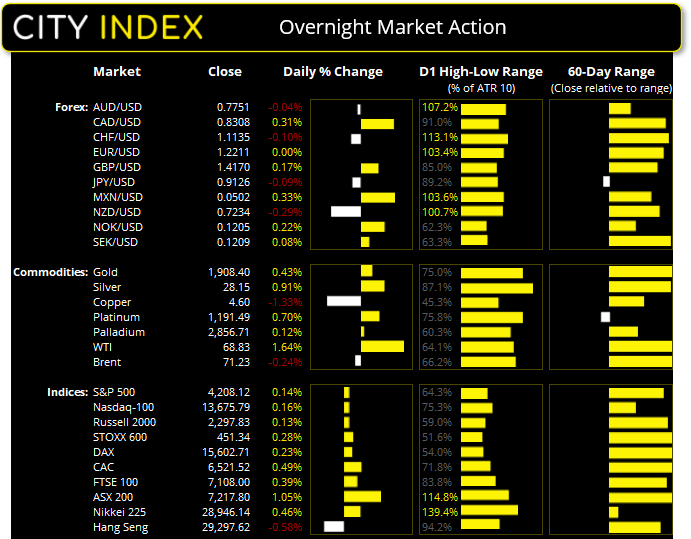

Wall Street posted minor gains and European bourses hovered near their highs during a mildly positive session ahead of tomorrow’s Nonfarm payroll report.

Asian Futures:

- Australia's ASX 200 futures are up 16 points (0.22%), the cash market is currently estimated to open at 7,233.80

- Japan's Nikkei 225 futures are down -70 points (-0.24%), the cash market is currently estimated to open at 28,876.14

- Hong Kong's Hang Seng futures are up 38 points (0.13%), the cash market is currently estimated to open at 29,335.62

UK and Europe:

- UK's FTSE 100 index rose 27.54 points (0.39%) to close at 7,108.00

- Europe's Euro STOXX 50 index rose 16.75 points (0.41%) to close at 4,088.50

- Germany's DAX index rose 35.35 points (0.23%) to close at 15,602.71

- France's CAC 40 index rose 32.12 points (0.5%) to close at 6,521.52

Wednesday US Close:

- The Dow Jones Industrial rose 25.07 points (0.07%) to close at 34,600.38

- The S&P 500 index rose 6.08 points (0.15%) to close at 4,208.12

- The Nasdaq 100 index rose 21.205 points (0.16%) to close at 13,675.79

Learn how to trade indices

Mildly positive tone on Wall Street:

‘Meme’ stocks lifted Wall Street at yesterday’s open and sentiment remain buoyed ahead of tomorrow’s Nonfarm payrolls report, although volatility was low overall. The Nasdaq rose 0.16%, the S&P was up 0.14% and the Dow Jones rose just 0.07%.

Rising energy and consumer stocks kept European bourses near their highs. The FTSE EUROFORST 100 was up 0.56%, the CAC rose 0.5% and DAX was up 0.23%. The FTSE 100 also rose 0.4% and closed at a three-week high after breaking out of a symmetrical triangle on Tuesday.

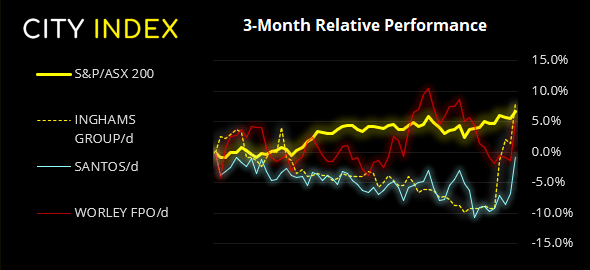

It was a solid close on the ASX 200 yesterday, rising over 1% and closing to a fresh record high after breaking above Tuesday’s hammer just after the open. Our initial target of 7200 has been breached and now 7300 is in focus. Levels for bulls to defend today are 7200 (but we wouldn’t be surprised to see this give way, as the index only closed just above it), 7187 – 7192 and 7163 – 7171.

ASX 200 Market Internals:

ASX 200: 7217 (1.05%), 03 June 2021

- 9 out of the 11 sectors closed higher

- 7 out of the 11 sectors outperformed the index

- 144 (72.00%) stocks advanced, 47 (23.50%) stocks declined

- 72% of stocks closed above their 200-day average

- 64% of stocks closed above their 50-day average

- 79% of stocks closed above their 20-day average

Outperformers:

- + 6.55% - Inghams Group Ltd (ING.AX)

- + 6.51% - Santos Ltd (STO.AX)

- + 6.47% - Worley Ltd (WOR.AX)

Underperformers:

- -4.72% - Megaport Ltd (MP1.AX)

- -3.52% - Nanosonics Ltd (NAN.AX)

- -3.01% - Regis Resources Ltd (RRL.AX)

Forex: CAD remains firm ahead of employment data

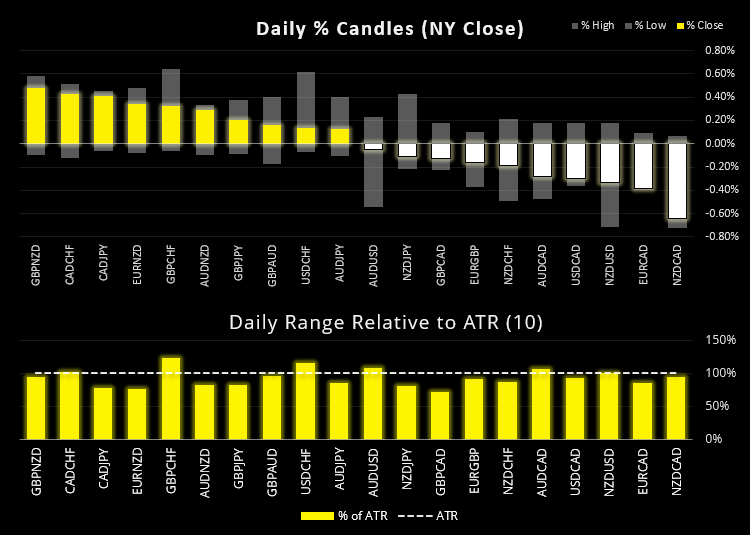

The US dollar index (DXY) continues to behave as we feared; plenty of chop but not real commitment to a direction on a daily basis. It remains trapped between 89.50 and 90.40, although its daily close range over the past four has been just 0.23 points as it meanders around 90.0. In a nutshell it acts as a reminder to not hold onto positions for too long and seek smaller moves over a day or session’s period. And this may be a trend that persists for a whilst longer as we head into the summer months.

AUD/NZD reached our initial bullish target around the 1.0700 handle, although any plans to consider switching to a short bias (for a swing trade) are now in ice given the strength of the rally from 1.0600 to 1.0700. Stronger-than-expected GDP data for Australia yesterday, despite Melbourne extending its lockdown as made AUD relatively attractive against NZD these past 24hours.

The Canadian dollar was the strongest major overnight, supported by higher oil prices following Tuesday’s OPEC meeting. There’s also hopes tomorrow’s employment report will be strong. And, whilst we’re at it, the Canadian dollar is the strongest major currency in Q2 (+4.8%) and year-to-date (+6.1%). Over this same period brent has risen +13.6% in Q2 and +37.5% YTD.

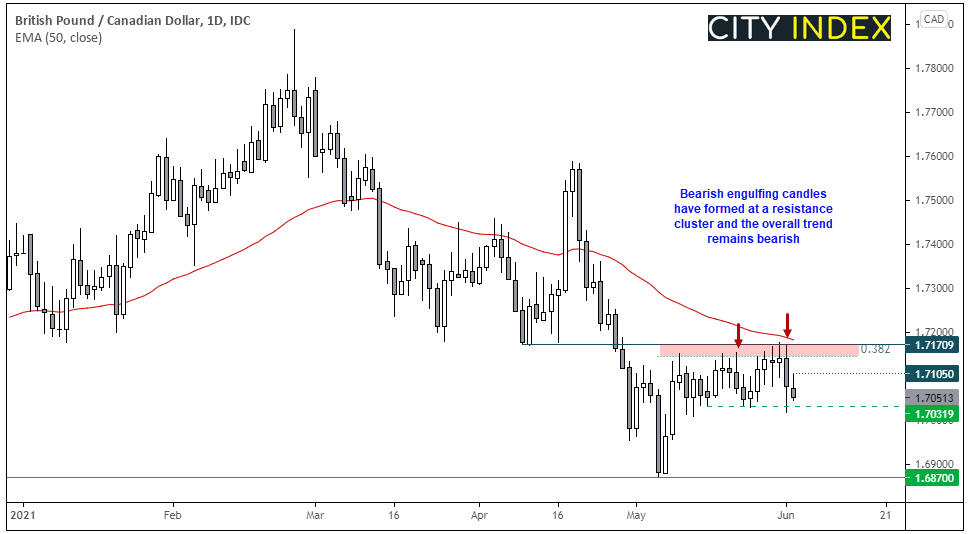

GBP/CAD ready to top?

It’s time to catch up on GBP/NZD, which we initially explored back on the 24th May after a bearish engulfing candle formed at a key resistance zone. The downside never really took off and it has since re-tested the resistance zone, but price action is again suggesting the market is trying to top out. An even larger bearish engulfing/outside candle has formed at 1.7170 resistance following Tuesday’s OPEC meeting, and yesterday’s high found resistance just below the midpoint of Tuesday’s range to leave a lower high on the four-hour chart. Given sentiment for GBP is at risk of souring (should Boris Johnson throw in the towel and officially retract reopening plans) and employment data for Canada tomorrow is strong, GBP/CAD could become a bears picnic heading into the weekend. Our core view remains bearish below 1.7170, a more aggressive bear could use yesterday’s high of 1.7105 to aid with risk management.

Learn how to trade forex

Commodities: Oil prices continue to rally

Oil prices continued to climb overnight, seeing WTI futures rise to 68.80 and brent to 71.26, their highest levels since May 2019. Data from API (American Petroleum Institute) showed an increase in demand with crude stockpiles falling by -5.4 million barrels. Iran nuclear deal continues to move at a snails pace which has lowered expectations of an oversupply of Iranian oil. Furthermore, OPEC decided to stick to their plan of gradually removing supply cuts, all of which are supportive of oil prices as global lockdown restrictions are eased.

Gold rose to 1908, its highest daily close in nearly five months as US yields edged lower. Support has been found around its 50-bar eMA on the daily chart and above 18.90 ahead of inflation outlook data.

Silver prices recovered some lost ground within its bullish channel after a minor breach beneath its lower trend channel to close above 28.0 for the first day in two weeks. Although the level it could really do with closing above it the Feb 23rd high at 28.32, as two previous attempts to do just that have resulted in bearish hammers on the daily chart.

Up Next (Times in AEST)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

Latest market news

Latest Indices articles

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM