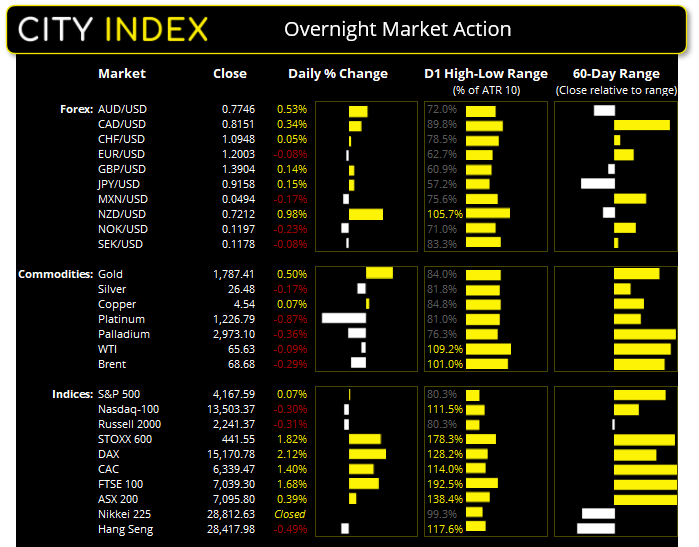

Asian Futures:

- Australia's ASX 200 futures are up 5 points (0.07%), the cash market is currently estimated to open at 7,100.80

- Japan's Nikkei 225 futures are down -20 points (-0.07%), the cash market is currently estimated to open at 28,792.63

- Hong Kong's Hang Seng futures are up 78 points (0.28%), the cash market is currently estimated to open at 28,495.98

UK and Europe:

- UK's FTSE 100 index rose 116.13 points (1.68%) to close at 7,039.30

- Europe's Euro STOXX 50 index rose 77.99 points (1.99%) to close at 4,002.79

- Germany's DAX index rose 314.3 points (2.12%) to close at 15,170.78

- France's CAC 40 index rose 87.72 points (1.4%) to close at 6,339.47

Wednesday US Close:

- The Dow Jones Industrial rose 97.31 points (0.29%) to close at 344,230.34

- The S&P 500 index rose 2.93 points (0.08%) to close at 4,167.59

- The Nasdaq 100 index fell -41.297 points (-0.3%) to close at 13,503.37

Indices: New High for the Dow, Strong Recovery in Europe

Supporting a COVID-19 IP waiver (intellectual property rights) is something Biden said he would support during his presidential campaign. But, after rising cases in India and mounting pressure from over 100 countries, the US issued a statement to confirm that certain IP’s would be temporarily waivered to help countries fight the pandemic. With investors already pricing in a reopening for much of the Western world, this move could make the recovery more ‘wholesome’ for the global community.

The Dow Jones industrial closed to a record high and commodity currencies (NZD, AUD and CAD) were the strongest majors overnight. Still, tech stocks remained under pressure with Microsoft (MFST) and Amazon (AMZN) dragging the Nasdaq 100 down, which gave back earlier gains to close 0.3% lower.

Earlier in the session, ISM services missed expectations at 62.7 vs 63.7 expected, business activity fell to 62.7 from 69.4 and new orders down to 63.2 from 67.2. Still, theses aren’t exactly terrible numbers, and simply a case of losing a little momentum from giddy heights.

It was a better session for Europe, rallying to their strongest close in two months and all but eradicating Tuesday’s sell-off. Basic resources and oil and gas sectors pushed the STOXX 600 to a +1.8% gain whilst the DAX effectively invalidated its head and shoulders breakout within 24 hours of its apparent confirmation. Now back above 15,000, a break above trendline resistance could signal the resumption of its bullish trend.

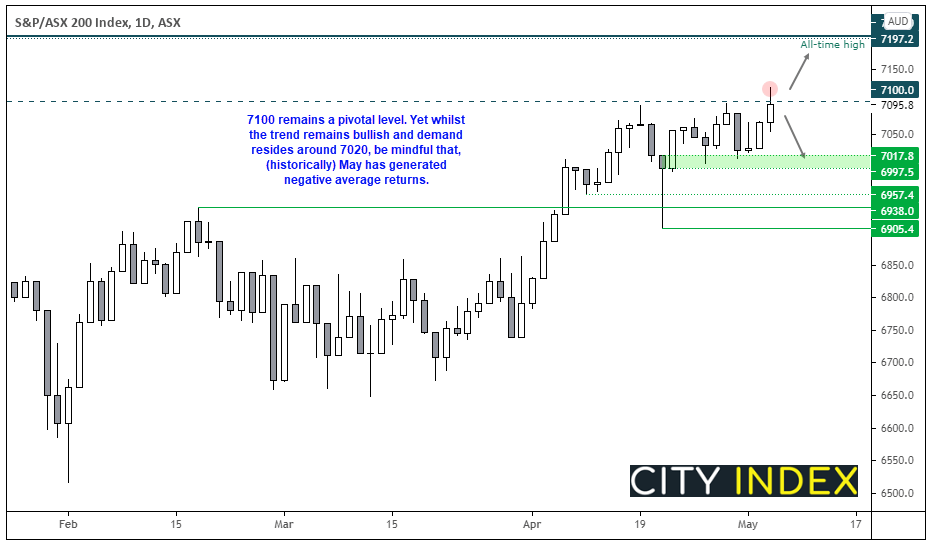

ASX 200: Is Today the Day?

We should be in for a firmer open in Asia thanks to the boost in sentiment, so this should see the ASX 200 above 7100. So, the question now is whether it can remain above it for more than two minutes. On one hand, the trend is bullish overall and there is clearly demand around 7020. But on the other, May is generally one of the worst months for ASX returns so perhaps any upside moves could be short lived. A daily close above 7100 would at least be a positive start whilst repeated (failed attempt) to close above it suggests it to be topping out.

ASX 200: 7095.8 (0.39%), 04 May 2021

- Healthcare (0.97%) was the strongest sector and Information Technology (-1.11%) was the weakest

- 2 out of the 11 sectors outperformed the index

- 9 out of the 11 sectors closed higher

- 10 hit a new 52-week high, 2 hit a new 52-week low

- 73% of stocks closed above their 200-day average

- 49% of stocks closed above their 20-day average

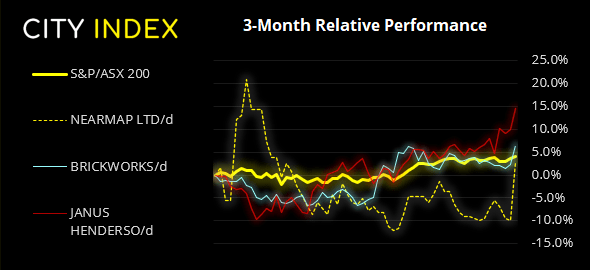

Outperformers

- + 14.6% - Nearmap Ltd (NEA.AX)

- + 4.23% - Brickworks Ltd (BKW.AX)

- + 4.11% - Janus Henderson Group PLC (JHG.AX)

Underperformers:

- -5.39% - Flight Centre Travel Group Ltd (FLT.AX)

- -5.05% - Polynovo Ltd (PNV.AX)

- -4.39% - Ramsay Health Care Ltd (RHC.AX)

Learn how to trade indices

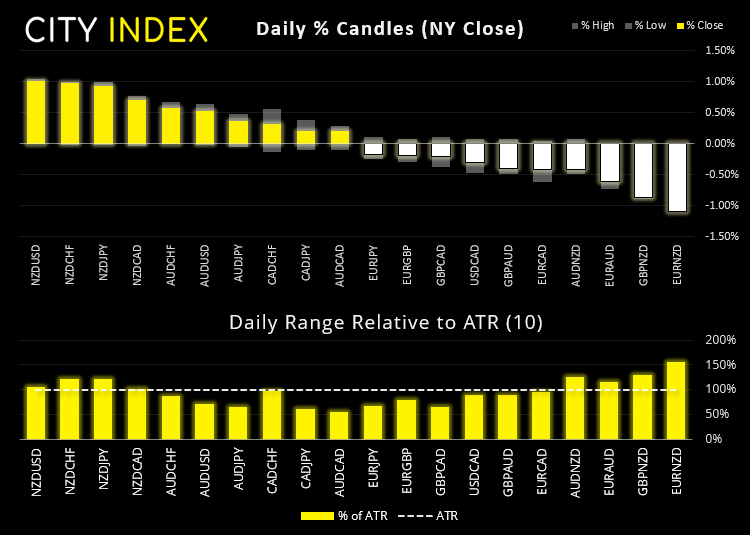

Forex: A few interesting setups are NZD pairs

The US dollar index (DXY) was essentially flat overnight, closing the day with a Doji (indecision candle) after teasing with a break above 91.40 resistance before closing just beneath it.

- We’re keeping an eye on NZD/JPY for a potential breakout (or breakdown). The daily chart continues to respect trend support projected form the March low, however, it is heading for strong resistance at the February high at 79.20.

- Conversely, AUD/NZD is also trading above trendline support, yet momentum has turned. Therefore, this trendline could well come under attack quite soon, given it printed a bearish hammer which failed to close above 1.8000 and subsequent bearish engulfing candle.

- EUR/NZD has closed beneath 1.6665 support with a bearish engulfing candle, just one day after a bearish hammer failed to hold above 1.6824 resistance.

- CAD/JPY broke above its small corrective channel on the four-hour chart and is treading water just beneath 89.22 resistance. A break above this level confirms trend resumption and the bias remains bullish above the 88.40 low.

Learn how to trade forex

Commodities: Copper Falters at Its High

As we feared following Tuesday’s minor break to a 10-year high, momentum was not sustained, and copper futures are now back below 4.55. The trend remains bullish above 4.49 on the four-hour chart, yet near-term momentum favours a retest (and potential) break of this ley level.

Oil prices looked past a large drop in crude stocks and positive covid vaccine news to close the session effectively flat. Brent found resistance at $70 and WTI failed to hold onto a small breakout above 66.40 resistance, although perhaps not surprising given the significance brent’s $70.

Falling real rates helped gold rise 0.50% and reaffirm support at 1769.60. Our bias remains bullish above 1760 and for an eventual break above 1800.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 05:45 AM

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Latest ASX articles

April 18, 2024 02:40 AM

April 16, 2024 10:19 PM

April 10, 2024 11:24 PM

April 9, 2024 11:02 PM