Asian Futures:

- Australia's ASX 200 futures are up 1 points (0.01%), the cash market is currently estimated to open at 7,303.50

- Japan's Nikkei 225 futures are down -10 points (-0.03%), the cash market is currently estimated to open at 28,948.56

- Hong Kong's Hang Seng futures are up 133 points (0.46%), the cash market is currently estimated to open at 28,871.88

UK and Europe:

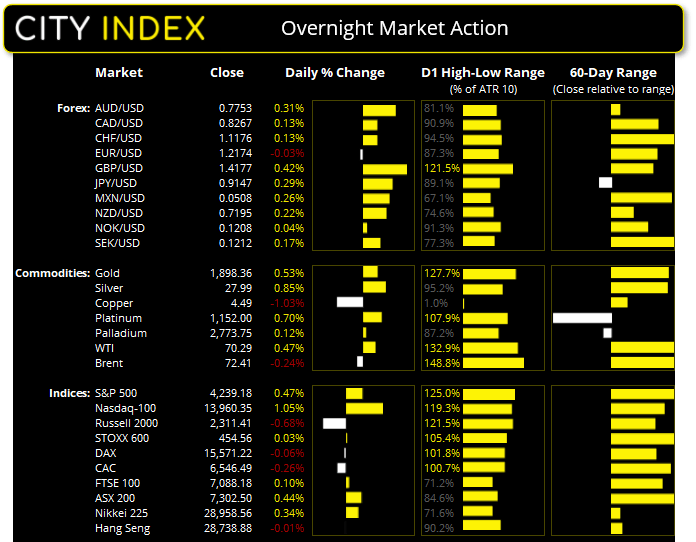

- UK's FTSE 100 index rose 7.17 points (0.1%) to close at 7,088.18

- Europe's Euro STOXX 50 index fell -0.78 points (-0.02%) to close at 4,096.07

- Germany's DAX index fell -9.92 points (-0.06%) to close at 15,571.22

- France's CAC 40 index fell -16.96 points (-0.26%) to close at 6,546.49

Thursday US Close:

- The Dow Jones Industrial rose 19.1 points (0.06%) to close at 34,466.24

- The S&P 500 index rose 19.63 points (0.47%) to close at 4,239.18

- The Nasdaq 100 index rose 145.404 points (1.05%) to close at 13,960.35

Learn how to trade indices

US indices take comfort in US inflation report:

CPI YoY rise to 5% (its most inflationary level since 2008). However, some of its rise can be attributed to the ‘basing effect’ and low figures last year, which are expected to level off in next month’s report. On the month CPI rose 0.6%, down from 0.8% prior. Basically, inflation is rising but not above and beyond expectations and, whilst the jury remains out as to whether it is transitory or not, the Fed is not seemingly under too much pressure to pop the stock market fun and begin ‘talking about talking’ about tapering.

The Nasdaq 100 closed to a six-week high and moved in on its record high, stopping just 31 points shy of 14k. The S&P 500 was lifted to its record high by healthcare, real estate and technology stocks.

Technology and banking stocks lifted the ASX 200 yesterday, narrowly avoiding a break beneath its key reversal high. Futures markets are pointing to an open around 7300 which may prove to be a pivotal level. The key here is seeing if it acts as support or resistance, before assuming a direction simply by where prices trade from it after the open.

ASX 200 Intraday S/R Levels

- R2: 7334.90

- R1: 7311 – 7314.60

- Pivotal: 7302.50

- S1: 7289

- S2: 7267.60 – 7265.60

- S3: 7244.30 – 7251.00

ASX 200 Market Internals:

ASX 200: 7302.5 (0.44%), 10 June 2021

- Real Estate (2.34%) was the strongest sector and Materials (-0.01%) was the weakest

- 10 out of the 11 sectors closed higher

- 5 out of the 11 sectors outperformed the index

- 123 (61.50%) stocks advanced, 68 (34.00%) stocks declined

- 12 hit a new 52-week high, 0 hit a new 52-week low

- 73.5% of stocks closed above their 200-day average

- 72% of stocks closed above their 50-day average

- 78.5% of stocks closed above their 20-day average

Outperformers:

- + 16.8% - Iress Ltd (IRE.AX)

- + 5.18% - Whitehaven Coal Ltd (WHC.AX)

- + 3.85% - Unibail-Rodamco-Westfield SE (URW.AX)

Underperformers:

- -3.40% - NRW Holdings Ltd (NWH.AX)

- -3.33% - A2 Milk Company Ltd (A2M.AX)

- -3.27% - Worley Ltd (WOR.AX)

Forex: GBP Strongest major, USD volatility lacked direction

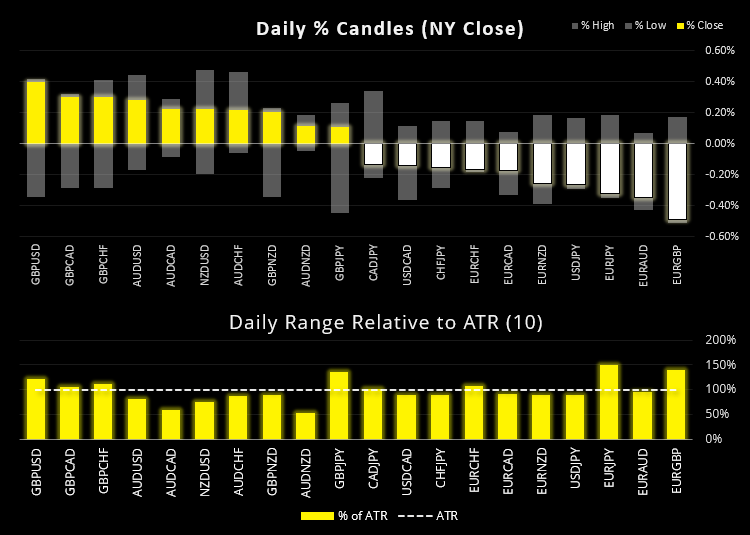

Volatility certainly returned to currency markets overnight, although not all currencies provide directional moves. The US dollar index (DXY) saw spikes either side of its open and eventually closed around -0.05% lower, to produce an indecision candle (Doji) just beneath its 20-day eMA.

In EUR/USD terms, an equally frustrating candle was produced with a 0.04% gain just above its 20-day eMA. EUR/JPY produced a bearish outside candle after a false break above trendline resistance on the daily chart. Despite holding above the 1.3289 low, we have temporarily removed it from the long watchlist.

After a false break above Wednesday’s high, USD/JPY quickly erased and headed back towards 109.16 support to close the session with a bearish engulfing day, thus removing it from our bullish watchlist. Given this followed on from a larger bearish engulfing candle last week (around twice the size) then it appears a break beneath 109.16 could eventually be on the cards.

USD/CHF produced a bearish hammer, and its high of the day perfectly respected its 20-day eMA. Like USD/JPY, it now appears set to test and break recent lows at 0.8926.

The British pound was the strongest major overnight (and the second strongest over the past month). Sterling became the currency of the session thanks to the ECB keeping their stimulus taps fully open and on the back of higher-than-expected inflation form the US (and a weaker dollar).

Learn how to trade forex

Commodities: Gold bugs set to return?

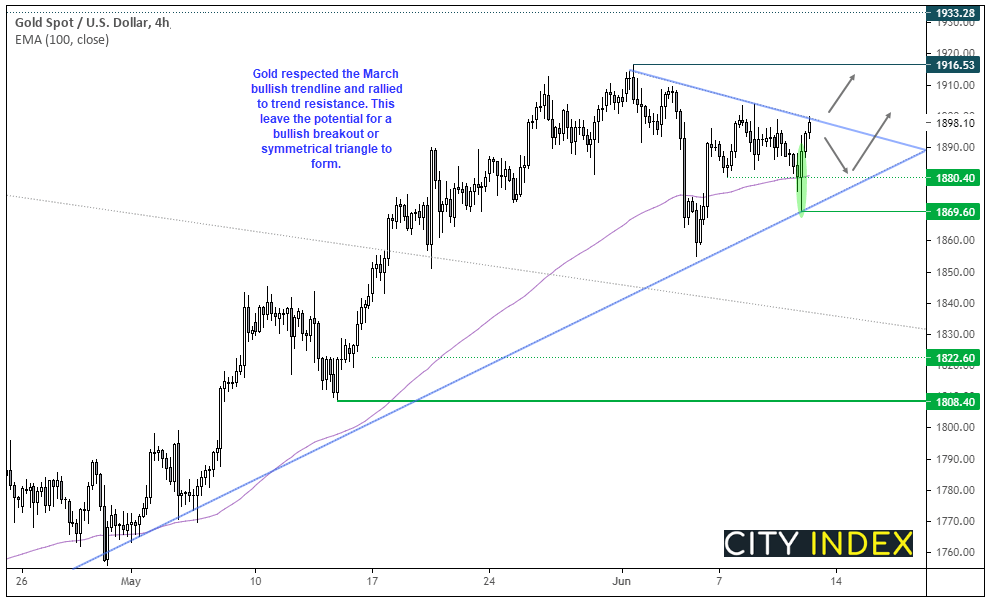

Lower real interest rates and a weaker USD only added to the argument for gold bugs to return. A bullish engulfing candle with a large lower wick (buying tail) appeared on the daily chart overnight. After selling off ahead of the CPI report, support was found at the bullish trendline form the March low before a V-shape recovery formed and prices were propelled higher. Whilst prices remain below 1900, gold’s bullish structure suggest it may mow try to break above trend resistance and head towards 1916.53 (and possibly beyond). Whilst our bias remains bullish above 1869.60, support around 1880.40 from the 100-hr eMA and closing price lows can also be used to aid with risk management. Should prices not break above trendline resistance soon, then an alternative (and potentially still bullish) scenario is for a symmetrical triangle to form.

The inflationary tailwind didn’t make its way over to silver, which remains stuck below 28.0 despite printing a bullish outside candle. Out of the two metals gold appears the more structurally sound for the bullish case.

Oil prices essentially tracked the US dollar (invertedly) and produced another Indecision candle around its cycle highs. With inflation out of the way we may find oil’s fundamentals come back into play (which remain bullish overall) but we’d like to see a solid level of support build on WTI above 67.98 before its trend resumes. Break below said support likely signals a correction.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM