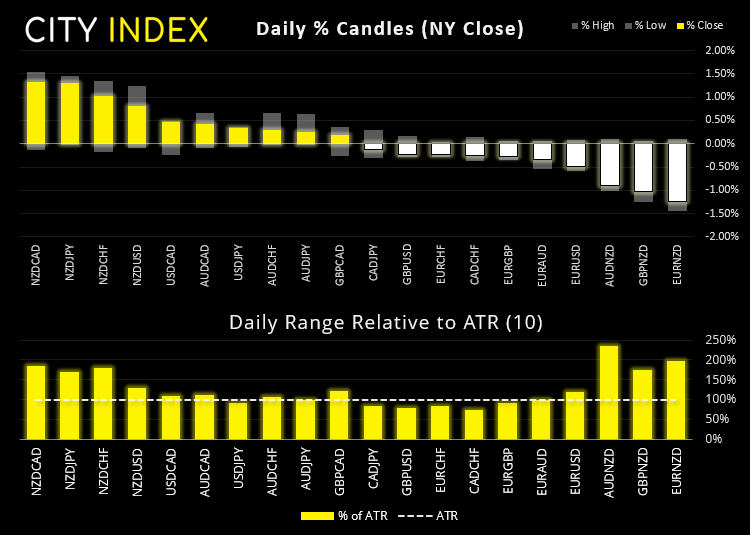

RBNZ’s hawkish surprise saw the Kiwi dollar trade higher through all three sessions yesterday. It also appears to have spurned some profit taking on an (arguably) over-stretched Canadian dollar.

Asian Futures:

- Australia's ASX 200 futures are up 3 points (0.04%), the cash market is currently estimated to open at 7,095.50

- Japan's Nikkei 225 futures are up 30 points (0.1%), the cash market is currently estimated to open at 28,672.19

- Hong Kong's Hang Seng futures are up 25 points (0.09%), the cash market is currently estimated to open at 29,191.01

UK and Europe:

- UK's FTSE 100 index fell -2.86 points (-0.04%) to close at 7,026.93

- Europe's Euro STOXX 50 index fell -4.37 points (-0.11%) to close at 4,031.67

- Germany's DAX index fell -14.37 points (-0.09%) to close at 15,450.72

- France's CAC 40 index rose 1.33 points (0.02%) to close at 6,391.60

Wednesday US Close:

- The Dow Jones Industrial rose 10.59 points (0.03%) to close at 34,323.05

- The S&P 500 index rose 7.86 points (0.19%) to close at 4,195.99

- The Nasdaq 100 index rose 45.011 points (0.33%) to close at 13,702.74

Learn how to trade indices

Narrow ranges for US indices

Narrow ranges on Wall Street saw minor gains for the Nasdaq 100, S&P 500 and Dow Jones, although small caps took the lead with the Russell 2000 rising nearly 2% on its way to a bullish engulfing day.

The Nikkei 225 produced a bullish engulfing candle yesterday, although it is approaching the April 30th low at 28,760 and appears to still be in a countertrend move. Should resistance hold and bearish momentum return, we’d keep an eye out for a break beneath trendline support on the daily chart to signal its next leg lower.

An outbreak in Victoria, Australia weighed on the ASX 200 yesterday the Melbourne now faces the prospects of new restrictions making a return. Closing back beneath 7100 and breaking a four-day rally, eyes will be on a potential announcement today after the government said yesterday that “the next 4 hours are critical” as to how they respond to the rise in cases. Key support for bulls to defend to day are 7083, 7066 and 7053.

ASX 200 Market Internals:

ASX 200: 7092.5 (-0.32%), 26 May 2021

- Information Technology (1.11%) was the strongest sector and Materials (-1.15%) was the weakest

- 6 out of the 11 sectors closed higher

- 7 out of the 11 sectors outperformed the index

- 82 (41.00%) stocks advanced, 104 (52.00%) stocks declined

- 16 hit a new 52-week high, 0 hit a new 52-week low

- 67.5% of stocks closed above their 200-day average

- 51.5% of stocks closed above their 50-day average

- 57% of stocks closed above their 20-day average

Outperformers:

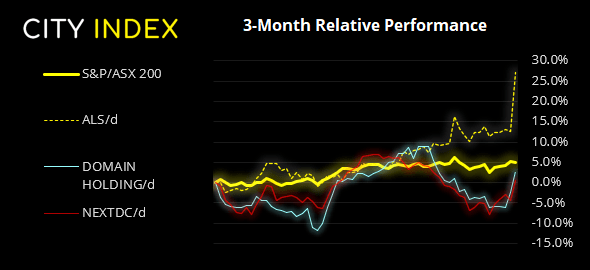

- + 12.8% - ALS Ltd (ALQ.AX)

- + 5.26% - Domain Holdings Australia Ltd (DHG.AX)

- + 5.17% - NEXTDC Ltd (NXT.AX)

Underperformers:

- -5.73% - Kogan.com Ltd (KGN.AX)

- -5.01% - OZ Minerals Ltd (OZL.AX)

- -4.91% - Redbubble Ltd (RBL.AX)

Forex: US dollar index back above 90

The US dollar index (DXY) closed above 90.0 after just one day beneath it, which puts this week’s candle currently on track for a second small bullish hammer (and second consecutive one at the lows). Shorting the dollar is not a new idea and we remain wary that its downtrend will persist in such a straight line, especially that it is now struggling to hold beneath 90.0 and above the January low. This may not be enough to warrant a long-dollar mindset by itself, but something for bears to consider before they go ‘all in’ at these lows.

Euro was broadly lower overnight on the back of a stronger dollar, quickly invalidating our bullish bias on EUR/GBP and taking EUR/USD back below its previous day’s breakout level. EUR/JPY is also back beneath the September 2018 high after reaching our initial both our targets from a bull flag breakout on Tuesday, placing it on the back burner for now.

The Kiwi Dollar extended gains through the European and US session after rallying from RBNZ’s hawkish meeting yesterday. RBNZ’s hawkish surprise made them the third central bank to talk normalisation, making the Kiwi dollar by far the strongest currency and closing broadly higher.

AUD/NZD fell like a rock and broken beneath our initial 1.0640 target overnight. Given RBA have no intention of normalising their policy over the next couple of years, our core view remains bearish on this cross, even if near-term technicals are stretched.

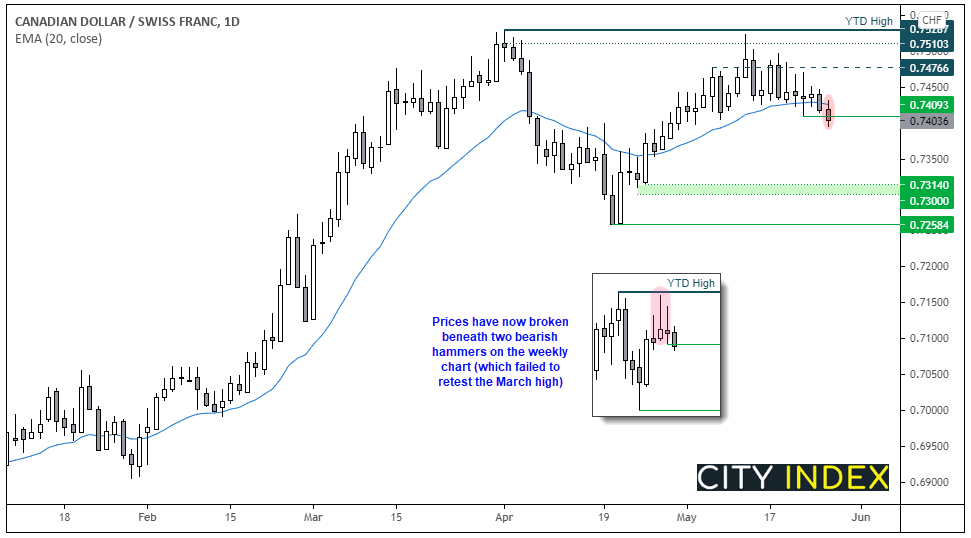

We mentioned in Monday’s Asian Open report that CAD long positioning was at +2.6 standard deviations, so potentially at a technical extreme. Matt Weller sees a case for USD/CAD to bottom and there are signs elsewhere that CAD could indeed begin to retrace. Last week me mentioned that we were watching CAD/CHF for a potential short, given its two bearish hammers failed to retest the March high. Prices have now drifted beneath their lows, so it may only take a spark of risk-off to trigger a bearish follow through (as nervous longs weigh up the risks-off a sentiment extreme on CAD).

We can see on the daily chart it has closed beneath recent low and is now below its 20-day eMA. As this is a potential top it may take a whilst and, as its from a weekly signal, we’ll have a wider ‘invalidation point’ up at the 0.7466 high. But, if risk-off sentiment is to return the crosses such as CAD/CHF are vulnerable to a quick sell-off.

Learn how to trade forex

Commodities: Gold and silver feel their own weight at their highs

Gold and silver failed to hold onto earlier gains, seeing gold close below 1900 with a bearish pinbar to warn of trend exhaustion, and silver printing a bearish engulfing candle and falling back below 28.0. Whilst this raises the prospect of a retracement or consolidation for gold, silver is a choppy meal at the best of times and remains in its bullish channel and above 27.20 support, so we’d reconsider the long bias should a new level of support build form here. Direct losses puts it on the back burner.

Oil prices remained elevated yet ultimately flat overnight. WTI futures settled at 66.16 and trades in a tight intraday channel near May’s highs whilst brent sits at 68.84.

Platinum futures produced a bearish pinbar which closed back below 1207.90 (our original invalidation point) so our bearish bias remains in place. We now need momentum to return and prices remain beneath the revised level at yesterday’s high of 1217.60.

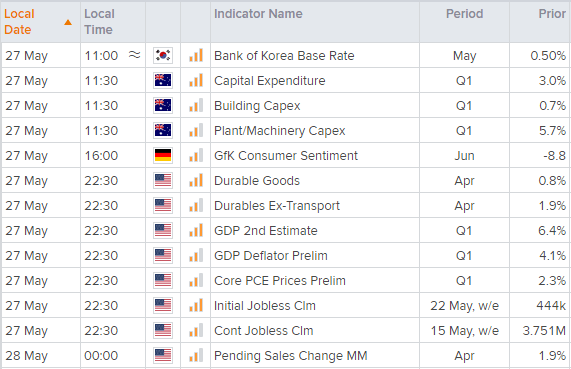

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 08:18 AM

Yesterday 10:40 PM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM