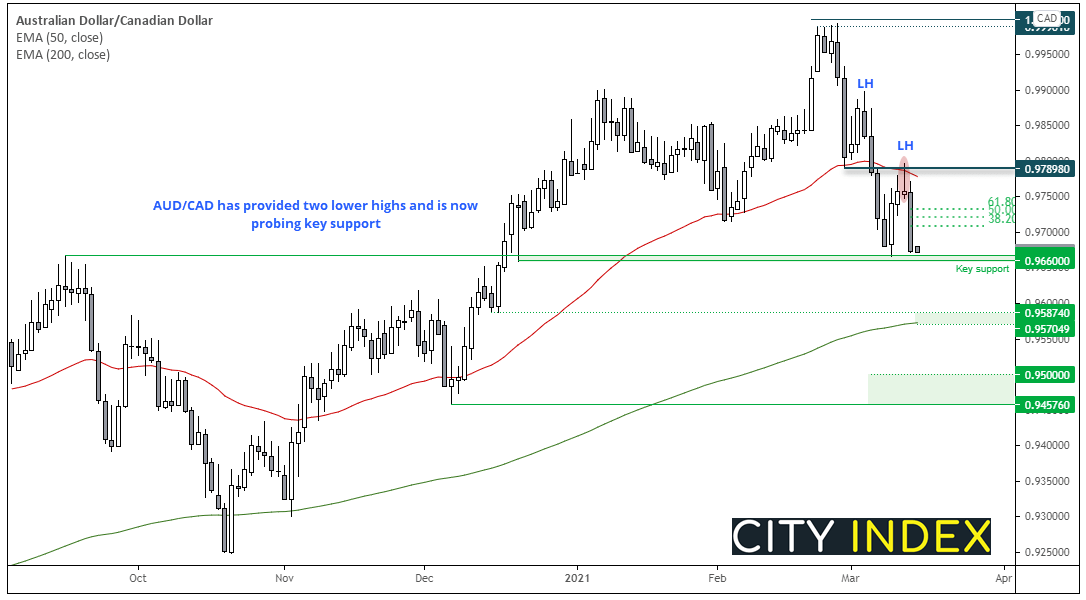

AUD/CAD probes key support

Despite the Australian dollar’s strength elsewhere, it continues to be outperformed by the Canadian dollar. Since it failed to retest parity in February the daily chart has been trending lower and formed two prominent lower higher. Thursday’s candle produced a small bearish pinbar at the 50day eMA before Friday’s large bearish candle and prices are now hovering at a key support level.

The bias is for an eventual break below 0.9660 support but a minor bounce from current levels would not come as much of a surprise.

- Bears could wait for a break beneath 0.9660 before entering, or wait to see if broken support then becomes resistance

- The bias remains bearish below Thursday’s high but risk management could be fine turned using Fibonacci ratio’s of Friday’s bearish candle.

- The eventual target is just above December’s low and the 0.9500 handle but we may find the 200-day eMA provides an interim target

Commodities: Gold bounces of 1700

Gold hit our counter-trend bearish target of 1700 on Friday and quickly rebounded to close the week at 1726.96. Whilst prices remain above 1700 our bias is for a retest of 1760. The weekly chart remains at the lower trendline of a bearish channel but produced a two-week bullish reversal (bullish piercing pattern) and Friday’s candle was a bullish pinbar.

Friday’s range on WTI was so small on Friday it was its least volatile session in over one year. Closing -0.7% lower and below the April 2019 high, prices are now under compression. However, we remain bullish above the $63 (Wednesday’s low) as it forms part of a 3-day bullish reversal pattern (morning star reversal). A break above Friday’s high brings $70 back into focus.

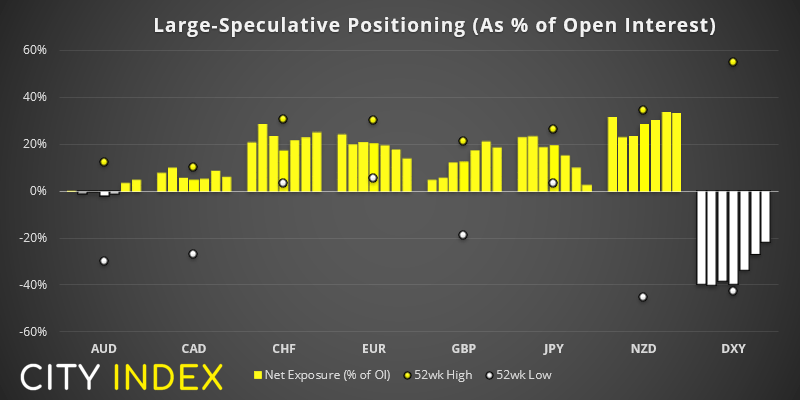

As of Tuesday the 9th of March:

- Net-long exposure to Euro futures were their least bullish in 8 months. Gross short interest rose for a seventh consecutive week and is at a 12-month high.

- Net-long exposure to gold futures fell to their lowest level since June 2019. (Incidentally, the last time net-long was this low it was the start of a large rally). However, gross longs are declining and gross shorts are rising.

- Traders are net-long Japanese yen futures by just 6.5k contracts, their least bullish net exposure in 12 months. Short exposure has risen to a 12-month high.

- Net-long exposure to DXY futures (US dollar index) has risen to a 10-mnonth high, reducing the net-short exposure to its least bearish level this year. However, gross-short exposure continues to rise.

- Bullish interest for NZD futures are flying at their highest level since August 2018. Hardly any short interest and gross longs continue to rise.

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM