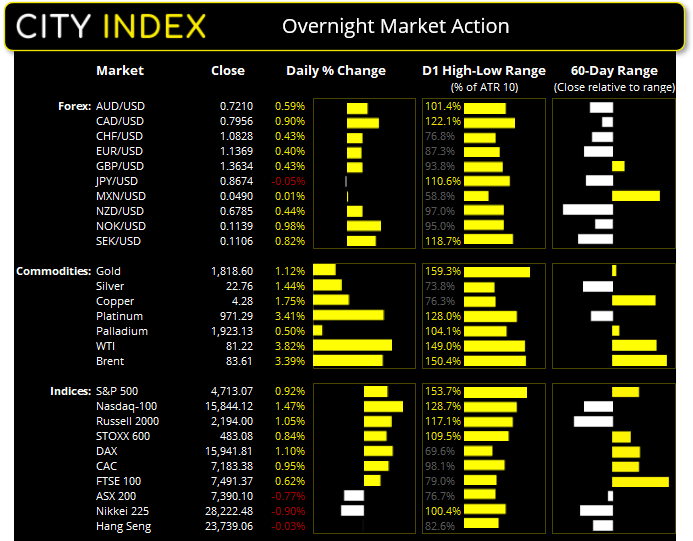

Jerome Powell telling the congressional hearing that the US economy is be able to withstand the combination of Omicron and the Fed tightening was music to Wall Street’s ears. Yields fell for a second day which alleviated pressure on tech stocks, allowing the Nasdaq to rally 1.5%. But overall, the colour of Wall Street was green for equity traders with the S&P and Russell 200 rising around 1% and the Dow up around 0.5%.

It could also be argued that yields remain overbought over the near-term, following their aggressive rally of late. And with markets getting too used to the idea of inflation being rampant, perhaps expectations (for much higher inflation) are ahead of themselves. Even a slight CPI miss today could be enough to shake out some pre-emptive doom-mongerers and further support equities, as part of the reason they sold off was the upward revision to Fed hikes, based upon inflationary fears.

ASX 200 to take Wall Street’s lead?

The ASX 200 fell -0.77% and closed below 7400 yesterday, but that fact that prices remain elevated above Thursday’s -2.8% bearish day (and trend support from the December low) is slightly encouraging for the bull-camp.

Dollar softer as it loses safe-haven appeal

The revival of appetite for risk has seen the dollar lose some of its safe-haven sparkle. The US dollar index trades near the lows of its 9-week range, and a clear break beneath 95.50 morphs this into topping pattern and likely confirms a bullish breakout on EUR/USD. The Australian dollar rose to a 1-month high although we still suspect this is simply part of a 3-wave countertrend move, so waiting for bearish momentum to return around 0.7220. The slight risk-on tone is also apparent on AUD/JPY which recouped most of yesterday’s losses, alongside the fact that the yen was the weakest currency yesterday.

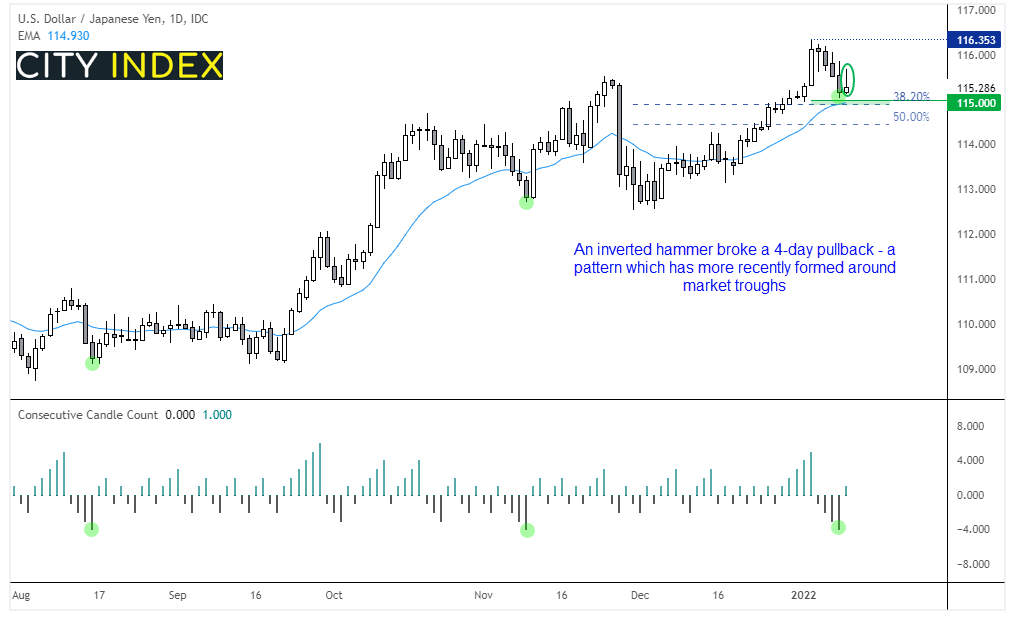

USD/JPY continues to hold above 115

However, USD/JPY dances to its own beat. Its rally from the December low saw USD/JPY gain around 3.4% in a relatively straight line. Since then, we have seen a retracement consist of 4-consecutive bearish days which was broken yesterday with a slightly bullish, inverted hammer. Given the past two days have held above 115 it appears to be an important level heading into today’s inflation report, where a decent print could see momentum realign with its bullish trend.

Another $20 day for gold

Price action on gold has piqued our interest the past two days because both bullish sessions have effectively opened at the low of the session and closed at the high. With banks upping their forecasts for potential Fed hikes and real yields falling, gold has regained its shine and seemingly behaving as an inflationary hedge again, ahead of today’s CPI data.

WTI back above $80

Powell also convinced energy traders that all is okay, despite the surge of Omicron. Rallying over 3.8%, it was WTI’s best day in 5-weeks, so our bias remains bullish above the 77.90 low and brings $85 back into focus.

Up Next (Times in AEDT)

How to trade with City Index

You can easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Trade Ideas articles

Yesterday 03:00 PM

Yesterday 11:14 AM

April 24, 2024 11:00 AM