Asian Futures:

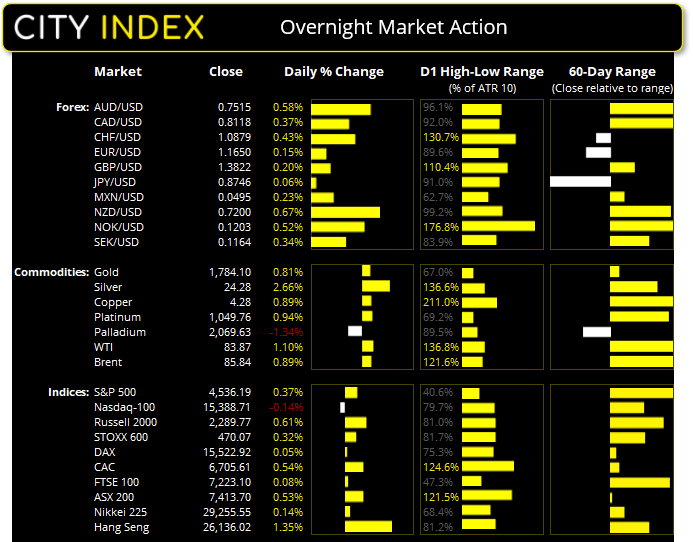

- Australia's ASX 200 futures are up 12 points (0.16%), the cash market is currently estimated to open at 7,425.70

- Japan's Nikkei 225 futures are down -20 points (-0.07%), the cash market is currently estimated to open at 29,235.55

- Hong Kong's Hang Seng futures are down -17 points (-0.06%), the cash market is currently estimated to open at 26,119.02

UK and Europe:

- UK's FTSE 100 index rose 5.57 points (0.08%) to close at 7,223.10

- Europe's Euro STOXX 50 index rose 5.34 points (0.13%) to close at 4,172.17

- Germany's DAX index rose 7.09 points (0.05%) to close at 15,522.92

- France's CAC 40 index rose 35.76 points (0.54%) to close at 6,705.61

Wednesday US Close:

- The Dow Jones Industrial rose 152.03 points (0.43%) to close at 35,609.34

- The S&P 500 index rose 16.56 points (0.37%) to close at 4,536.19

- The Nasdaq 100 index fell -22.012 points (-0.14%) to close at 15,388.71

Learn how to trade indices

Indices:

If we want to split hairs the S&P 500 closed -0.76 of a point below its record high (on a closing basis), although it’s a mere 9 points below if we use the intraday record high. Regardless, US indices rose in tandem as Q3 earnings continued to beat expectations. The S&P 500 value index hit a record high whilst the broader index is within striking distance of reaching its own milestone with a 0.21% gain led by the utility sector. Yet technology stocks underperformed to close -0.14% lower. In after-hour trade Tesla posted Q3 EPS at $1.86 (vs $1.59 expected) and revenue also exceeded expectations at $13.79 billion vs $16.63 estimated.

Wall Street were likely glad to hear that Democrats are reconsidering raising taxes on “businesses, high income individuals or capital gains” due to opposition from Dem Senator Kyrsten Sinema opposition against it, according to a report from the Wall Street Journal.

ASX 200 Market Internals:

ASX 200: 7413.7 (0.53%), 20 October 2021

- Information Technology (1.07%) was the strongest sector and Energy (-1%) was the weakest

- 9 out of the 11 sectors closed higher

- 2 out of the 11 sectors closed lower

- 3 out of the 11 sectors outperformed the index

- 127 (63.50%) stocks advanced, 59 (29.50%) stocks declined

- 68% of stocks closed above their 200-day average

- 53% of stocks closed above their 50-day average

- 64% of stocks closed above their 20-day average

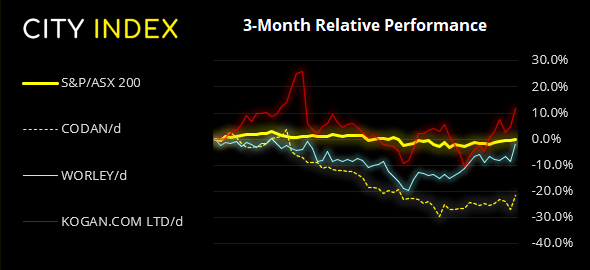

Outperformers:

- + 7.59%-Codan Ltd(CDA.AX)

- + 7.53%-Worley Ltd(WOR.AX)

- + 6.68%-Kogan.com Ltd(KGN.AX)

Underperformers:

- -7.85%-Whitehaven Coal Ltd(WHC.AX)

- -4.79%-Flight Centre Travel Group Ltd(FLT.AX)

- -4.34%-Star Entertainment Group Ltd(SGR.AX)

Forex:

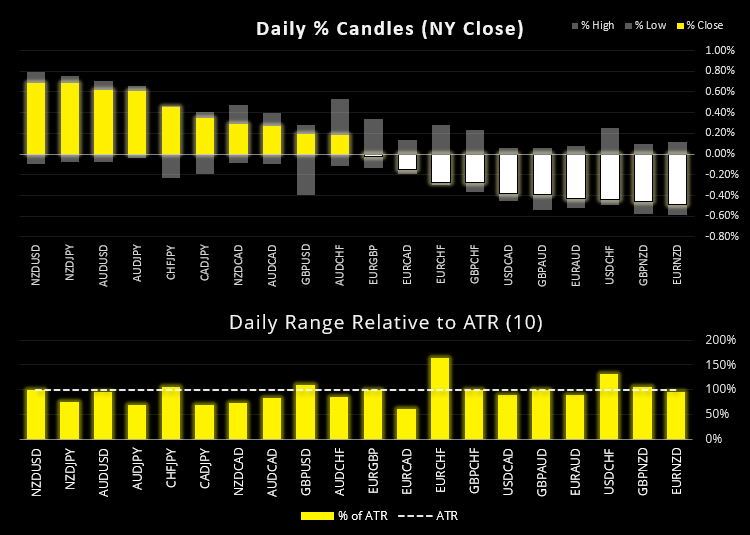

Centrist FOMC member Randal Quarles does not believe the Fed is behind the curve regarding fighting inflation, although does support tapering in November. This is at odds with comments made by his colleague Christopher Weller yesterday that inflation remains the biggest threat to the Fed. Regardless, the US dollar index (DXY) printed a bearish inside day and held above 94.50 support which may prove to be a pivotal level over the next couple of days.

NZD remained the best performing currency and closed around 0.72 – its highest level since June. NZD/JPY and NZD/EUR rallied to a 4-year high. GBP/NZD hit our bearish target just above the May low during its 5th consecutive bearish session. Momentum breaking out of its multi-week retracement suggests support could eventually break as its downtrend resumes. However, AUD is putting up a bit of a fight with AUD/NZD trying to hold above the December low, although we suspect it could give way in due course.

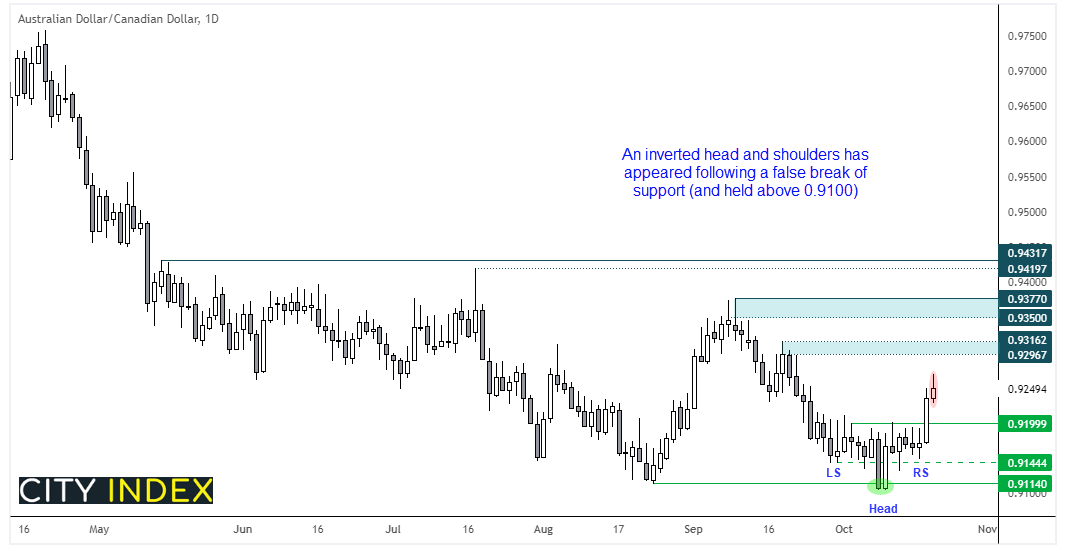

Canadian inflation hit an 18-year high although this is roughly in line with expectations. Still, overnight swap markets are pricing in a hike by early 2022, and potentially 3 by the end of next year – which is much more aggressive than BOC are currently letting on. USD/CAD touched a 3-month low yet remains above 1.3000. However, AUD/CAD appears to be reversing course.

AUD/CAD tried (yet failed) to break to new lows and found support at 0.91 with a 2-bar bullish reversal. This turned out to be the ‘head’ of an inverted head and shoulders pattern which was confirmed with yesterday’s break above 0.9200. A bearish hammer formed by today’s close to warn of near-term exhaustion, so perhaps we’ll now see a minor pullback towards the neckline ahead of its next leg higher.

Commodities:

So much for the pause in oil prices. After an initial break to a 4-day low, WTI rose over 1.1% as the weekly EIA report shows demand for crude remained strong and supply was tight. The day closed with a bearish outside day on above-average volume. Next resistance is $84 and $85.90.

Silver hit our 24.40 target projected form the inverted head and shoulders pattern on the daily chart, and bull flag breakout on the four-hour chart. As we suspect this is a change in trend we currently anticipate prices could continue higher, although the reward to risk ratio is not ideal around current levels on the daily chart.

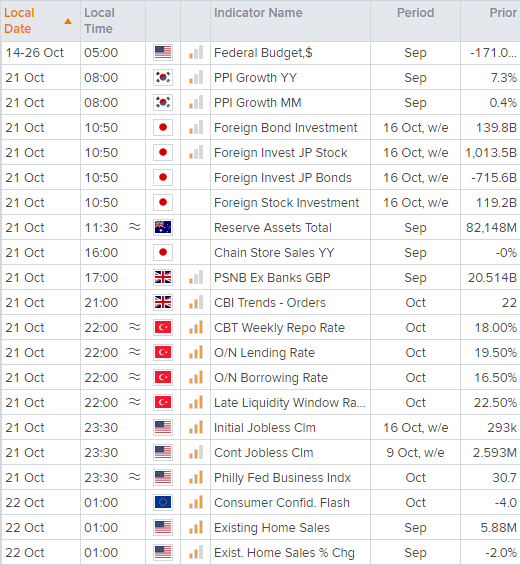

Up Next (Times in AEDT)

How to trade with City Index

You can trade easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Trade Ideas articles

Yesterday 11:00 AM

Yesterday 08:15 AM

Yesterday 05:45 AM