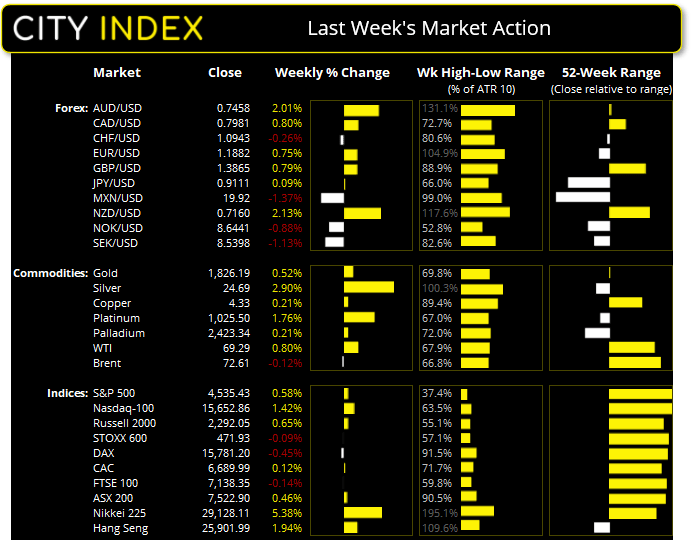

Asian Futures:

- Australia’s ASX 200 futures are down -23 points (-0.306%), the cash market is currently estimated to open at 7499.9

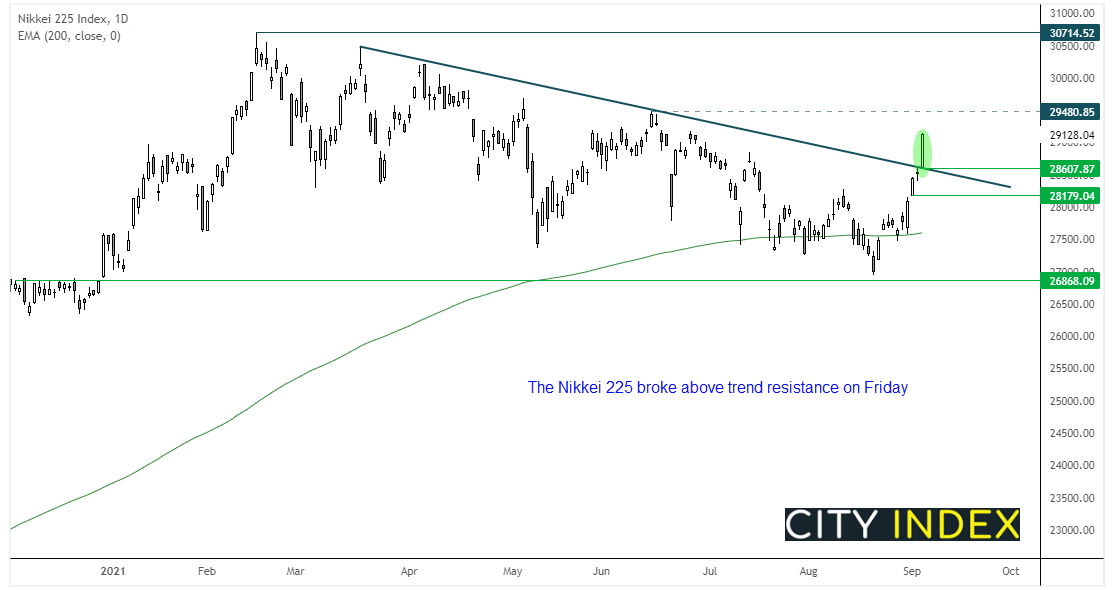

- Japan's Nikkei 225 futures have risen 420 points (1.44%), the cash market is currently estimated to open at 29548.11

- Hong Kong's Hang Seng futures are up 36 points (0.14%), the cash market is currently estimated to open at 25937.99

European Friday close:

- UK's FTSE 100 index fell -25.55 points (-0.36%) to close at 7138.35

- Europe's Euro STOXX 50 index fell -30.12 points (-0.71%) to close at 4201.98

- Germany's DAX index fell -59.39 points (-0.37%) to close at 15781.2

- France's CAC 40 index fell -73.09 points (-1.08%) to close at 6689.99

US Friday close:

- The Dow Jones fell -74.71 points (-0.21%) to close at 35,369.09

- The S&P 500 fell -1.52 points (-0.04%) to close at 4,535.43

- The Nasdaq 100 rose 48.611 points (0.31%) to close at 15,652.86

Learn how to trade indices

Indices tread water just off record highs

Wall Street indices continued to hover near their record highs following a huge miss on Friday’s Nonfarm Payroll report. The S&P 500 closed effectively flat at -0.03%, forming a second consecutive Doji and low daily range. Only 5 of the 11 sectors finished higher with tech stocks leading whilst utilities were the weakest. On the week it gained just 0.58% although it has risen 5.5% this quarter and 20.7% this year so far. The Nasdaq rose 0.3% on Friday and remains the general outperformer with its 0.45% gain last week, 7.5% this quarter and 21.5% this year.

The ASX 200 rose on Friday to close in the top quarter of the 7430 – 7543 range. As it found support at its 50-day eMA and daily trend support we now favour an eventual break above the range. Until that happens, range-trading strategies are preferred.

The Nikkei 225 broke above a significant retracement line on Friday after Japan’s stand-in PM confirmed he will not run again in the elections later this month. Popular guy! Overall, the Nikkei has been in a strong uptrend since March 2020 (like global indices in general) but in a shallow, yet extended correction since March this year. Yet the pickup in bullish momentum suggests the established uptrend is set to resume.

ASX 200 Market Internals:

ASX 200: 7522.9 (0.50%), 05 September 2021

- Materials (1.17%) was the strongest sector and Information Technology (-0.76%) was the weakest

- 9 out of the 11 sectors closed higher

- 3 out of the 11 sectors closed lower

- 4 out of the 11 sectors outperformed the index

- 138 (69.00%) stocks advanced, 53 (26.50%) stocks declined

- 70% of stocks closed above their 200-day average

- 66% of stocks closed above their 50-day average

- 61.5% of stocks closed above their 20-day average

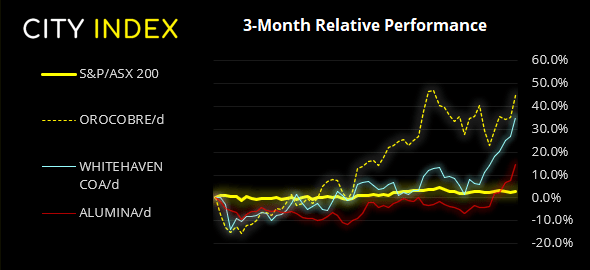

Outperformers:

- + 6.99% - Orocobre Ltd (ORE.AX)

- + 6.77% - Whitehaven Coal Ltd (WHC.AX)

- + 6.68% - Alumina Ltd (AWC.AX)

Underperformers:

- -3.00% - BlueScope Steel Ltd (BSL.AX)

- -2.97% - Ramelius Resources Ltd (RMS.AX)

- -2.77% - Afterpay Ltd (APT.AX)

Forex:

The US dollar index (DXY) fell to a 1-month low on Friday. However, it’s looking overstretched to the downside. It’s fallen nearly -2% since the August high with no obvious pullbacks, and Friday printed a ‘buying tail’ (lower wick) so a countertrend bounce this week seems feasible.

EUR/USD tested the July high on Friday, although it formed a bearish hammer ad closed back below its 200-day eMA. We now favour mean reversion over the near-term, although a break above Friday’s high paves the way for trend continuation.

AUD/USD rose to a 7-week high and probed its 200-day eMA on Friday. Given the potential for DXY to bounce and the Aussie testing its long-term average then the potential for a pause in trend or retracement.

Learn how to trade forex

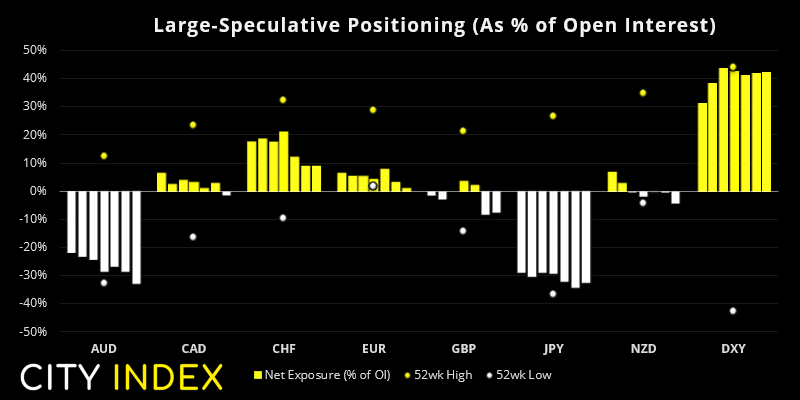

From the Weekly COT Report (Commitment of Traders)

From Tuesday 31st August 2021:

- Markets increased their net-long exposure to the US dollar by +$2.3 billion, taking it to a total of $10.7 billion ($11.1 billion againstG10 currencies and -$0.4 billion against emerging market currencies).

- Large speculators were their most bearish on AUD futures since September 2019. However, that now seems like a moot point given the rally on AUD last week as short covering has clearly taken hold due to the perpetually dovish Fed.

- Traders increased their short-exposure to NZD futures as the COVID-19 cases rose and lockdowns were extended. However, restrictions have since been eased so we suspect that traders won’t remain net-short for too much longer.

- Traders flipped to net-short exposure to CAD futures since December.

Commodities:

The CRB commodities index turned higher on Friday which suggests a swing low is in place at 216.75. A break above 221.25 assumes bullish continuation in line with its dominant trend.

Gold hit our 1834 target on Friday, all thanks to the weak NFP print. If prices can stabilise around last week’s highs then odds are on for a breakout above 1834.14. We’d need to see a break below 1803 to switch to a bearish bias.

A flat close for oil resulted in a Rikshaw man doji on the weekly chart below 70. This places a range between 67 – 70 an, until prices break out of one of those levels we favour range-trading strategies.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM