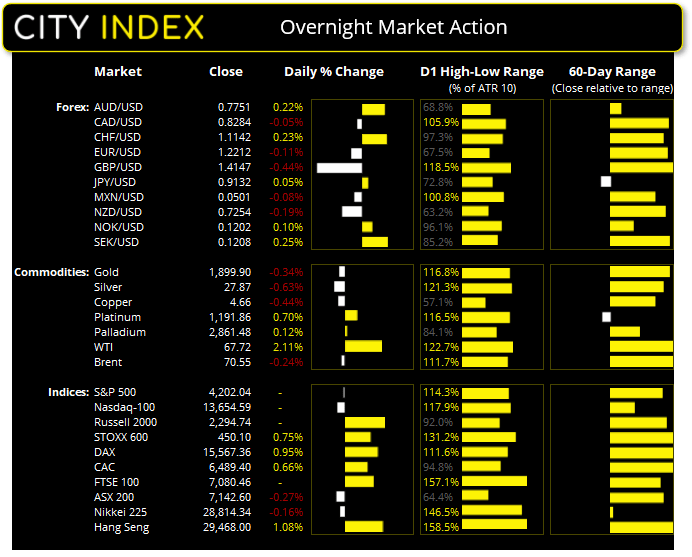

Asian Futures:

- Australia's ASX 200 futures are up 12 points (0.17%), the cash market is currently estimated to open at 7,154.60

- Japan's Nikkei 225 futures are down 0 points (0%), the cash market is currently estimated to open at 28,814.34

- Hong Kong's Hang Seng futures are down -53 points (-0.18%), the cash market is currently estimated to open at 29,415.00

UK and Europe:

- UK's FTSE 100 index rose 57.85 points (0.82%) to close at 7,080.46

- Europe's Euro STOXX 50 index rose 32.29 points (0.8%) to close at 4,071.75

- Germany's DAX index rose 146.23 points (0.95%) to close at 15,567.36

- France's CAC 40 index rose 42.23 points (0.66%) to close at 6,489.40

Tuesday US Close:

- The Dow Jones Industrial rose 45.86 points (0.13%) to close at 34,575.31

- The S&P 500 index fell -2.07 points (-0.05%) to close at 4,202.04

- The Nasdaq 100 index fell -31.923 points (-0.23%) to close at 13,654.59

Learn how to trade indices

Wall Street mixed, S&P 500 flirts with double top pattern

ISM manufacturing rose to 61.2 in May, up from 60.7 in April taking it to a twelfth consecutive month of expansion. New orders rose 2.7 points to 67 (just below its multi-year high) although prices paid (inflation) were down to 88 from 89.6. The employment index also expanded at its slowest pace in six months at 50.9 unfinished work accumulated due to a shortage of labour and shortage of raw materials. On the inflation front, 88 for prices paid is still a punchy number and no doubt driven by a supply shortage. But if these supply issues persist then they could creep into inflation numbers and make it less of a ‘transitory’ issue the Fed are currently expecting.

It was mixed on Wall Street with the S&P 500 and Nasdaq 100 closing -0.05% and -0.23% lower, whilst the Dow Jones and Russell 2000 rose 0.13% and 1.14%. Yet the more compelling observation is the bearish outside candle on the S&P 500 and its upper wick which just failed to retest a record high, leaving a potential double top around 4235/38.

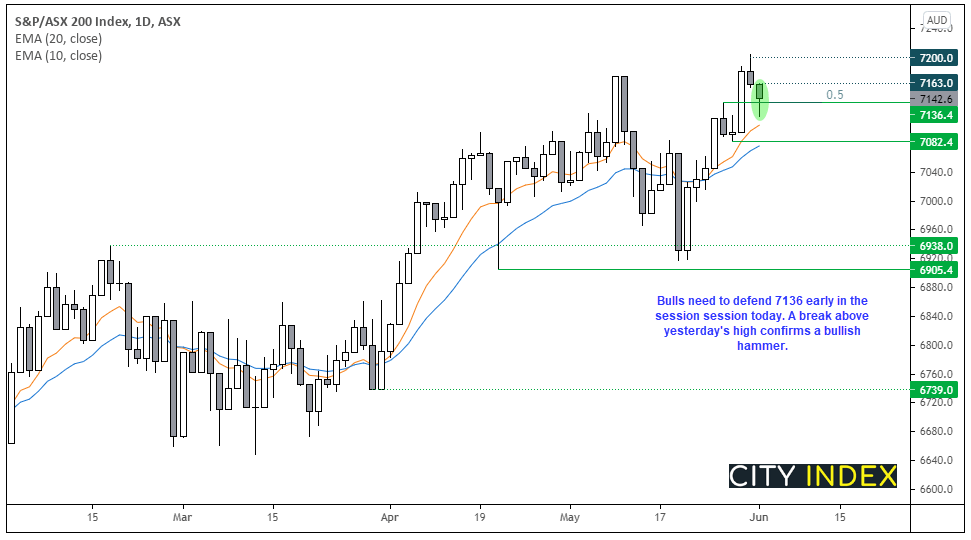

The ASX 200 has retraced for two days after setting a new-record high last week. Yesterday we suggested that bulls needed to defend 7136 support and, to a degree they have. A bullish hammer closed back above this level (just) and the Marabuzo line (50% retracement of the large bullish candle’s body). So from here it may be straight forward; a break above yesterday’s high confirms the bullish candle and brings 7200 back into focus, whilst a dip back below 7136 early trade paints an intraday bearish bias, and a break beneath yesterday’s low invalidates the bullish bias on the daily timeframe.

ASX 200 Market Internals:

ASX 200: 7142.6 (-0.27%), 01 June 2021

- Energy (1.34%) was the strongest sector and Healthcare (-0.7%) was the weakest

- 7 out of the 11 sectors outperformed the index

- 10 out of the 11 sectors closed lower

- 65 (32.50%) stocks advanced, 122 (61.00%) stocks declined

- 1 hit a new 52-week high, 0 hit a new 52-week low

- 68% of stocks closed above their 200-day average

- 57.5% of stocks closed above their 50-day average

- 65.5% of stocks closed above their 20-day average

Outperformers:

- + 5.71% - Whitehaven Coal Ltd (WHC.AX)

- + 3.22% - Reece Ltd (REH.AX)

- + 3.07% - Megaport Ltd (MP1.AX)

Underperformers:

- -4.99% - Blackmores Ltd (BKL.AX)

- -4.89% - Lynas Rare Earths Ltd (LYC.AX)

- -4.43% - Polynovo Ltd (PNV.AX)

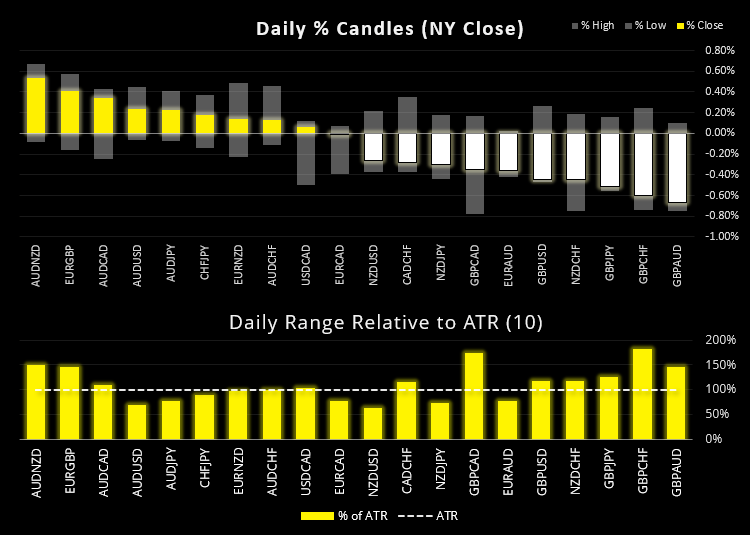

Forex: New Covid variant weighs on GBP

The British pound came under pressure after a new variant in the UK threatens to postpone the easing of lockdown restrictions. GBP/USD produced a bearish engulfing candle after printing an intraday three-year high. GBP/AUD was the weakest cross thanks to a rising Aussie dollar but also lost ground to safe haven currencies JPY and CHF.

AUD was the strongest major overnight (and currently the strongest this week so far). AUD/NZD has rallied straight into the resistance zone mentioned in yesterday’s report after finding demand around 1.0600 last week. Whilst the original idea was to then seek bearish setups around current levels, yesterday’s bullish expansion was stronger than we’d like. Still, GDP is due out later today so perhaps a weak print could take them steam out of this move and carve a top. A break above 1.0714 removes it from the short watchlist. AUD/CAD remains within its 0.6925 – 0.6980 range, a break either side of which could signal its next directional move.

Rising oil prices were a tailwind for the Canadian dollar which saw USD/CAD briefly touch its lowest level in six years. The session closed with a bullish pinbar above support failing to test 1.2000. If oil prices are to come off form their highs then USD/CAD may be a contender for a counter-trend setup over the near-term.

Learn how to trade forex

Commodities: Oil prices on the rise, Gold and silver wobble

OPEC+ members agreed they stick to the plan and easy supply curbs gradually throughout July, with OPEC’s Secretary General Barkindo saying the return of Iranian oil supply will also be orderly. With Chinese demand continuing to recover and lockdown restrictions being lifted globally, demand has risen as expected and so far fended off fears of an oversupply from Iran. OPEC’s next meeting is scheduled for July 1st.

Brent futures settled to their highest levels in March, although hit an intraday high of two-years with an earlier spike above $71.0. WTI futures rose to 68.87 before settling right on the March 2021 high at 67.98.

Gold is looking shaky at its highs after printing a volatile bearish outside day. Whilst it closed at 1900, yesterday’s bearish reversal candle was its four over five days. Our bias now is for a choppy retracement towards 1875.

Silver is making harder work of further gains, printing a bearish pinbar which failed to hold above the February 23rd high and creating a lower high beneath the May high. This has now been removed from the bullish watchlist (even though its bullish channel remains intact). A break below 27.20 confirms a trend reversal.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM