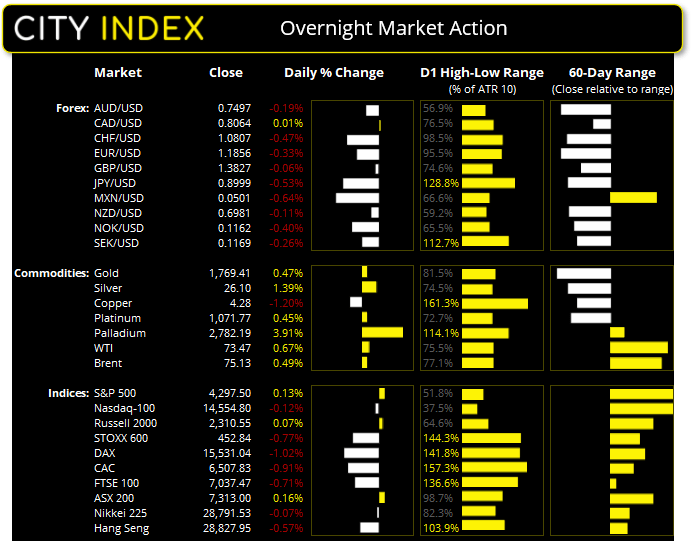

Asian Futures:

- Australia's ASX 200 futures are down -43 points (-0.59%), the cash market is currently estimated to open at 7,270.00

- Japan's Nikkei 225 futures are up 20 points (0.07%), the cash market is currently estimated to open at 28,811.53

- Hong Kong's Hang Seng futures are up 18 points (0.06%), the cash market is currently estimated to open at 28,845.95

UK and Europe:

- UK's FTSE 100 index fell -50.08 points (-0.71%) to close at 7,037.47

- Europe's Euro STOXX 50 index fell -43.21 points (-1.05%) to close at 4,064.30

- Germany's DAX index fell -159.55 points (-1.02%) to close at 15,531.04

- France's CAC 40 index fell -59.6 points (-0.91%) to close at 6,507.83

Wednesday US Close:

- The Dow Jones Industrial rose 210.22 points (0.61%) to close at 34,502.51

- The S&P 500 index rose 5.7 points (0.14%) to close at 4,297.50

- The Nasdaq 100 index fell -17.945 points (-0.12%) to close at 14,554.80

Learn how to trade indices

Strong month and quarter for US Indices:

Expectations for a strong NFP print tomorrow were given another boost overnight by a firm ADP employment report, with the private sector adding another 692k jobs following am 886 rise in May. This also follows on from yesterday’s consumer survey report which shows expectations for job availability to rise.

The S&P 500 rose for a fifth consecutive quarter and hit a record for a fifth straight day. 7 of its 11 sectors rose with the index, led by energy and consumer staples sectors. Value stocks also took the lead by rising 0.5% compared to -0.11% for growth stocks, although growth stocks outperformed the S&P 500 in June by rising 5.5%.

The Nasdaq 100 was down -0.12% by yesterday’s close but was a strong performer in June, rising 6.3% with the FANG index and biotech sector outperforming, with a 9.7% ad 8% rise in June respectively. Weak performers last month included the Nasdaq banking index at -6.1% and the housing index at -5.6%. Overall, it’s been a strong quarter for equities with the Nasdaq computer index rising 14%, FAANG stocks rising 12.9% and S&P 500 growth stocks rising 11.8%.

The ASX 200 has produced two volatile days of indecision, in opposite directions, effectively obliterating the symmetrical triangle at the month-end, quarter-end and end of financial year. With futures markets pointing to an open around 7270, then 7300 comes into focus as the first resistance level, with the next zone sitting around 7337 – 7374. Nearby support levels include 7260, 7243 and 7244.

ASX 200 Market Internals:

ASX 200: 7313 (0.16%), 29 June 2021

- Telecomm Services (2.66%) was the strongest sector and Healthcare (-0.81%) was the weakest

- 8 out of the 11 sectors closed higher

- 5 sectors outperformed the ASX 200

- 114 (57.29%) stocks advanced, 80 (40.20%) stocks declined

- 24 hit a new 52-week high, 4 hit a new 52-week low

- 71.86% of stocks closed above their 200-day average

- 64.32% of stocks closed above their 50-day average

- 54.27% of stocks closed above their 20-day average

Outperformers:

- + 11.7% - Iluka Resources Ltd (ILU.AX)

- + 4.71% - Clinuvel Pharmaceuticals Ltd (CUV.AX)

- + 4.65% - Chalice Mining Ltd (CHN.AX)

Underperformers:

- -12.9% - Nuix Ltd (NXL.AX)

- -9.99% - AGL Energy Ltd (AGL.AX)

- -9.46% - Kogan.com Ltd (KGN.AX)

Forex: Dollar’s most bullish month in 3.5 years

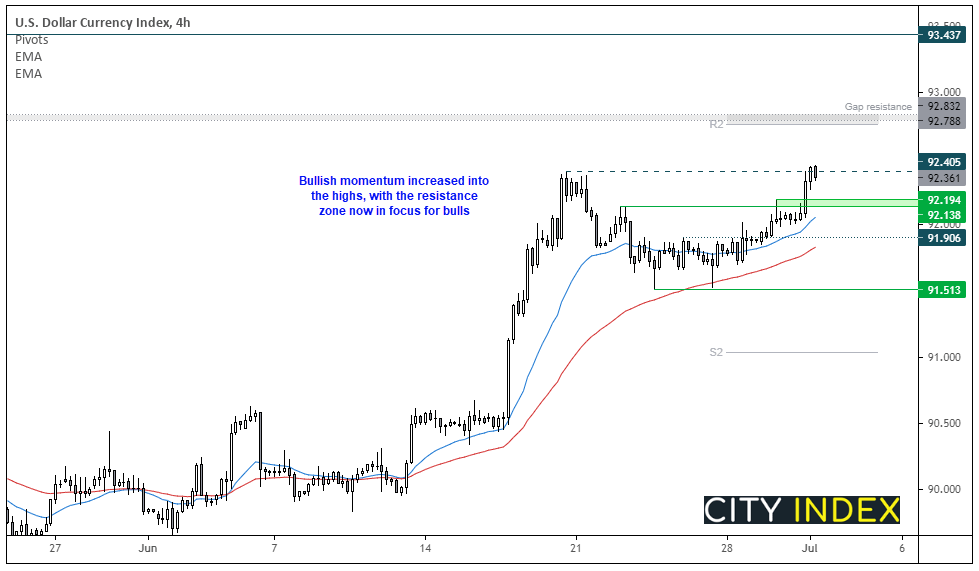

The US dollar index (DXY) rose to a 2.5 month high and enjoyed its most bullish month in 3.5 years. It has traded beyond our double bottom target at 92.30 and above its 50-week eMA, and is now resting just beneath the June high. We can see on the four-hour chart that bullish momentum has increased, so we are now looking for prices to hold above the 92.13/20 zone and head towards 92.76/83 zone where the weekly R2 pivot and gap resistance levels reside.

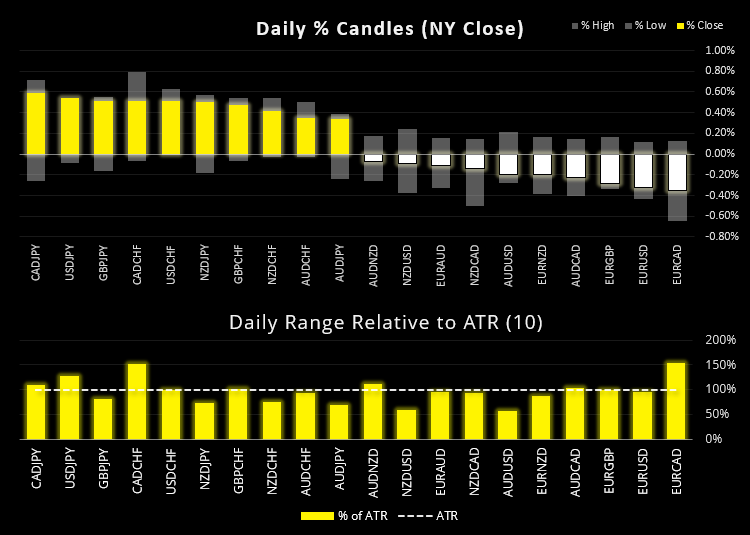

Safe-haven currencies CHF and JPY were the weakest currencies yesterday, CAD and GBP were the strongest. The Canadian dollar was higher against all but the dollar as GDP contracted less than feared. USD/CAD was effectively flat after hitting a seven-day higher earlier in the session. USD/CHF broke to a new cycle high beyond our initial 0.9230 high, with next resistance sitting at 0.9280 (weekly R pivot). AUD/USD and NZD/USD approached their cycle lows and extended losses beneath their 200-day eMA’s. All eyes will be on DXY to see if it can break higher and send such currencies (including EUR/USD) lower.

Learn how to trade forex

Commodities:

Oil prices were down ahead of today’s OPEC+ meeting, and brent futures are close to testing a bullish trendline on the four-hour chart. We suspect $74 could be a pivotal level if the trendline breaks. Currently markets are expecting an increase of 5000mn barrels per day, so any shortfall here could be bullish for oil (and less supply is hitting the market than expected).

Gold rose 0.5% and formed a bullish inside day, which like Tuesday’s candle failed to hold beneath 1756.24 support. This raises the possibility that a near-term floor is in place, although we would still consider a break below 1750 (Tuesday’s low) as a bearish trend continuation sign.

Silver had a more prominent close, rising 1.5% and forming a bullish engulfing day after finding support at 25.70. Combined with gold it would suggest a downside is not as imminent as it appeared this time yesterday.

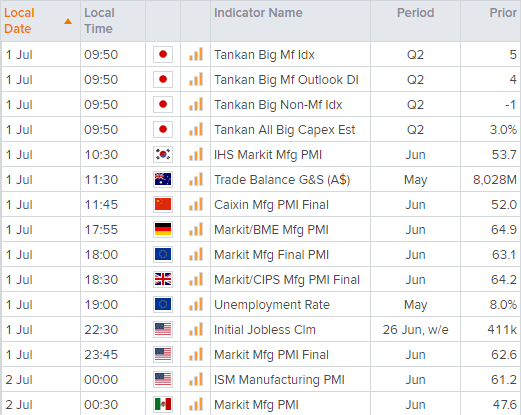

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Indices articles

Yesterday 03:30 PM

April 18, 2024 04:46 PM