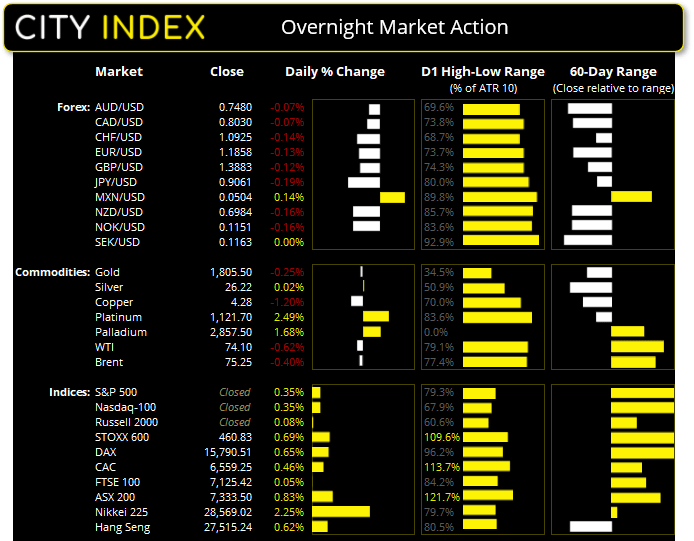

Asian Futures:

- Australia's ASX 200 futures are up 11 points (0.15%), the cash market is currently estimated to open at 7,344.50

- Japan's Nikkei 225 futures are up 180 points (0.63%), the cash market is currently estimated to open at 28,749.02

- Hong Kong's Hang Seng futures are up 71 points (0.26%), the cash market is currently estimated to open at 27,586.24

UK and Europe:

- UK's FTSE 100 index rose 3.54 points (0.05%) to close at 7,125.42

- Europe's Euro STOXX 50 index rose 25.29 points (0.62%) to close at 4,093.38

- Germany's DAX index rose 102.58 points (0.65%) to close at 15,790.51

- France's CAC 40 index rose 29.83 points (0.46%) to close at 6,559.25

Monday US Close:

- The Dow Jones Industrial rose 126.02 points (0.36%) to close at 34,996.18

- The S&P 500 index rose 15.08 points (0.35%) to close at 4,384.63

- The Nasdaq 100 index rose 51.798 points (0.35%) to close at 14,877.89

Learn how to trade indices

Indices higher ahead of earnings:

Wall Street advanced to new highs overnight ahead of earnings season, which is due to kick off this week. According to FactSet, Q2 earnings growth is estimated to rise 64% for the S&P 500 which would make it the highest YoY growth rate since Q4 2009. Moreover, 66 companies have issued a positive EPS guidance which would make it the highest on record since FactSet began tracking it in 2006.

The S&P 500 and Dow Jones broke to record highs and the Nasdaq 100 printed an intraday record high before closing with a small-legged Rikshaw Man Doji near its high. The FAANG index was a top performer, rising 0.91% with banks also outperforming with a 0.71% rally. The STOXX and STOXX 50 (also in yesterday’s video) also broke to new highs.

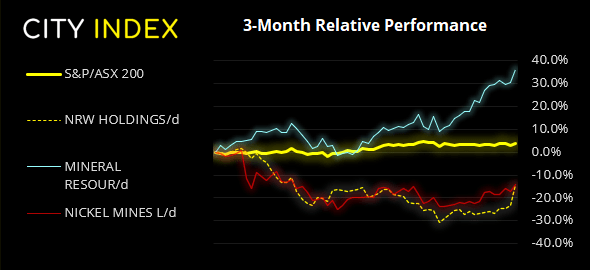

ASX 200 Market Internals:

ASX 200: 7333.5 (0.83%), 12 July 2021

- Materials (2.19%) was the strongest sector and Consumer Staples (-0.38%) was the weakest

- 9 out of the 11 sectors closed higher

- 2 out of the 11 sectors outperformed the index

- 131 (65.50%) stocks advanced, 62 (31.00%) stocks declined

- 6 hit a new 52-week high, 0 hit a new 52-week low

- 59.5% of stocks closed above their 50-day average

Outperformers:

- + 11.9% - NRW Holdings Ltd (NWH.AX)

- + 4.21% - Mineral Resources Ltd (MIN.AX)

- + 3.79% - Nickel Mines Ltd (NIC.AX)

Underperformers:

- -2.85% - Redbubble Ltd (RBL.AX)

- -2.16% - Star Entertainment Group Ltd (SGR.AX)

- -1.68% - Omni Bridgeway Ltd (OBL.AX)

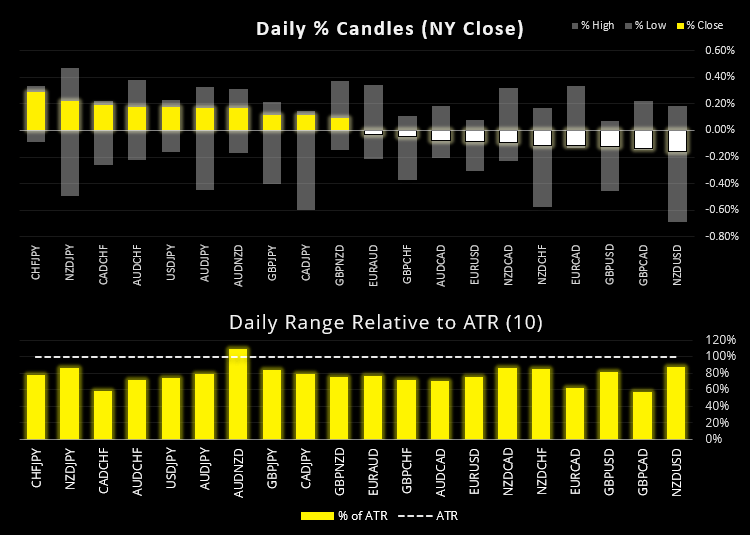

Forex: Neither volatile nor particularly directional

Lack of economic news resulted in lows of inside days and false breaks across currency pairs, with daily ranges typically below their averages ranges and producing more wicks than body. That traders are waiting for inflation data for the US means we could be in for more of the same, unless we see come surprises in today’s data for Asia.

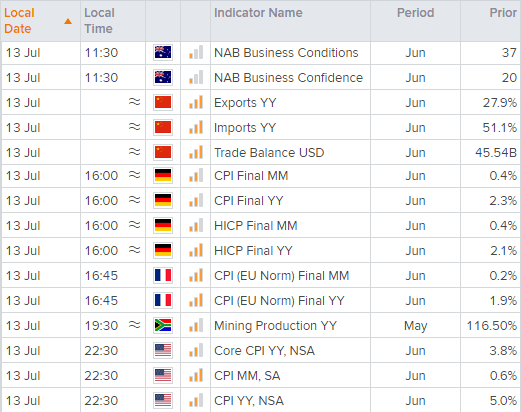

NAB (National Australia Bank) release their business conditions and confidence reports at 11:30 AEST. Sales, profits and employment rose sharply in the May read to take the headline conditions index to a record high in May and whilst business confidence dipped -3 points it remains historically high. China’s trade data will also be a focal point for AUD traders, as strong export data tends to be supportive of the currency (and risk-sentiment in general).

AUD/CHF respected the lower region of our 0.6868 – 0.6900 resistance zone overnight and formed a Doji below its 200-day eMA. AUD/USD was slightly lower overnight and closed around midway between the September 2020 high (0.7413) and its 200-day eMA (0.7050), with the latter making a viable bullish target should China’s exports and NAB business confidence rise.

Learn how to trade forex

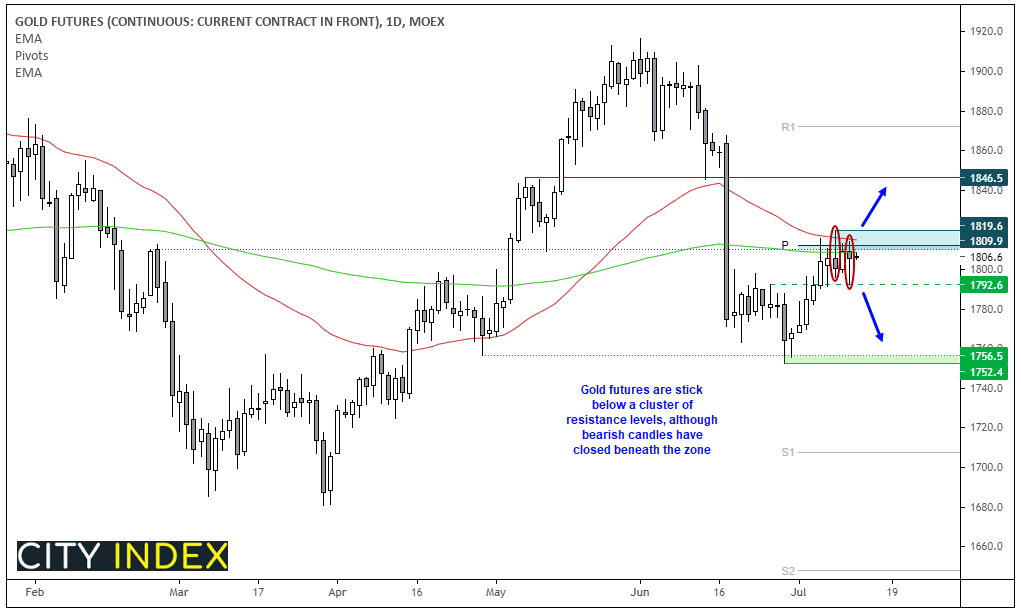

Commodities: Gold to break out of its range?

Oil prices were slightly lower as concerns over the spread of the latest COVID-19 variants offset tight crude supplies. WTI futures fell -0.62% to form a potential bearish hammer yet held above Friday’s low of 72.72 whilst Brent futures fell -0.4%.

Gold futures have effectively been trapped within a $30 range over the past week. Yet whilst prices rose into the recent consolidation, its prior leg lower from the June high was seen with strong bearish momentum, so we suspect gold prices may try to take another dip lower.

Note that a strong zone of resistance has capped any upside, and (levels include the monthly pivot point, 200 and 50-day eMA and prior support/resistance) and that bearish hammers have formed beneath it, suggesting a swing high is trying to form. A break below 1792 would confirm the bearish reversal candles and could clear the way for another leg lower, whilst a break above 1819.60 would clear the resistance zone and bring 1840 – 1846.5 into focus.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Indices articles

Yesterday 03:30 PM

April 18, 2024 04:46 PM