Asian Futures:

- Australia's ASX 200 futures are down 0 points (0%), the cash market is currently estimated to open at 7,460.20

- Japan's Nikkei 225 futures are up 90 points (0.3%), the cash market is currently estimated to open at 30,413.34

- Hong Kong's Hang Seng futures are up 81 points (0.33%), the cash market is currently estimated to open at 24,748.85

UK and Europe:

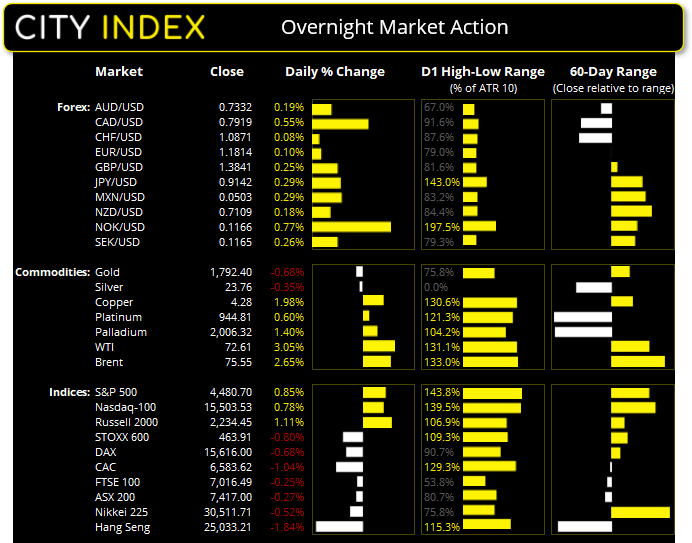

- UK's FTSE 100 index rose 10.99 points (0.16%) to close at 7,027.48

- Europe's Euro STOXX 50 index rose 23.93 points (0.58%) to close at 4,169.87

- Germany's DAX index rose 35.75 points (0.23%) to close at 15,651.75

- France's CAC 40 index rose 38.97 points (0.59%) to close at 6,622.59

Thursday US Close:

- The Dow Jones Industrial fell -36.07 points (-0.18%) to close at 34,751.32

- The S&P 500 index fell -6.95 points (-0.16%) to close at 4,473.75

- The Nasdaq 100 index rose 12.374 points (0.08%) to close at 15,515.91

Learn how to trade indices

Indices:

US retail sales surprised to the upside, rising 0.7% in August compared to the -0.8% contraction expected. Over the past year retail sales have risen 15.1%, with clothing/accessories, food and drink services and department stores contributing the most if we exclude gasoline (38.8%). Jobless claims rose slightly last week but, in context of it sitting just off post-pandemic lows, was negligible overall.

After a weak start on Wall Street, prices recovered as they headed towards the close with just the Nasdaq 100 posting a minor gain of 0.08%. The S&P 500 was down -0.16%, with energy and materials leading 7 of its sectors lower. The Dow Jones fell -0.18%.

The Nikkei 225 printed its most bearish down day since mid-August. The bearish engulfing candle suggests the index is ready to begin a correction after its strong rally faltered around the February high. As outlined earlier in September, it appears that momentum has now realigned with its long-term uptrend which means it should eventually break to new highs once its current correction is complete.

ASX 200 Market Internals:

ASX 200: 7460.2 (0.58%), 16 September 2021

- Financials (0.86%) was the strongest sector and Healthcare (-0.4%) was the weakest

- 9 out of the 11 sectors closed higher

- 3 out of the 11 sectors outperformed the index

- 120 (60.00%) stocks advanced, 71 (35.50%) stocks declined

- 67% of stocks closed above their 200-day average

- 68% of stocks closed above their 50-day average

- 50.5% of stocks closed above their 20-day average

Outperformers:

- + 6.37% - Chalice Mining Ltd (CHN.AX)

- + 5.17% - AUB Group Ltd (AUB.AX)

- + 4.36% - Incitec Pivot Ltd (IPL.AX)

Underperformers:

- -6.8% - Redbubble Ltd (RBL.AX)

- -5.3% - Washington H Soul Pattinson and Company Ltd (SOL.AX)

- -4.9% - Pilbara Minerals Ltd (PLS.AX)

Forex: Dollar rises with retail sales

The US dollar dominated the currency space, which saw the US dollar index (DXY) close back above the monthly pivot and last week’s high, forming a bullish engulfing candle. This very much puts the dollar in the driving seat as we head into the weekend. EUR/USD is now comfortably below 1.1800 and USD/CHF is now probing the June high after several weeks of messy price action. Rising across the board, USD was stronger against emerging markets so it would appear something bigger may be going down, to the dollar’s advantage.

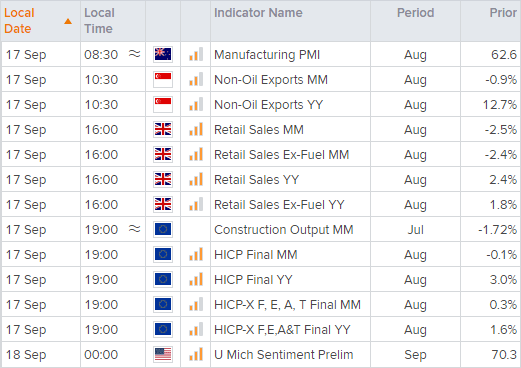

NZ business PMI is scheduled for 08:30 AEST and forecast to dip slightly to 61.8, which is still quite high considering Auckland remains in level 4 lockdown and the rest of the country remain in level 2 (to be reviews on Monday). The New Zealand dollar remains the strongest major in September and the past month, and this could strengthen further should we see further easing of restrictions. UK retail sales are up at 16:00 BST and the main event in the US session is the University of Consumer Sentiment Survey at midnight.

Learn how to trade forex

Commodities:

Oil prices stabilised just below Wednesday’s high, which suggests prices are trying to establish a new range after its breakout. A bullish engulfing candle formed on H4 timeframe to suggest a swing low may be in place at 71.48.

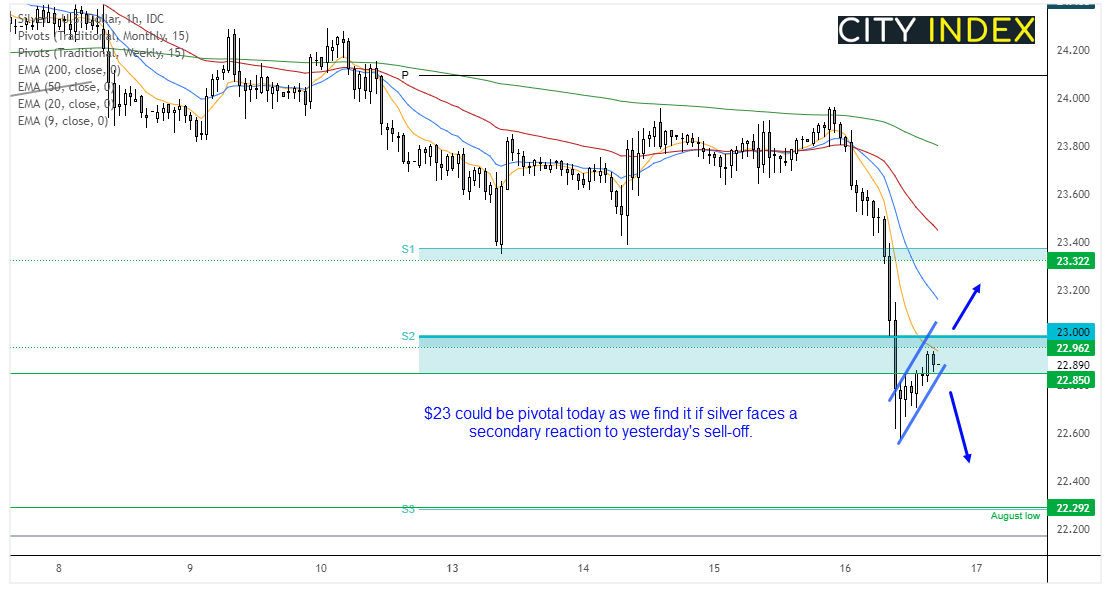

Gold and silver produced the more volatile reaction from strong retail sales overnight, falling -4.2% and -2.1% respectively. Out of the two, price action for silver appears to be the more vulnerable over the near-term.

Silver hit our $23.0 target overnight and even pushed prices beneath it. We can see on the hourly futures chart that silver saw rising volume during its decline overnight. After crashing through the August 20th low, prices have retraced in an orderly fashion but on lower volumes (corrective behaviour) and now treads water between the mentioned swing low and weekly S2 pivot. If we see a secondary response in Asia then we’d like to see $23 cap as resistance before bearish momentum returns. A break above $23 assumes a deeper countertrend move against yesterday’s selloff.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM