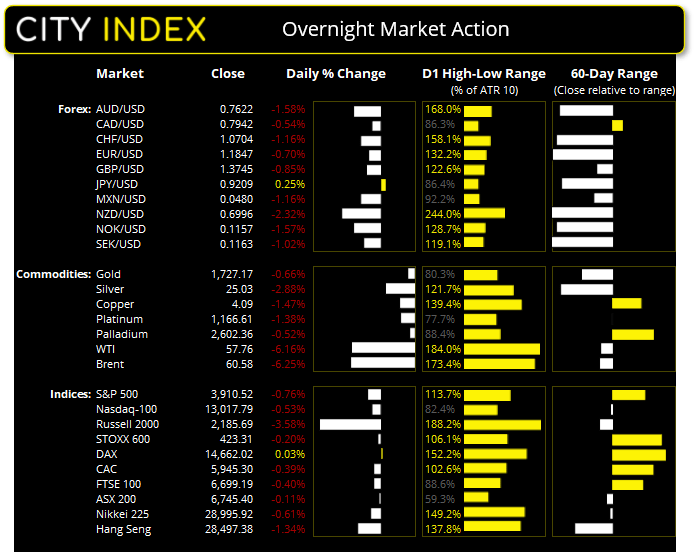

Asian Futures:

- Australia's ASX 200 futures are down -20 points (-0.15%), the cash market is currently estimated to open at 6,725.40

- Japan's Nikkei 225 futures are down -180 points (-0.62%), the cash market is currently estimated to open at 28,815.92

- Hong Kong's Hang Seng futures are down -49 points (-0.17%), the cash market is currently estimated to open at 28,448.38

UK and Europe:

- The UK's FTSE 100 futures are down -61.5 points (-0.92%)

- Euro STOXX 50 futures are down -25 points (-0.66%)

- Germany's DAX futures are down -48 points (-0.33%)

Tuesday US Close:

- The Dow Jones Industrial fell 308.5 points (-0.94%) to close at 32,423.15

- The S&P 500 index fell -30.07 points (-0.77%) to close at 3,910.52

- The Nasdaq 100 index fell -68.724 points (-0.53%) to close at 13,017.79

Indices: Small caps lead Wall Street’s decline

Wall Street was broadly lower overnight as investors weighed up the true cost of Biden’s new $3 trillion spending bill and the resurgence of coronavirus cases. With parts of Europe re-entering lockdowns and daily global COVID-19 rising to around 500k from 260k in six weeks, the great recovery is clearly not out of the woods (and Biden’s $1.9 trillion stimulus package is clearly old news).

Small cap stocks led Wall Street’s declines overnight, with the Russell 2,000 falling -3.5% during its worst session in a month. We had outlined the potential for further gains, provided prices broken above Friday’s high first. But that died a quick death as prices instead crashed beneath the cluster of support levels to signal a deeper retracement against the dominant, bullish trend. Now trading beneath its 50-day eMA with an opening Marabuzo candle (a large candle which opens at the high of the day and produced a small lower wick) sentiment is clearly unravelling for the little guys.

The Dow Jones was off just under -1% and closed beneath it’s 20-day eMA for the first day in thirteen. The S&P 500 (-0.76%) and Nasdaq 100 (-0.5%) held up relatively well as they both remained above their 10 and 20-day eMA’s.

The ASX 200 is set to open lower, within the lower third of its 6650 – 6850 range. Until we see a clear break either side of these areas then range trading strategies are favoured.

Learn how to trade indices.

Forex: NZD is where the volatility was at

If you wanted volatility then the New Zealand dollar and Australian dollar were where it was at yesterday. NZD/JPY was by far the worst performer with a -2.5% and its daily range was nearly 300% of its 10-day ATR (10-day average). In fact, all NZD pairs exceeded their ATR’s.

AUD and NZD extended losses through the European and US sessions, having already led the way lower during yesterday’s Asian session. The rise of COVID-19 cases weighed broadly on risk, making antipodean currencies the punching bag of the session and NZD was under the added pressure of macroprudential tools being reimplemented, which is seen as a net-negative for growth prospects.

- NZD/USD (0.6995) plunged -2.2% during its single worst session since the depth of the pandemic last March.

- EUR/NZD rallied over 1.6% and hit the lower bound of our 1.6950 – 1.7000 target.

- NZD/CAD finally broke out of its sideways congestion around its 200-day eMA and hit the upper bound of our 0.7853 – 0.8800 target.

- AUD/USD (0.7745) fell -1.6% and is now probing 0.7622 support.

Whilst NZD pairs show the potential to extend losses, the magnitude of losses overnight make it tricky to enter whilst achieving an adequate reward to risk ratio. Therefore, bears may want to consider very low holding times (timeframes) to try and stick with momentum. But traders of the daily chart may want to look elsewhere or wait for a period of consolidation / retracement.

The US dollar index (DXY) closed to a 2-week high and posted its most bullish session in thirteen. With momentum trying to break further away above its 20-day eMA, bulls may be interest in any dips above 92.03 – 92.16 support.

Learn how to trade Forex

Commodities: Bears drive oil and gold lower

Demand concerns continued to weigh on oil prices which broke to fresh lows overnight as bears regained control of momentum. WTI now trades at a 5-week low around $56.00 having shed a further -6.5%, bringing its losses to around -15.7% in just over two weeks. Brent now trades around $60.55 and close to a 4-week low having shed -13.7% in seven sessions.

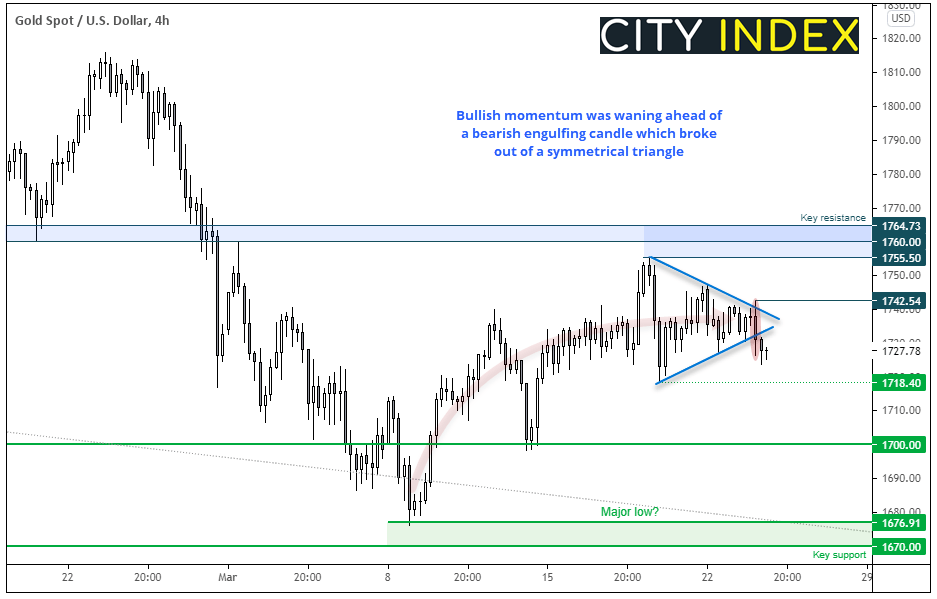

Not wanting to miss out, gold also turned to a 4-day low, although volatility was kept in check relative the calamity elsewhere. Bullish momentum since the 1767 low is waning and bulls failed to break higher from a symmetrical triangle. In fact, a bearish outside candle confirmed a false initial break with an eventual break lower. So, with sentiment down and Asian markets set to open we cannot rule out further losses for the precious yellow metal.

- The near-term bias remains bearish below 1742.54 with next major support sitting at 1700.

- Bears could consider fading into minor rallies beneath 1742.54, using 1720 as in interim target.

- A break above 1742 brings the 1755 high into focus but we’d prefer to wait for a break above 1760 – 1764 before reconsidering bullish setups on the daily chart.

Palladium produced a bearish inside day following Monday’s bullish hammer. Our bias remains bullish above the 2514 breakout level although bears may want to check for a break above Monday’s high as it could suggest momentum is realigning itself with last week’s breakout.

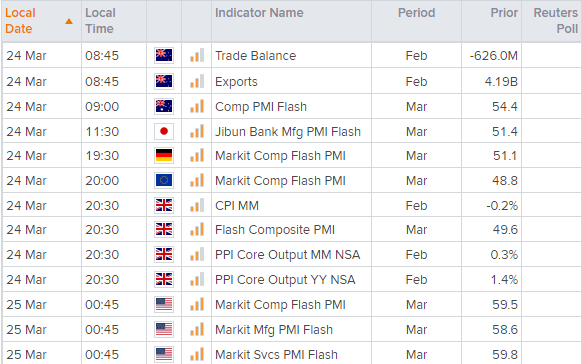

Up Next (Times in AEDT)

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

The main theme connecting them all is flash PMI (purchase manufacturer’s index) for Australia, Japan, Eurozone (and each country) UK and of course the US. As these are preliminary releases and leading indicators they can generate higher levels of volatility.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM