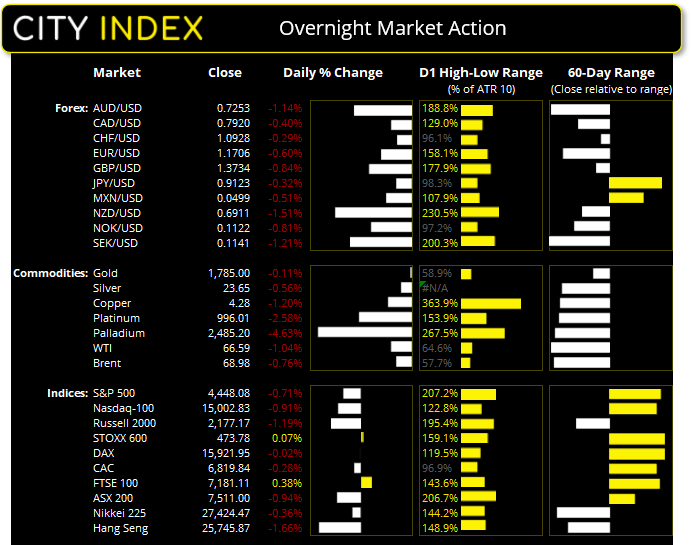

Asian Futures:

- Australia's ASX 200 futures are down -34 points (-0.46%), the cash market is currently estimated to open at 7,477.00

- Japan's Nikkei 225 futures are up 60 points (0.22%), the cash market is currently estimated to open at 27,484.47

- Hong Kong's Hang Seng futures are down -67 points (-0.26%), the cash market is currently estimated to open at 25,678.87

UK and Europe:

- UK's FTSE 100 index rose 27.13 points (0.38%) to close at 7,181.11

- Europe's Euro STOXX 50 index fell -6.04 points (-0.14%) to close at 4,196.40

- Germany's DAX index fell -3.78 points (-0.02%) to close at 15,921.95

- France's CAC 40 index fell -18.93 points (-0.28%) to close at 6,819.84

Tuesday US Close:

- The Dow Jones Industrial fell -282.12 points (-0.79%) to close at 35,343.28

- The S&P 500 index fell -31.63 points (-0.71%) to close at 4,448.08

- The Nasdaq 100 index fell -137.945 points (-0.91%) to close at 15,002.83

Learn how to trade indices

Indices in the red

The risk-off tone set in Asia continued overnight as traders absorbed the fallout and evacuation of Afghanistan, weak China data and the rise in COVID-19 cases. Retail sales also disappointed to further show lack of confidence from consumers (which, if Friday’s weak consumer sentiment was anything to go might have been dollar bearish) although firmer industrial production softened the blow anyway.

But the pattern was simple; sell equites, metals, risker currencies and buy bonds, USD, CHF and JPY. The S&P 500 fell -0.71% to an 8-day low, although recouped around 2/3rd of its early losses after finding support at the 20-day eMA and printing a bullish hammer on the daily chart. 7 of its 11 sectors were in the red, led by consumer discretionary and materials sectors and 70% of its stocks declined. The Nasdaq 100 shed -0.9% with FAANG stocks falling -1.9%.

The ASX 200 extended losses although found support around the 7506.30 high. Sentiment favours a weak start today with next support sitting around 7448, with potential resistance at 7538 and 7582.

ASX 200: Market Internals

ASX 200: 7511 (-0.94%), 17 August 2021

- Healthcare (0.44%) was the strongest sector and Financials (-1.73%) was the weakest

- 7 out of the 11 sectors closed lower

- 54 (27.00%) stocks advanced, 135 (67.50%) stocks declined

- 68% of stocks closed above their 200-day average

- 61% of stocks closed above their 50-day average

- 57.5% of stocks closed above their 20-day average

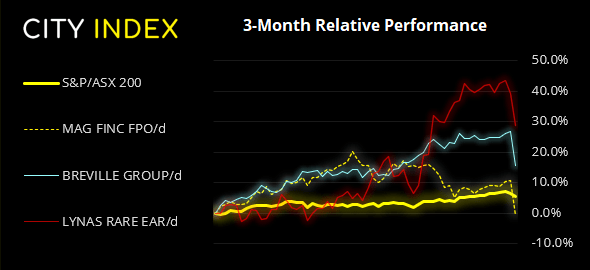

Outperformers:

- + 4.71% - Domain Holdings Australia Ltd (DHG.AX)

- + 3.84% - Steadfast Group Ltd (SDF.AX)

- + 3.76% - Fisher & Paykel Healthcare Corporation Ltd (FPH.AX)

Underperformers:

- -10.1% - Magellan Financial Group Ltd (MFG.AX)

- -8.97% - Breville Group Ltd (BRG.AX)

- -7.59% - Lynas Rare Earths Ltd (LYC.AX)

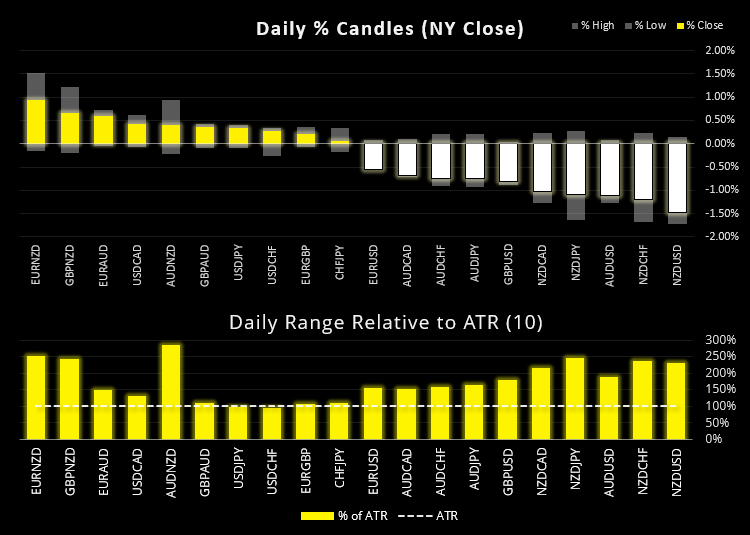

Forex: RBNZ cash rate meeting in focus

New Zealand announced a 3-day lockdown due to a single case detected case in Auckland yesterday, and that just may be a record in terms of the lowest threshold for a government to act. And the way the New Zealand dollar tumbled in response suggests this single case may even prevent RBNZ from hiking rates today – an event which markets had already priced in. The 1-month OIS (overnight index swap) fell from around 0.523 on Monday to 0.44 by Tuesday’s close, which means the probability for a +25 bps hike has fallen from approximately 109% to 76%. So it still appears likely, just not the ‘dead cert’ it appeared to be yesterday.

The US dollar was the strongest major on safe-haven flows, with slightly hawkish (less dovish) comments from Powell overnight saying he’s not certain the Delta outbreak will hamper the economic recovery. Although JPY ad CHF pairs also remain firm overall.

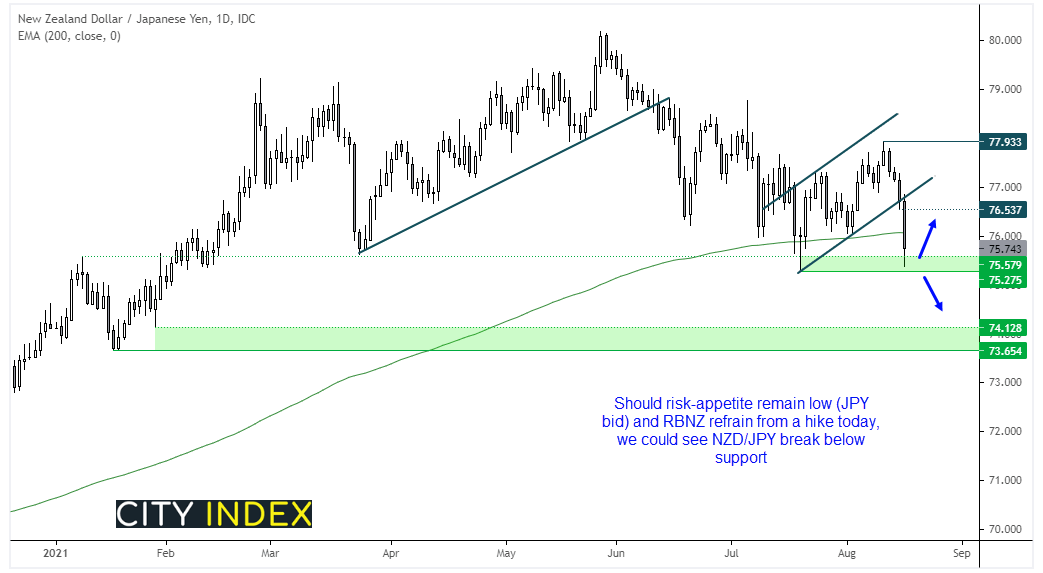

So, this places NZD/JPY into focus for today’s RBNZ meeting. The daily chart has seen bearish momentum accelerate out of a corrective channel and fall just short of the July low. Prices have recovered slightly above the 75.27 – 75.58 support zone, and this area may tempt cheeky longs should RBNZ go ahead and raise rates as originally expected. But, if the yen remains bid due to safe-haven flows and RBNZ pull the plug on a hike today (and not hint at a hike any time soon) then we could see NZD/JPY break below 75.27

Learn how to trade forex

Commodities broadly lower:

The Thomson Reuters CRB commodity basket fell -1.8% to a 5-day low, excluding energy it was still -1.6% lower for the day.

Copper futures fell -1.2% to a 1-month low as the Afghanistan fallout and China data dented sentiment for the bronze metal.

Platinum futures remains below the 20-day eMA and rolled over from the 1021 – 1038 resistance zone mentioned in yesterday’s report. Our bias remains bearish below 1038 although last week’s high could also be used to fine tune risk management.

Gold broke its 5-day winning streak to close marginally lower by -0.12% and formed a small Doji on the daily chart. The stronger dollar acted as a headwind but we were sceptical of an extended bullish run whilst it traded below 1789 – 1800 resistance, so we remain neutral for now.

Silver printed a small bearish candle within the 23.78 – 24.00 resistance zone. Should risk-off sentiment prevail we suspect it will be the ‘next shoe to drop’ behind platinum.

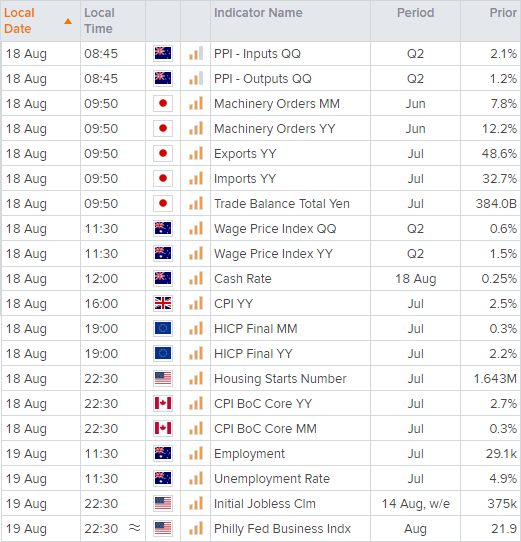

Up Next (Times in BST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 01:15 PM

Today 07:49 AM

Today 04:24 AM

Yesterday 10:48 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM