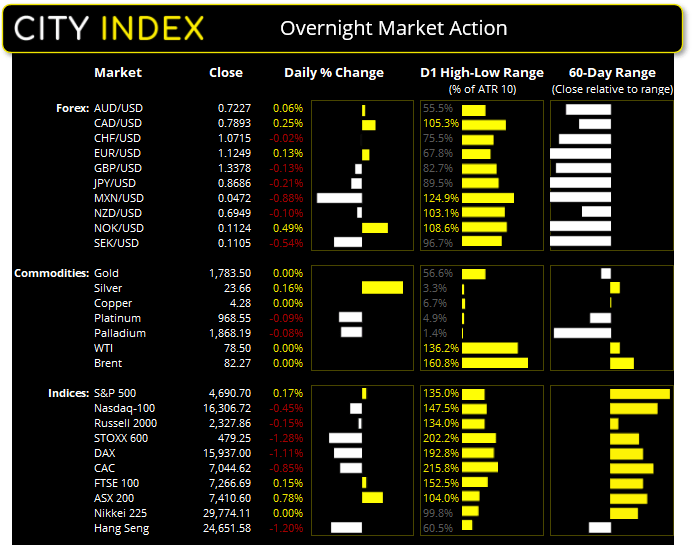

Asian Futures:

- Australia's ASX 200 futures are up 1 points (0.01%), the cash market is currently estimated to open at 7,411.60

- Japan's Nikkei 225 futures are down -110 points (-0.37%), the cash market is currently estimated to open at 29,664.11

- Hong Kong's Hang Seng futures are down -11 points (-0.04%), the cash market is currently estimated to open at 24,640.58

- China's A50 Index futures are down -18 points (-0.12%), the cash market is currently estimated to open at 15,631.60

UK and Europe:

- UK's FTSE 100 index rose 11.23 points (0.15%) to close at 7,266.69

- Europe's Euro STOXX 50 index fell -54.87 points (-1.26%) to close at 4,283.82

- Germany's DAX index fell -178.69 points (-1.11%) to close at 15,937.00

- France's CAC 40 index fell -60.38 points (-0.85%) to close at 7,044.62

Tuesday US Close:

- The Dow Jones Industrial rose 194.55 points (0.55%) to close at 35,813.80

- The S&P 500 index rose 7.76 points (0.17%) to close at 4,690.70

- The Nasdaq 100 index fell -74.262 points (-0.45%) to close at 16,306.72

Oil prices get the Biden-bounce

The US delved into their oil reserves, a move that was floated by Biden in an attempt to cap oil prices. And as the release of 50 million barrels was less than expected (and already well telegraphed) oil prices actually rose around 3%. $80 is the next key level for bulls to conquer after printing a 3-day bullish reversal at a potential corrective low.

Euro lifted on improved business sentiment

Better-than expected business sentiment for the eurozone helped alleviate selling pressure on euro crosses. Manufacturing PMI rose to 55.8 from 54.2. EUR/JPY bounced for a second session after finding support at the August and September lows. EUR/NZD bounced from its YTD lows around 1.6065 whilst EUR/GBP and EUR/CHF made a similar move after refusing to probe Monday’s YTD lows. However, with the potential for lockdowns over Christmas then this could be a dead-cat bounce, so as of yet not ready to call a reversal for the unloved euro.

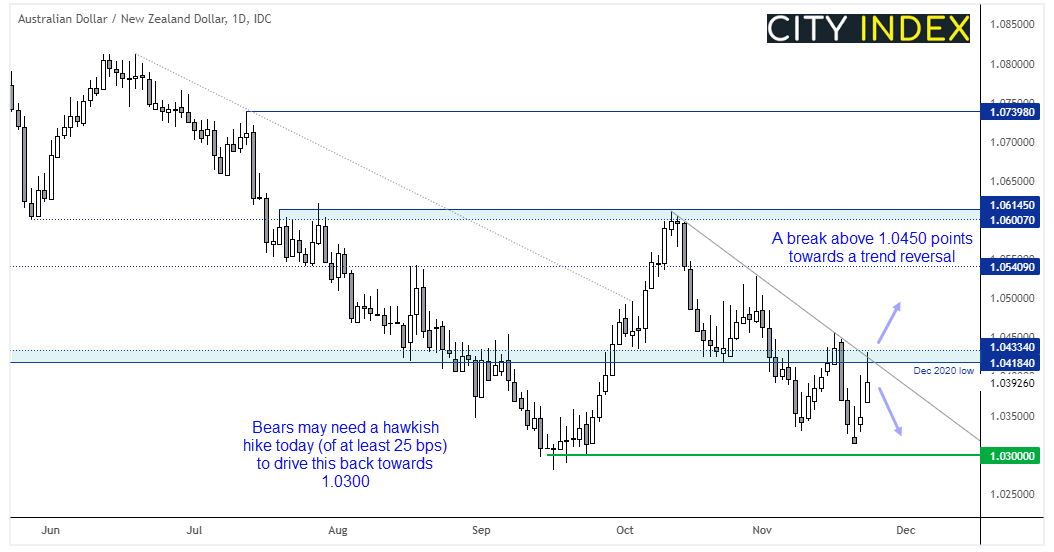

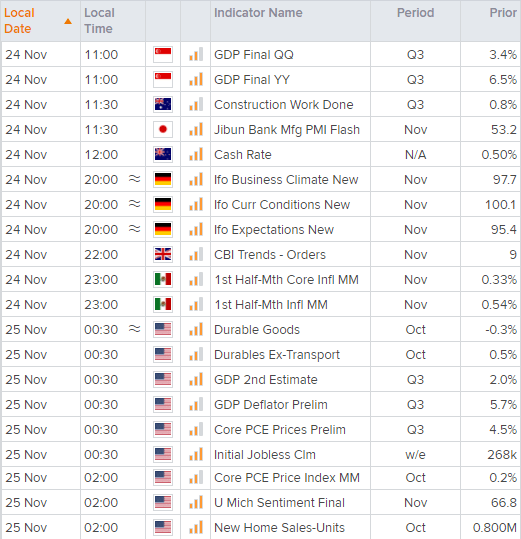

RBNZ are expected to raise rates today – but by how much remains the question

On aggregate, data from New Zealand has continued to warrant at least a 25 bps hike and there has been much speculation that it could be as much as 50 bps. Unemployment is at a record low, inflation is at 4.9% and inflation forecasts were revised higher to 2.9% for the +1 year and 3.7% for the +2 year. Perhaps there is a case for the OCR at 1%, although what makes us wary is that RBNZ already offer the highest rates among FX majors and that they had reminded markets that central banks tend to cut aggressively and hike slowly (even going as far to say hikes are usually 25 bps). Whilst OIS (overnight index swaps) have fully priced in a 25 bps hike, we need to look 6 month south before OIS fully prices in a 50 bps hike. So, 25 bps looks more likely today but that is no reason to not prepare for a 50.

AUD/NZD probed the December 2020 lows and tested trend resistance overnight. And we see the potential to break higher should RBNZ only hike by 25 bps. There has been much speculation over the last several weeks of today’s hike so it is already old news, and a ‘mere’ 25 bps hike could shake out some bullish NZD positions in the process. We would either require a 50 bps hike or a ‘hawkish; 25 bps hike today to see AUD/NZD retest 1.0300.

Technically, a higher low formed above 1.0300 and its decline from the 1.0615 high appears to be corrective in nature due to the overlapping of the swings. Still, at current levels it remains favourable to bearish swing traders, should today’s meeting deliver the hawkish goods. Whilst a break above 1.0450 could be taken as a sign of its bullish reversal.

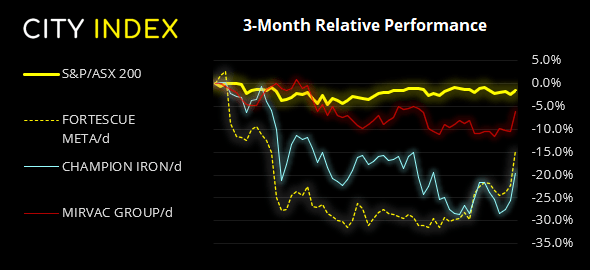

The ASX rallied with iron ore prices yesterday

The ASX 200 made ‘short’ work of our bearish bias yesterday, rallying from the open despite the weak lead from Wall Street and negative sentiment across other parts of APAC. Mining companies were top of the pack as iron ore prices ripped higher, as traders speculated the resumption of steel production in China. Therefore, iron ore is clearly a market to watch today for sentient of the ASX. Take note of the resistance zone around 7431 – 7442 as we likely need a break above it for any rally to be sustained.

ASX 200: 7410.6 (0.78%), 23 November 2021

- Energy (2.54%) was the strongest sector and Information Technology (-3.49%) was the weakest

- 8 out of the 11 sectors closed higher

- 3 out of the 11 sectors closed lower

- 6 out of the 11 sectors outperformed the index

- 112 (56.00%) stocks advanced, 82 (41.00%) stocks declined

- 64% of stocks closed above their 200-day average

- 60.5% of stocks closed above their 50-day average

- 49.5% of stocks closed above their 20-day average

Outperformers:

- + 9.81%-Fortes

- cue Metals Group Ltd(FMG.AX)

- + 8.04%-Champion Iron Ltd(CIA.AX)

- + 5%-Mirvac Group(MGR.AX)

Underperformers:

- -9.58%-Bapcor Ltd(BAP.AX)

- -5.63%-WiseTech Global Ltd(WTC.AX)

- -5.6%-Silver Lake Resources Ltd(SLR.AX)

Up Next (Times in AEDT)

How to trade with City Index

You can easily trade with City Index by using these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Trade Ideas articles

Yesterday 03:00 PM

Yesterday 11:14 AM

April 24, 2024 11:00 AM

April 24, 2024 08:15 AM