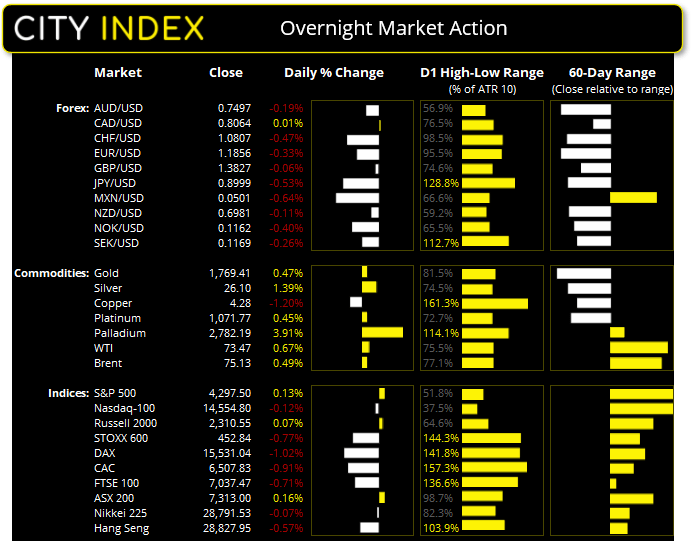

Asian Futures:

- Australia's ASX 200 futures flat (0%), the cash market is currently estimated to open at 7,265.60

- Japan's Nikkei 225 futures are up 120 points (0.42%), the cash market is currently estimated to open at 28,827.04

- Hong Kong's Hang Seng futures are up 18 points (0.06%), the cash market is currently estimated to open at 28,845.95

UK and Europe:

- UK's FTSE 100 index rose 87.69 points (1.25%) to close at 7,125.16

- Europe's Euro STOXX 50 index rose 14.59 points (0.36%) to close at 4,078.89

- Germany's DAX index rose 72.77 points (0.47%) to close at 15,603.81

- France's CAC 40 index rose 45.99 points (0.71%) to close at 6,553.82

Thursday US Close:

- The Dow Jones Industrial rose 131.02 points (0.38%) to close at 34,633.53

- The S&P 500 index rose 22.44 points (0.53%) to close at 4,319.94

- The Nasdaq 100 index rose 5.252 points (0.04%) to close at 14,560.05

Learn how to trade indices

Indices: S&P hits record high for 6th straight day

Another day, another set of strong employment data and record highs for the US stock market. Weekly jobless claims continued to fall and now sit at their lowest level since the pandemic began. And, in a separate report, intentions to lay-off staff by firms have hit a 21-year low. That said, the employment component of the ISM manufacturing index contracted to 49.9 from 50.9. But, taken alongside strong ADP beating expectations earlier this week (even if softer than the prior read), it’s not a bad set of data overall ahead of today’s NFP report. But, as Matt Weller points out, some leading indicators point towards a weaker-than expected NFP today which could lead to another disappointment for the highly anticipated release (and take the wind out of sentiment just before the weekend).

The S&P 500 hit a record high for a sixth consecutive session and rose 0.5%, led by energy, utility and financial sectors. Consumer staples was the only sector to close in the red. Nasdaq biotech stocks rose 1.16%, banking stocks were up 1.06% although the Nasdaq 100 was only up by 0.04%. FAANGS were down slightly at -0.05%.

ASX 200 Market Internals:

ASX 200: 7265.6 (-0.65%), 30 July 2021

- Materials (0.08%) was the strongest sector and Consumer Discretionary (-1.3%) was the weakest

- 9 out of the 11 sectors closed lower

- 59 (29.65%) stocks advanced, 134 (67.34%) stocks declined

- 9 hit a new 52-week high, 2 hit a new 52-week low

- 71.36% of stocks closed above their 200-day average

- 60.3% of stocks closed above their 50-day average

- 46.23% of stocks closed above their 20-day average

Outperformers:

- + 8.05% - Regis Resources Ltd (RRL.AX)

- + 5.57% - St Barbara Ltd (SBM.AX)

- + 5.43% - Nuix Ltd (NXL.AX)

Underperformers:

- -5.93% - Chalice Mining Ltd (CHN.AX)

- -4.92% - Iluka Resources Ltd (ILU.AX)

- -4.51% - Metcash Ltd (MTS.AX)

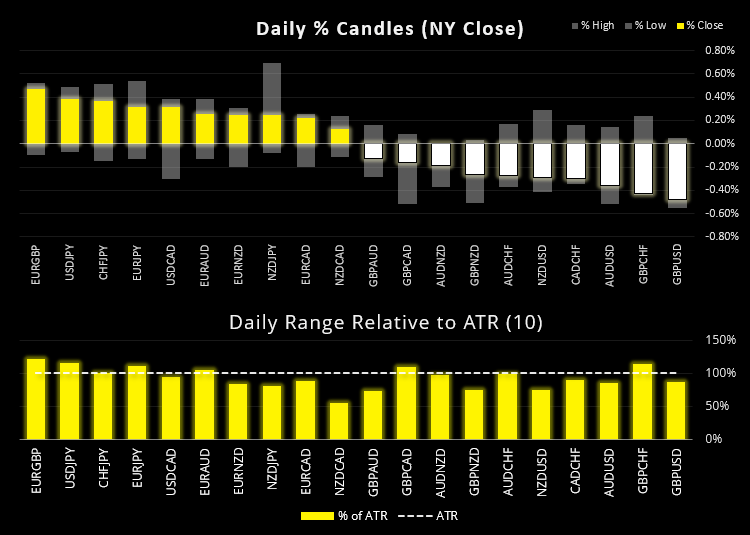

Forex: USD retains extends its lead, BOE Bailey send GBP lower

The US dollar index (DXY) rose to a three-month high of 92.630 overnight as economic data hinted towards a strong NFP print, in turn bring expectations of a hike sooner than the Fed are currently making out. Let’s hope NFP excels to live up to bullish expectation, or else gains be quickly lost.

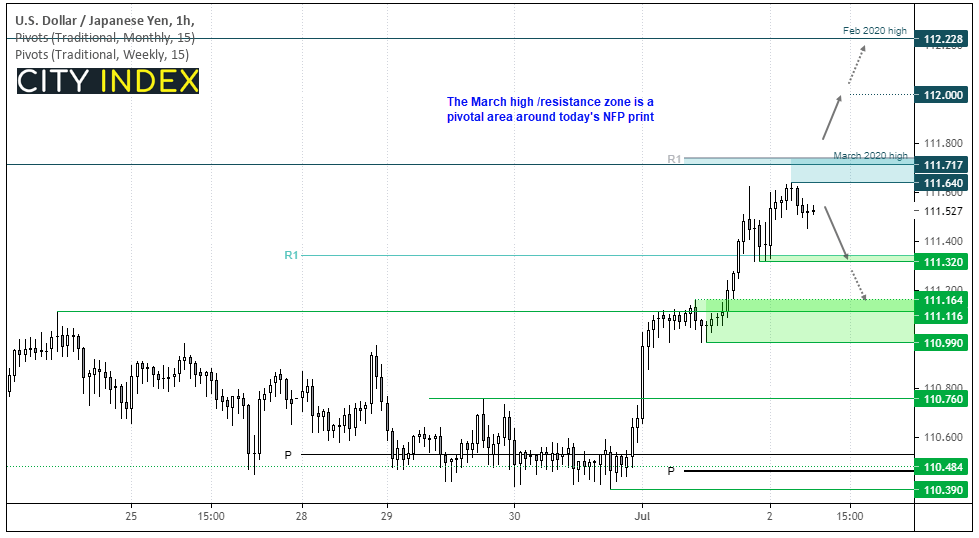

USD/JPY reached our first target in the European session and second target in the US and is now trading slightly lower around 111.50. Its next major resistance levels to conquer are the pandemic and highs at 111.71 and 112.22 (with 112.00 thrown in due to being a round number, of course). If today’s NFP data comes in strong enough it could reach 112.0 quite easily and possibly even 12.22. But, if it disappoints once again, we’d expect prices to close firmly beneath the March 2020 high of 111.70 this week and roll over. Therefore, the March 2020 high is a pivotal level around today’s FP report in our view.

The British pound was the weakest currency BOE’s governor Andrew Bailey after saying it was important to not overact (ie. raise rates) to rising inflation. GBP/USD broken beneath key support of 1.3784 to an 11-week low and EUR/GBP rose 0.43% to print a bearish outside candle. Incidentally, GBP/USD was the weakest pair and EUR/GBP was the strongest.

AUD/USD fell to its lowest level this year before finding support at the December 1st low It very much remains in the hands of today’s NFP report. AUD/CAD warrants a look as it has formed a bullish hammer at the June low (and just above its October low). Granted, its not the prettiest of trades but there is potential for a counter-trend bounce, particularly if Canada’s PMI data, building permits and trade balance data disappoints at 1:30pm tonight.

Learn how to trade forex

Commodities: OPEC+ send oil prices higher

Gold prices rallied for a second day and rose around 0.3%, which is not bad given the strength of the US dollar. We had tipped out hat to gold’s potential to rise yesterday although it didn’t quite reach our lower target of 1785. Still, with real-rates (represented by TIPS) continuing to fall, perhaps there’s till room for gold to rise from here.

The OPEC+ meeting sent oil prices higher after indicating they would increase production at a slower rate than expected. WTI rose 2.4% to 75.23 and brent rallied 0.53% to settle at 75.53.

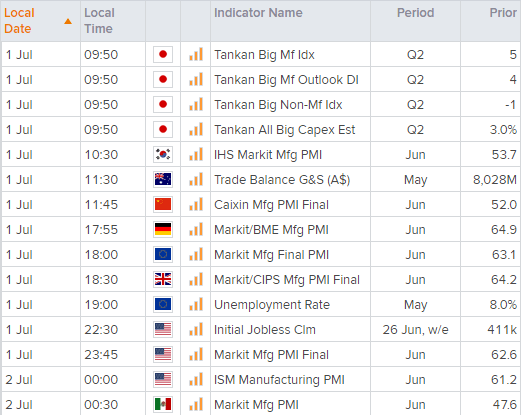

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Latest Indices articles

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM