Asian Futures:

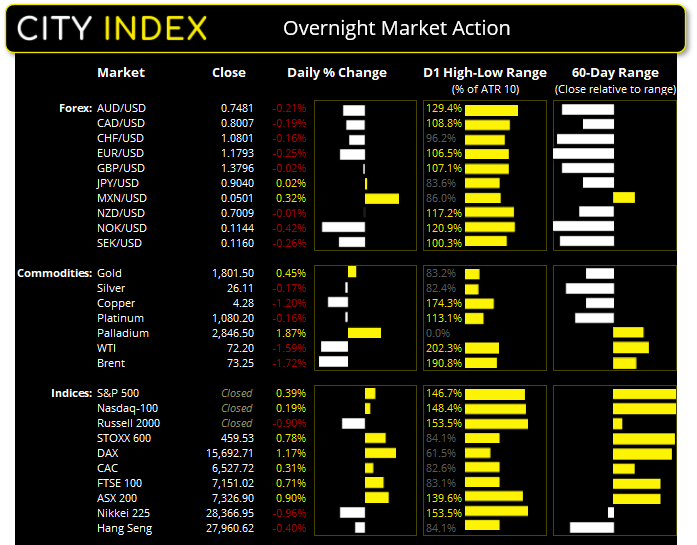

- Australia's ASX 200 futures are down 0 points (0%), the cash market is currently estimated to open at 7,326.90

- Japan's Nikkei 225 futures are down -50 points (-0.18%), the cash market is currently estimated to open at 28,316.95

- Hong Kong's Hang Seng futures are down -6 points (-0.02%), the cash market is currently estimated to open at 27,954.62

UK and Europe:

- UK's FTSE 100 index rose 50.14 points (0.71%) to close at 7,151.02

- Europe's Euro STOXX 50 index rose 25.86 points (0.64%) to close at 4,078.53

- Germany's DAX index rose 181.33 points (1.17%) to close at 15,692.71

- France's CAC 40 index rose 20.24 points (0.31%) to close at 6,527.72

Wednesday US Close:

- The Dow Jones Industrial rose 53.62 points (0.16%) to close at 33,730.89

- The S&P 500 index rose 14.59 points (0.34%) to close at 4,358.13

- The Nasdaq 100 index rose 24.178 points (0.16%) to close at 14,810.54

Learn how to trade indices

Indices like the lack of tapering:

The Fed were more balanced than some had hoped, according to the minutes of FOMC meeting released overnight. And if tapering is not as close as feared, it means there is more easy money sloshing around the financial system to support equity markets.

The S&P rose 0.34% to a new high, with 9 of its 11 sectors rising, led by materials, industrials and healthcare. The Nasdaq closed just 0.16% higher after giving back early gains whilst the biotech sector fell -1.3%.

The ASX 200 produced a bullish engulfing candle yesterday yet remains inside the range of Tuesday’s bearish outside day. The key word here is ‘range’, which is between 7240 – 7345, therefore range-trading strategies being preferred until we see a convincing breakout.

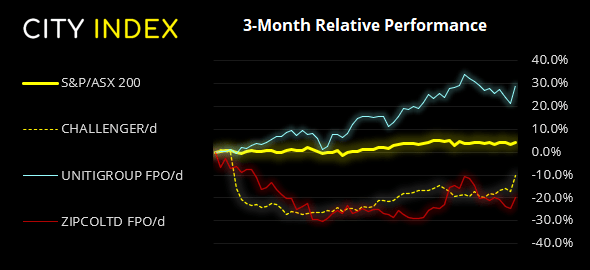

ASX 200 Market Internals:

ASX 200: 7326.9 (0.90%), 07 July 2021

- Information Technology (2.82%) was the strongest sector and Industrials (-0.02%) was the weakest

- 10 out of the 11 sectors closed higher

- 5 out of the 11 sectors outperformed the index

- 142 (71.00%) stocks advanced, 48 (24.00%) stocks declined

- 6 hit a new 52-week high, 0 hit a new 52-week low

- 73.5% of stocks closed above their 200-day average

- 100% of stocks closed above their 50-day average

- 48% of stocks closed above their 20-day average

Outperformers:

- + 8.78% - Challenger Ltd (CGF.AX)

- + 6.69% - Uniti Group Ltd (UWL.AX)

- + 6.48% - Zip Co Ltd (Z1P.AX)

Underperformers:

- -4.83% - Nanosonics Ltd (NAN.AX)

- -3.76% - Whitehaven Coal Ltd (WHC.AX)

- -3.02% - Worley Ltd (WOR.AX)

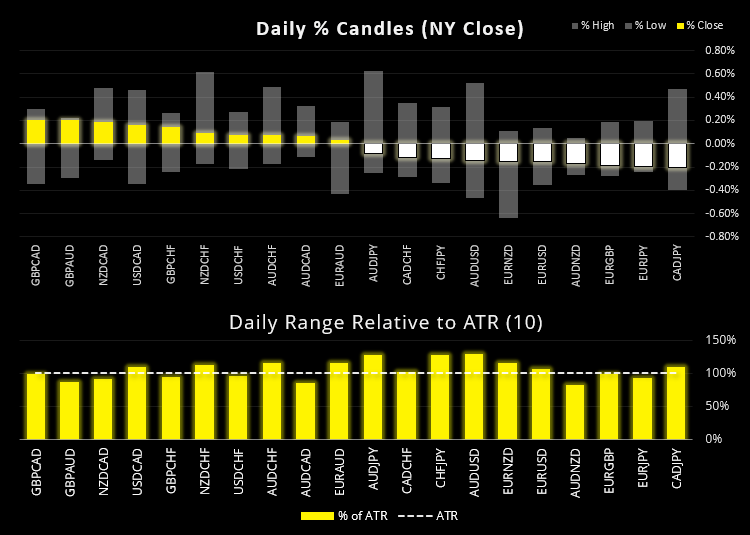

Forex: Lower oil weighs on CAD

We can see on the FX dashboard there were quite a few whipsaws yesterday, where upper and lower wicks accounted for most of the action before closing between +/-0.2% from the open. So not the most decisive of sessions but with volatility comes opportunity.

CAD and EUR were the weakest currencies, GBP and NZD were the strongest. Which is a shame for the Canadian dollar because its Ivey PMI report came in much stronger than expected, rising 71.9 from 64.7 (versus 57.4 forecast). Ultimately, weaker oil prices remain the headwind for CAD and also explain why it is the weakest major currency over the past week.

The US dollar index (DXY) touched a new 3-month high overnight and hit our gap resistance target, before reverting lower to leave some sort of hammer/Doji hybrid. However, it is not a close which denotes extreme-bullish strength, so perhaps majors have some wriggle room for minor gains against the dollar today.

AUD/USD closed beneath its 200-day eMA for a 7th day but is struggling to close beneath the December 21st low. Support levels reside at 0.7443 and 0.7400 with resistance at 0.7580 and 0.7537. AUD/NZD hit a month-to-date low, and bearish momentum increased after finding resistance at its 200-day eMA.

NZD/CAD found support at the 0.8770 breakout level yet also formed a double top at 0.8780. Our bias remains bullish above Tuesday’s low with the initial target being around the 0.8852 high / 200-day eMA.

Learn how to trade forex

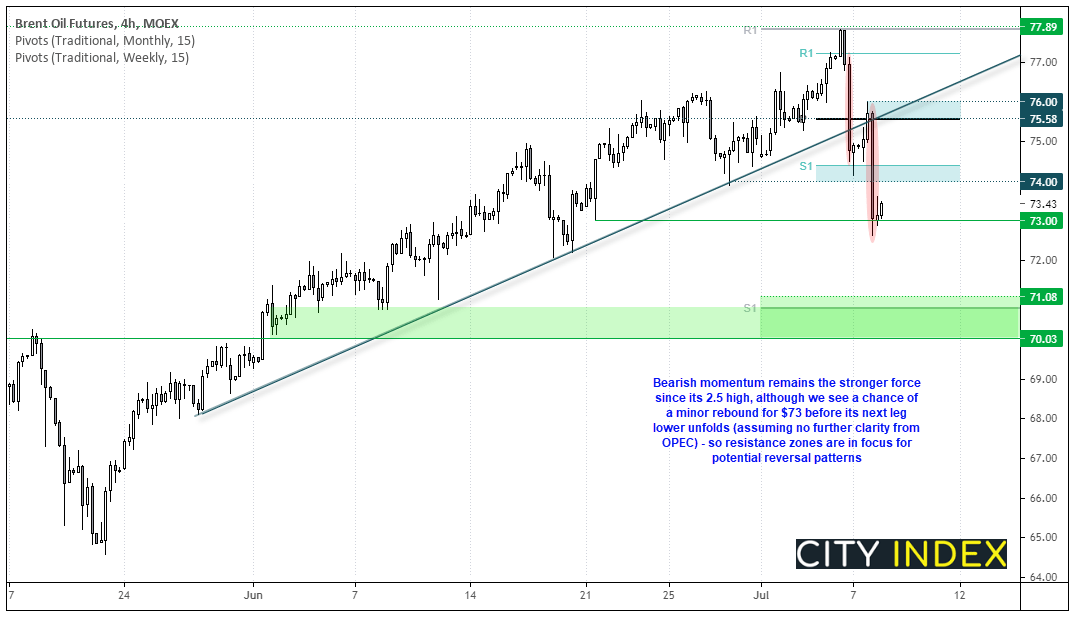

Commodities: Oil falls over -6% from its highs

The lack of OPEC clarity continued to weigh on oil prices for second day. WTI hit our near-term bearish target of 72.0 and Brent futures fell a further -2.2% to take its two-day fall to -6.6% from its 2.5 year high.

An early rebound saw resistance found around its weekly pivot and broken trendline, before accelerating to the downside and dipping below 73.00, to settle at 73.14. Given momentum remain favourable to bears, we are on the lookout for bearish reversal patterns around resistance zones. Should volatility remain low for a move towards 74-74.40 then perhaps bears can regain control.

Gold rose 0.4% despite a slightly strong US dollar, taking its lead from lower bond yields instead. It formed a bullish inside day which closed above 1800 yet beneath its 200-day eMA. Silver was effectively flat and formed a indecisive Doji, showing the market currently lacks direction.

Copper futures also printed a bullish inside day, failing to break beneath $4.20 support to confirm the next leg lower after printing a bearish hammer on Tuesday. We continue to watch that key level for a potential break, whilst a break above 4.4350 suggests bulls are regaining control.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM