Asian Futures:

- Australia's ASX 200 futures are up 27 points (0.37%), the cash market is currently estimated to open at 7,396.50

- Japan's Nikkei 225 futures are up 120 points (0.4%), the cash market is currently estimated to open at 30,128.19

- Hong Kong's Hang Seng futures are up 148 points (0.58%), the cash market is currently estimated to open at 25,864.00

UK and Europe:

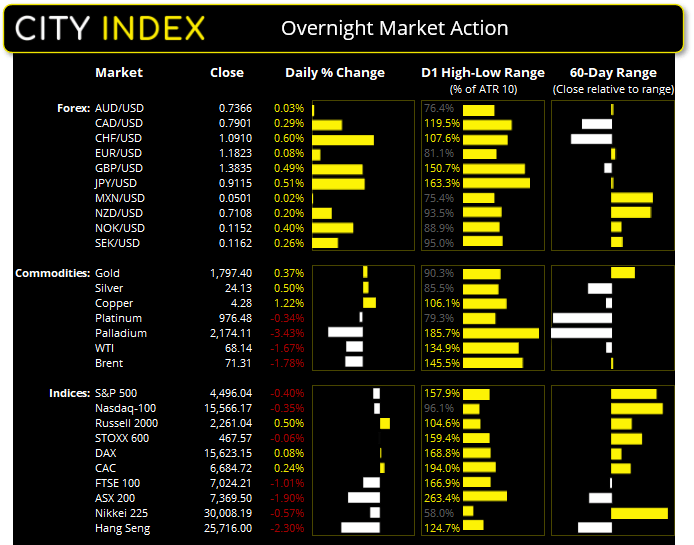

- UK's FTSE 100 index fell -71.32 points (-1.01%) to close at 7,024.21

- Europe's Euro STOXX 50 index fell -0.04 points (0%) to close at 4,177.11

- Germany's DAX index rose 12.87 points (0.08%) to close at 15,623.15

- France's CAC 40 index rose 15.83 points (0.24%) to close at 6,684.72

Thursday US Close:

- The Dow Jones Industrial fell -151.69 points (-0.43%) to close at 34,879.38

- The S&P 500 index fell -20.79 points (-0.47%) to close at 4,493.28

- The Nasdaq 100 index fell -59.8 points (-0.38%) to close at 15,561.05

Learn how to trade indices

Indices: Wall Street edges lower once more

US jobless claims approached an 18-month low, with initial claims shedding -35k and continual falling -20k. Yet whilst it takes the edge of a weaker than expected NFP print, it doesn’t fully make up for it given just 235k were added compared to the 720k expected, and that was reflected in equity markets which were lower for a fourth consecutive session. The S&P 500 was down -0.27% although continues to hold above its 20-day eMA. 6 of its 11 sectors were lower, led by real estate and consumer staples whilst financials and healthcare supported the broader market, so quite balanced in the grand scheme of things.

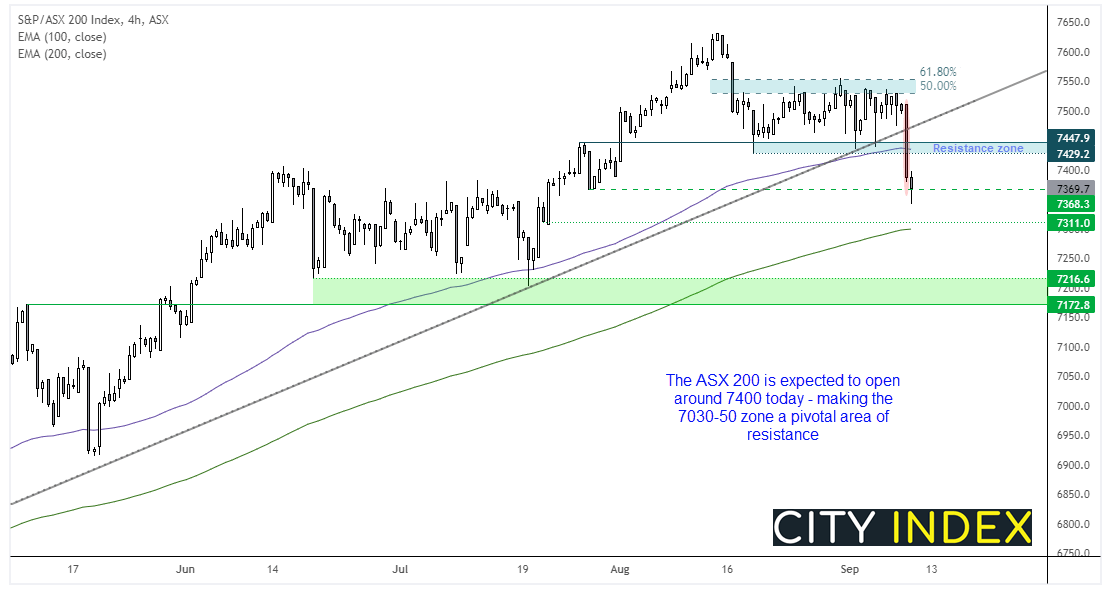

It wasn’t the best day for bullish ASX 200 traders yesterday, with the large cap index failing -1.9% during its worst session in 4-months, causing the ASX 200 VIX index (AXVI) to rise to a near 2-month high. It was a -2 standard deviation day, but it is worth noting that single -2SD days haven’t usually triggered an extended sell-off during this bull trend. But then to counter that, if this is a turning point, then the dynamics have changed and the -2SD day may be a red flag for bulls.

From here we’d like to see the 7430 area hold as resistance for potential bearish setups over the near-term. Futures markets are pointing to a positive open and the AXS open around 7400, so it leaves a little wriggle room for upside early on for bears to consider fading into before gunning for 7300 and maybe the 7200 support zone.

ASX 200 Market Internals:

ASX 200: 7369.5 (-1.90%), 09 September 2021

- Energy (0.04%) was the strongest sector and Information Technology (-3.18%) was the weakest

- All 11 sectors closed lower

- 6 (3.00%) stocks advanced, 190 (95.00%) stocks declined

- 9 stocks hit a new 52-week low

- 65% of stocks closed above their 200-day average

- 58.5% of stocks closed above their 50-day average

- 34.5% of stocks closed above their 20-day average

Outperformers:

- + 1.84% - Resmed Inc (RMD.AX)

- + 1.38% - Whitehaven Coal Ltd (WHC.AX)

- + 0.42% - Elders Ltd (ELD.AX)

Underperformers:

- -7.93% - Virgin Money UK PLC (VUK.AX)

- -6.32% - Orocobre Ltd (ORE.AX)

- -5.71% - EML Payments Ltd (EML.AX)

Forex: Dollar down as ECB (kind of) tapers

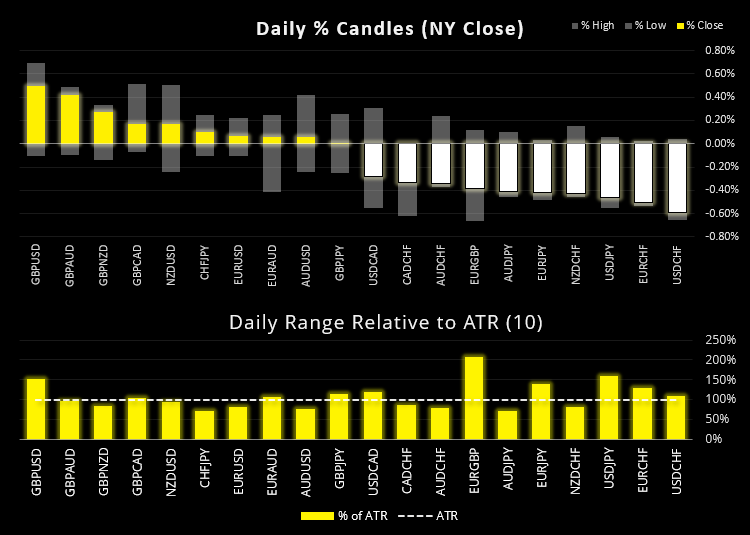

The ECB slowed the pace of their bond buying in a move which President Lagarde described as “recalibrating PEPP”. Call it what you will, but the euro benefitted, even if only marginally so. A bullish inside day formed and held above 1.1800 yet closed below its 50-day eMA. So hardly an explosive session.

A bearish engulfing candle formed on the US dollar index (DXY) and closed below its 20-day eMA. Form here we want to see if 92.3 can hold as support before it moves higher once more, in line with its rally from the 200-day eMA.

AUD/USD held above the 20-day eMA for a second session and formed an inside day / Doji, so signs of stability are present since pull back from the 0.7478 high were the 200-day initially capped as resistance.

GBP/USD erased losses since the UK tax hikes were announced and closed the day as the strongest major and pair we track. A 3-bar bullish reversal (Morning Star) has now formed following its bounce from the 200-day eMA, making it a pair to watch for bulls on the daily chart.

It’s fairly quiet on the data front in today’s Asia session, with electronic card retail sales and migration data kicking off at 08:45 BST.

Learn how to trade forex

Commodities: China dents oil demand

Oil prices were lower on reports China planned to tap into state reserves, denting demand for US crude. WTI continues to hold above 67.12 support whilst a break beneath it suggests a deeper retracement against the rally from 61.56.

Silver is meandering around $24 yet still shows the potential for move lower in line with its bearish trend from the May high. It likely just needs to see a weaker US dollar to help push it over.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM