Asian Futures:

- Australia's ASX 200 futures are down 0 points (0%), the cash market is currently estimated to open at 7,248.20

- Japan's Nikkei 225 futures are down 0 points (0%), the cash market is currently estimated to open at 30,500.05

- Hong Kong's Hang Seng futures are down -393 points (-1.63%), the cash market is currently estimated to open at 23,706.14

UK and Europe:

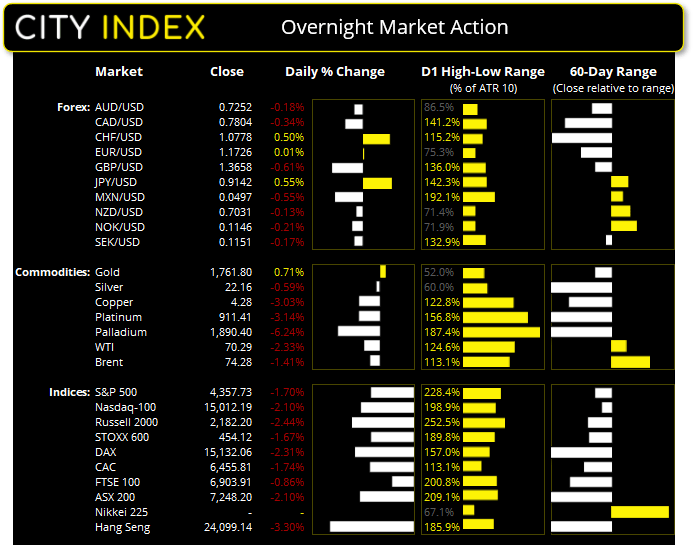

- UK's FTSE 100 index fell -59.73 points (-0.86%) to close at 6,903.91

- Europe's Euro STOXX 50 index fell -87.21 points (-2.11%) to close at 4,043.63

- Germany's DAX index fell -358.11 points (-2.31%) to close at 15,132.06

- France's CAC 40 index fell -114.38 points (-1.74%) to close at 6,455.81

Monday US Close:

- The Dow Jones Industrial fell -614.41 points (-1.78%) to close at 33,970.47

- The S&P 500 index fell -75.26 points (-1.7%) to close at 4,357.73

- The Nasdaq 100 index fell -321.286 points (-2.1%) to close at 15,012.19

Learn how to trade indices

Indices:

The FTSE 100 fell towards our target near the June lows, although later recovered to close back above the 200-day eMA. It was the most bearish session on the S&P 500 futures contract in four-months on rising volume, which saw the index fall to a 2-month low, taking its retracement from its all-time high to -5.6% by the day’s low.

The risk-off tone is stealing the thunder from what is to be a busy week of central bank meetings and economic data. It’s also possible that we may not see the Fed announce tapering on Wednesday’s meeting, which could leave the dollar vulnerable, although it currently remains bid in the current risk-off environment.

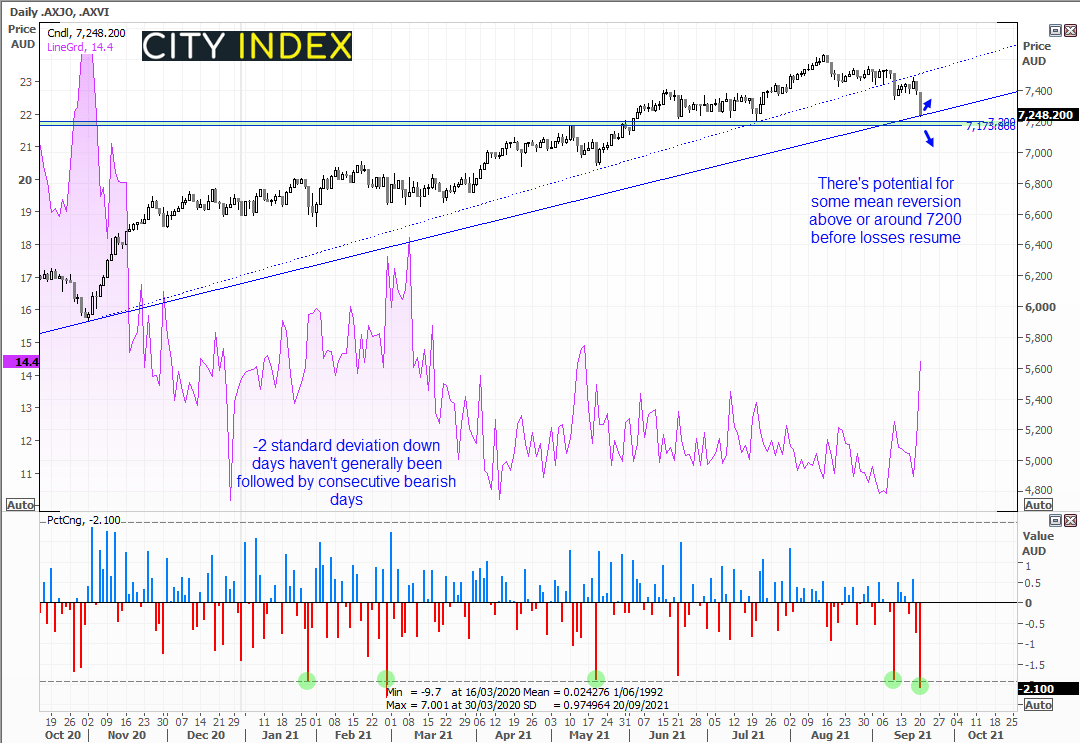

The ASX 200 was dragged lower by plummeting iron ore prices and the broader risk-off vibe from the Evergrande debacle. Falling over -2% during its worst session since late February, prices have found support at a longer-term trendline after posting a -2 standard deviation day. Whilst traders should continue to keep an eye on iron ore prices and the ongoing fallout surrounding Evergrande, it’s worth noting that down days that have fallen -2 standard deviations are not generally followed by continued selling. Coupled with the long-term trend support line and support around 7200 then (dare we say) the ASX 200 may have to undergo some mean reversion before losses continue.

Please note, exchanges in China and South Korea remain closed today due to public holidays.

ASX 200 Market Internals:

ASX 200: 7248.2 (-2.10%), 20 September 2021

- Utilities (1.01%) was the strongest sector and Materials (-3.74%) was the weakest

- 9 out of the 11 sectors closed lower

- 12 (6.00%) stocks advanced, 184 (92.00%) stocks declined

- 65% of stocks closed above their 200-day average

- 49% of stocks closed above their 50-day average

- 25.5% of stocks closed above their 20-day average

Outperformers:

- + 19.19% - AusNet Services Ltd (AST.AX)

- + 2.17% - Endeavour Group Ltd (EDV.AX)

- + 2.05% - Nufarm Ltd (NUF.AX)

Underperformers:

- -12.33% - Champion Iron Ltd (CIA.AX)

- -11.8% - Lynas Rare Earths Ltd (LYC.AX)

- -9.61% - Pilbara Minerals Ltd (PLS.AX)

Forex: JPY and CHF suck in safe-haven flows

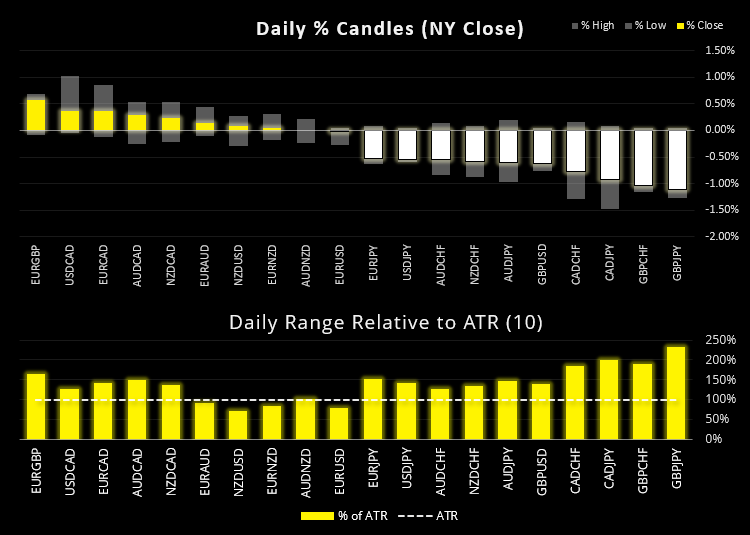

The Japanese yen and Swiss franc were the strongest currencies as they sucked up safe haven flows amidst a weak session on Wall Street. USD/JPY printed a bearish engulfing candle and once again failed to hold above 110. GBP/JPY was the weakest currency pair and hit our bearish target rather promptly, and GBP/USD is about ¾ of the way to reaching our target around the August low. We now wait to see how these markets react around their respective swing lows and whether Beijing will step in to bail out Evergrande and restore appetite for risk as a result.

The dollar also received safe haven bids against its peers excluding JPY and CHF. The US dollar index (DXY) reached our March-high target, although closed the day with a bearish pinbar which warns of near-term trend exhaustion. USD/CAD rallied to a 1-month high, fuelled by a stronger greenback and the growing potential that Canada’s PM Justin Trudeau could be unseated (or at the very least give away a lot of power to opposition parties) at the election. Canadian are currently at the polls casting their votes.

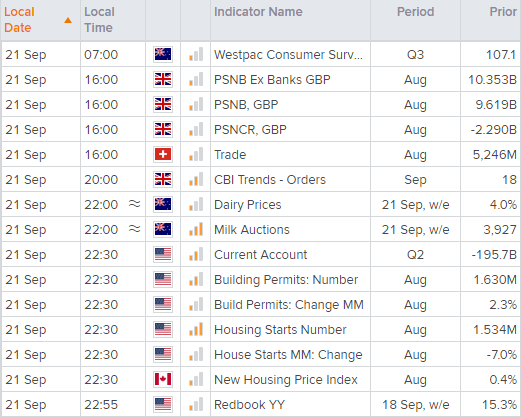

It’s very quiet today in Asia on the data front. A consumer sentiment report for New Zealand shows confidence has dipped to a 4-month low, although the drop is much less severe at just 4.4 points compared to the prior wave of the pandemic.

The first central bank meeting of the week is at 17:30 AEST, where Sweden’s Riksbank is expected to keep policy unchanged yet they may begin hinting at policy tightening due to a good recovery from the pandemic.

Learn how to trade forex

Commodities broadly lower

The Thomson Reuters CRB commodity index fell for a third day after printing a 6-year high last week. The stronger dollar and risk-off appetite has weighed on commodity prices in general, most notably across some metals which saw palladium fall a further -6.2%, and platinum and copper fall just over -3%. Silver was also down -0.6% which left gold as the only major metal market which closed higher on the day.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 07:49 AM

Today 04:24 AM

Yesterday 10:48 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM