Asian Futures:

- Australia's ASX 200 futures are up 38 points (0.53%), the cash market is currently estimated to open at 7,273.30

- Japan's Nikkei 225 futures are up 690 points (2.46%), the cash market is currently estimated to open at 28,700.93

- Hong Kong's Hang Seng futures are up 139 points (0.49%), the cash market is currently estimated to open at 28,628.00

UK and Europe:

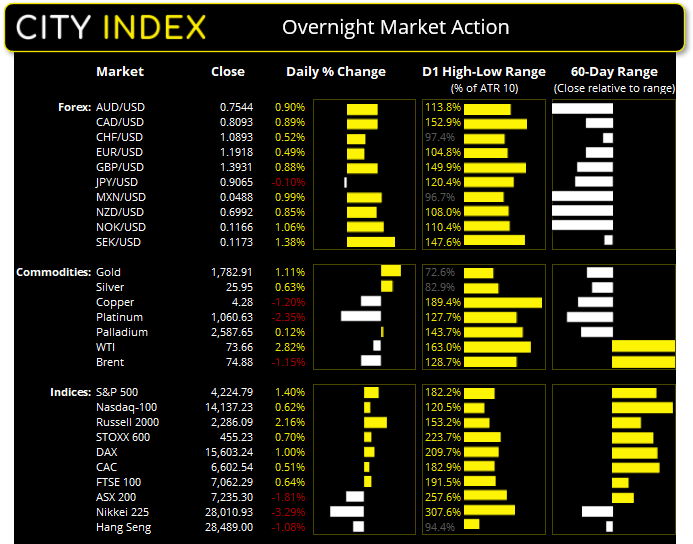

- UK's FTSE 100 index rose 44.82 points (0.64%) to close at 7,062.29

- Europe's Euro STOXX 50 index rose 28.96 points (0.71%) to close at 4,112.33

- Germany's DAX index rose 155.2 points (1%) to close at 15,603.24

- France's CAC 40 index rose 33.38 points (0.51%) to close at 6,602.54

Monday US Close:

- The Dow Jones Industrial rose 586.89 points (1.76%) to close at 33,876.97

- The S&P 500 index rose 58.34 points (1.41%) to close at 4,224.79

- The Nasdaq 100 index rose 87.645 points (0.62%) to close at 14,137.23

Learn how to trade indices

Indices:

The Dow Jones led Wall Street’s rebound overnight, rising 1.76% compared to the 1.4% rise on the S&P 500 and 0.6% on the Nasdaq 100. All sectors of the S&P 500 flashed green with energy and financial sectors gaining 4.2% and 2.3% respectively. Small caps also rebounded with the Russell 2000 recouping 2.1% and the R2K value index up 2.5% whilst S&P 600 small caps rose 2.6%. This all points to a brighter open for Asia today, with Nikkei, TOPIX and SPI 200 futures all signalling a firmer start.

The ASX 200 fell to a twelve-day low yesterday during its worst session in a Month. With most of its losses occurring in the first hour of trade an intraday triangle formed around its lows. Given RSI (2) was oversold at 7.2 is was already suggesting it was overbought over the near-term, and futures markets suggest the market will open around 7283 today.

ASX 200 Intraday S/R

- R4: 7406

- R3: 7381

- R2: 7361

- R1: 7319

- S1: 7265 - 7275

- S2: 7245

- S3: 7200 – 7207

- S4: 7119

ASX 200 Market Internals:

ASX 200: 7235.3 (-1.81%), 18 June 2021

- Consumer Staples (0.22%) was the strongest sector and Industrials (-1.9%) was the weakest

- 10 out of the 11 sectors closed lower

- 33 (16.50%) stocks advanced, 159 (79.50%) stocks declined

- 3 hit a new 52-week high, 2 hit a new 52-week low

- 72.5% of stocks closed above their 200-day average

- 59.5% of stocks closed above their 50-day average

- 51% of stocks closed above their 20-day average

Outperformers:

- + 2.46% - Afterpay Ltd (APT.AX)

- + 2.27% - Megaport Ltd (MP1.AX)

- + 2.08% - Altium Ltd (ALU.AX)

Underperformers:

- -11.8% - Codan Ltd (CDA.AX)

- -7.81% - Chalice Mining Ltd (CHN.AX)

- -7.00% - NRW Holdings Ltd (NWH.AX)

Forex: The dollar retreats on FOMC-fatigue

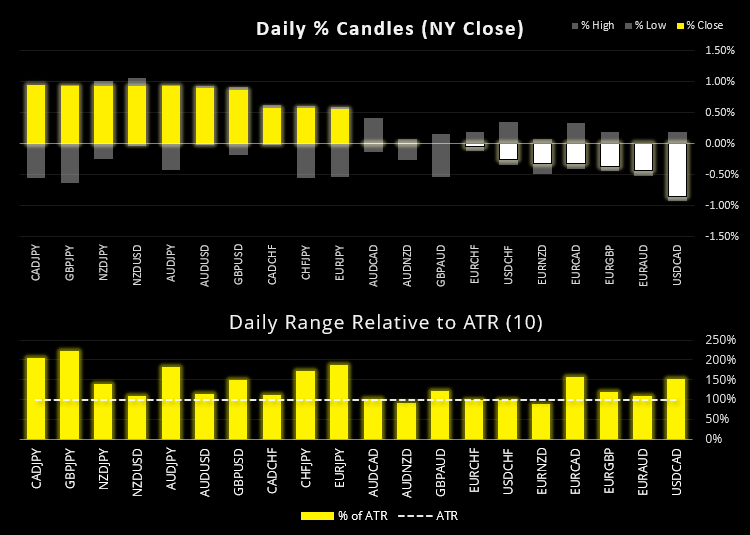

The US dollar index (DXY) pretty much explains what has occurred across most FX majors; a two bar-reversal which retraced most if not all of Friday’s moves. USD/CAD is back below 1.2400, NZD/USD is back above 0.6943 support. AUD/USD is back above the April low (although found resistance at tis 200-day eMA) which leaves a clear pivotal level today for traders. And GBP/USD printed a bullish engulfing candle yet closed just beneath Friday’s high. So, the key question over the next 24 hours is whether this is part of a deeper correction against last week’s FOMC rally, or simply a single-day event of the dollar’s demise. We will therefore keep a close eye how DXY plays around its 200-day eMA / Friday’s low which is currently acting as support, as a break beneath it suggests a deeper correction.

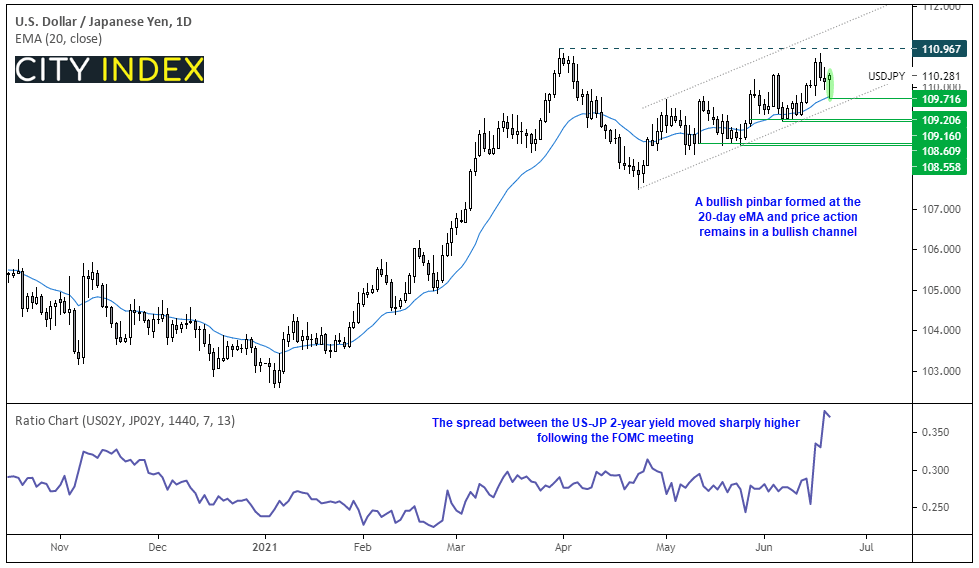

USD/JPY is dancing its own beat and shows the potential for another leg higher, given the policy divergence between the Fed and BOJ. A bullish pinbar has formed at its 20-day eMA to suggest a swing low is in place at 109.71 and prices remain elevated from trendline support to suggest momentum is picking up. Given the spread between US-JP 2-year bonds has risen sharply higher then we suspect USD/JPY is building up towards a move towards the 110.96 high.

Learn how to trade forex

Commodities: Metals rise

Gold held above 1760 and rose 1.07% as part of a (relatively mild) counter-trend move, which we discussed in yesterday’s video. A move to 1800 is not out of the question given the magnitude of last week’s 6% loss, where we may seek bearish setups if volatility remains low below or around that key level.

Silver is lagging behind gold but also shows the potential for a rebound from its lows. A small bullish engulfing candle formed and closed above the 25.70 low and it does remain above its 200-day eMA., so perhaps a return to its 100-day eMA around 26.53 / Friday’s high could be on the cards.

Platinum printed a small-bullish candle with a low of 1022 (just above our 1100 target following its trendline break), so we’re happy to step aside on this one.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM