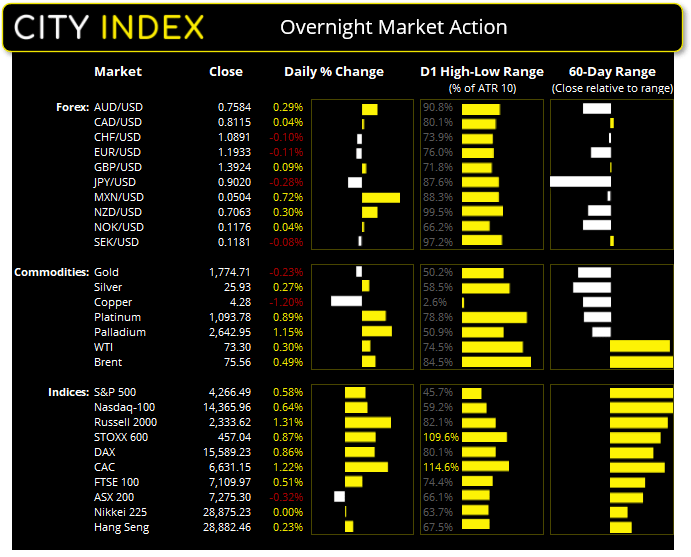

Asian Futures:

- Australia's ASX 200 futures flat, the cash market is currently estimated to open at 7,275.30

- Japan's Nikkei 225 futures are up 190 points (0.66%), the cash market is currently estimated to open at 29,065.23

- Hong Kong's Hang Seng futures are up 75 points (0.26%), the cash market is currently estimated to open at 28,957.46

UK and Europe:

- UK's FTSE 100 index rose 35.91 points (0.51%) to close at 7,109.97

- Europe's Euro STOXX 50 index rose 46.49 points (1.14%) to close at 4,122.43

- Germany's DAX index rose 132.84 points (0.86%) to close at 15,589.23

- France's CAC 40 index rose 80.08 points (1.22%) to close at 6,631.15

Thursday US Close:

- The Dow Jones Industrial rose 322.58 points (0.95%) to close at 34,196.82

- The S&P 500 index rose 24.65 points (0.59%) to close at 4,266.49

- The Nasdaq 100 index rose 91.716 points (0.64%) to close at 14,365.96

Learn how to trade indices

US indices hit new highs on bipartisan deal:

Wall Street finished on a high note as US President Joe Biden confirmed a bipartisan Senate deal for a $1.2 trillion infrastructure plan. Furthermore, after market closed it was confirmed that banks had passed the Fed’s stress tests which paves the way for more buybacks – another pillar of support for equity markets.

The Nasdaq 100 rose 0.64% (and up 2.25% WTD) and hit a fresh record high, although take note of the bearish pinbar whilst RSI (2) hit an overbought level of 94.3 which warns of near-term exhaustion. The S&P 500 rose 0.58% (2.4% WTD) and also closed to a record high without a reversal candle and RSI (2) is not yet overbought at 85.7. 9 of its 11 sectors closed in the green led by the financial sector. The S&P 600 small cap index was the strongest mover, up 1.6% (4.7% WTD) and the Nasdaq bank index rose 1.5% (5.1% WTD).

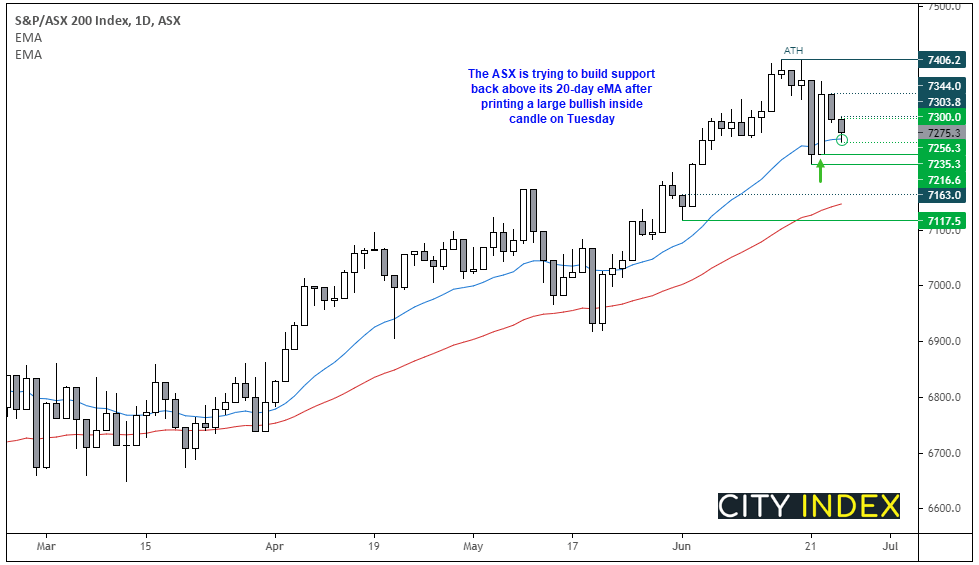

Futures market point to a positive open across Asia, so we may see this spill over to the ASX 200 and break its two-day losing streak. Tuesday’s large bullish inside day shows support at 7235.30, although notice that yesterday’s lower wick found support at the 20-day eMA, so as long as prices don’t drop too sharply earlier in today’s session we would seek a break above 7303.8 to suggest bullish continuation and bring 7344 resistance into view. Ultimately, our bias remains bullish above 7235.30.

ASX 200 Market Internals:

ASX 200: 7275.3 (-0.32%), 24 June 2021

- Information Technology (2.07%) was the strongest sector and Healthcare (-1.8%) was the weakest

- 4 out of the 11 sectors outperformed the index

- 90 (45.00%) stocks advanced, 97 (48.50%) stocks declined

- 9 hit a new 52-week high, 2 hit a new 52-week low

- 74.5% of stocks closed above their 200-day average

- 65% of stocks closed above their 50-day average

- 60% of stocks closed above their 20-day average

Outperformers:

- + 7.1% - Redbubble Ltd (RBL.AX)

- + 6.9% - Pro Medicus Ltd (PME.AX)

- + 6.2% - Afterpay Ltd (APT.AX)

Underperformers:

- -11.2% - Northern Star Resources Ltd (NST.AX)

- -3.69% - Boral Ltd (BLD.AX)

- -3.63% - Charter Hall Group (CHC.AX)

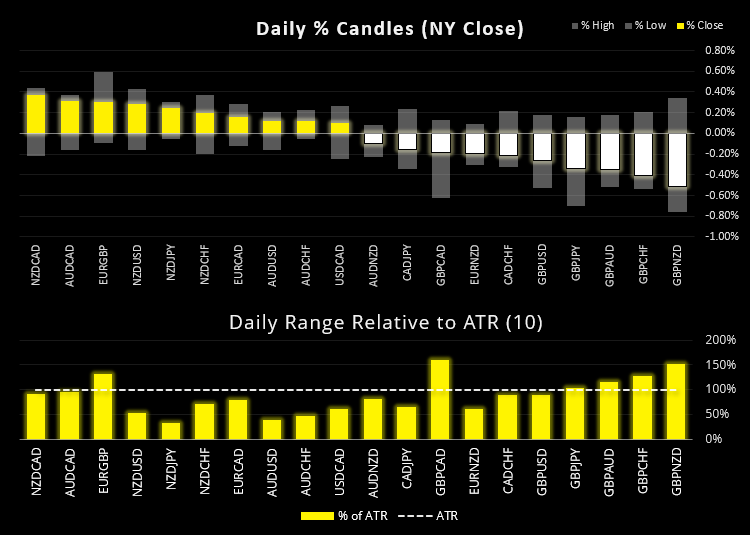

Forex: GBP weakest major following dovish BOE

The British pound accounted for the baulk of overnight volatility after the BOE (Bank of England) were more dovish than expected. The summary of the minutes included “transitory” eight times and “temporary” 11 times regarding inflation, stamp duty and economic data in general, so they don’t appear on track to make any rash decisions, especially now the Fed are keeping rates low and sticking to their transitory guns (even if only temporarily… pun intended).

GBP was broadly weaker, five pairs were the weakest currency pairs of the 28 major and crosses we track, and 6 of their daily ranges exceeded their ATR (10). GBP)/JPY produced a bearish outside day and closed firmly back inside its 9-week range after a one-day hiatus above it. GBP/USD printed a bearish engulfing candle after topping out at 1.4000 the prior day and quickly fell to (and later beyond) our bearish downside target presented ahead of the meeting.

The US dollar index (DXY) printed a small Doji (inside candle) to show volatility remains capped ahead of CPI data tonight. We therefore expect to be in for a quiet Asian session due to lack of top-tier data scheduled for currency markets.

Learn how to trade forex

Commodities in holding patterns ahead of key inflation data:

Oil prices held just below their near-three year highs with WTI effectively closing flat. Prices remain supported following drawdowns in US inventories and improved economic activity for Germany.

Spot gold printed another bearish hammer, although this was a bearish inside day. Silver printed a small bullish hammer (also an inside day). It basically shows a reluctance to break higher, yet volatility is likely caped ahead of today’s Core PCE print from the US.

A hanging man candle (inverted hammer) formed below 4.450 resistance, breaking a three-day rally. Resistance levels to monitor include 4.395 (20 and 50-day eMA cross) and 4.4350 (previous support).

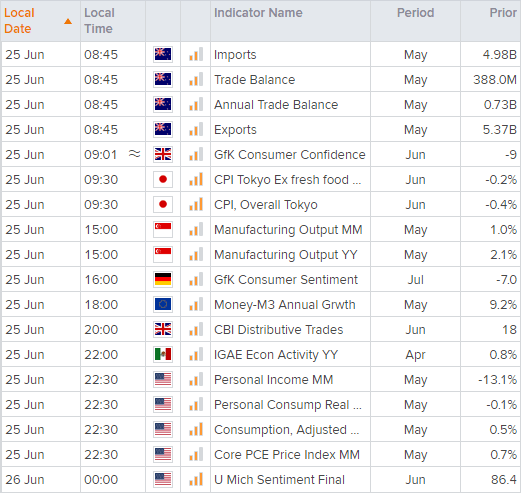

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Today 08:33 AM

Latest ASX articles

April 16, 2024 10:19 PM

April 10, 2024 11:24 PM

April 9, 2024 11:02 PM