Asian Futures:

- Australia's ASX 200 futures are up 18 points (0.27%), the cash market is currently estimated to open at 6,789.20

- Australia's ASX 200 futures are up 180 points (0.62%), the cash market is currently estimated to open at 29,207.94

- Australia's ASX 200 futures are up 337 points (1.17%), the cash market is currently estimated to open at 29,110.23

UK and Europe:

- The UK's FTSE 100 futures are up 3 points (0.04%)

- Euro STOXX 50 futures are up 22 points (0.58%)

- Germany's DAX futures are up 48 points (0.33%)

Tuesday US Close:

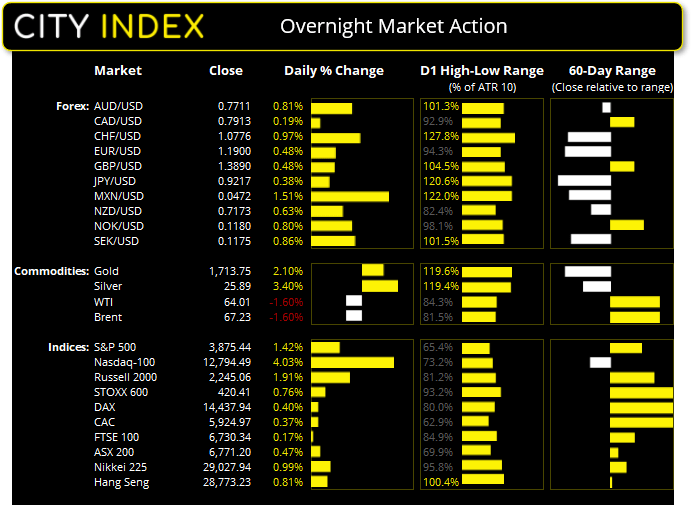

- The Dow Jones Industrial rose 30.3 points (0.1%) to close at 31,832.74

- The S&P 500 index rose 54.09 points (1.42%) to close at 3,875.44

- The Nasdaq 100 index rose 495.411 points (4.03%) to close at 12,794.49

A successful 3-year bond auction overnight enticed investors to buy bonds across the curve and send yields lower, in turn giving sentiment on Wall Street a lift and sending indices higher. OECD’s upgrade to global and US growth also played its part. The US 10-year yield fell to 1.54% and the 30-year is now down to 2.25%.

Wall Street was quick to take note, which saw technology stocks lead the rebound and the Nasdaq 100 post an impressive 4.4% gain. This also means that the close above the 12,758 ‘neckline’ invalidates the bearish head and shoulders pattern on the daily chart, although price action remains in a tight bearish channel. A break above 13,300 is required before we can assume bullish continuation on the daily chart.

The Russell 2000 rallied over 2% to take second place, the S&P 500 was up 1.9% and the Dow Jones rose 0.17%.

As for Europe, the DAX (0.4%) extended its reach to a new record high after breaking above key resistance on Monday. The STOXX 600 rose 0.76%, the STOXX 50 was up 0.6% whilst the CAC posted a 0.37% gain.

The ASX 200 is expected to open slightly higher around 6771.02 today.

Forex: Did the dollar go too far, too soon?

DXY fell -0.4%, its most bearish session in four weeks and produced a bearish engulfing candle. At current levels the weekly chart is on track for a bearish pinbar. The initial impressions suggest the dollar has entered a corrective phase which should allow for the unwind of recent moves, but we do not yet think we have seen the high of the dollar.

- All majors were higher against the USD, with AUD, CHF and NZD leading the rebound. Whilst AUD and NZD highlighted the risk-on tone to the session, the Swiss franc made a notable rebound as USD/CHF bullish bets were quickly reversed following such a solid rise over recent sessions.

- USD/CHF stalled at the June 2020 low (to the pip) and mirrors price action on DXY. Next major support for USD/CHF is around 0.9200, making it a viable counter-trend target or likely support level for bullish dip buyers.

- NZD/USD has rebounded from key support at 0.7096, helped higher by RBNZ announcing they will remove some of the temporary liquidity facilities implemented in response to the COVID-19 pandemic. Yet 0.9200 continues to cap as resistance

- EUR/USD rebounded from its 200-day eMA and weekly S1 pivot, as warned in yesterday’s European market report. There is the potential for further upside as part of its corrective phase but we remains bearish whilst prices remain beneath the 1.2000 barrier, with the 1.1952 high also likely to cap gains initially at least.

- USD/CNH also produced a bearish outside day and fell back to the original breakout level of 0.6515. Whilst our bullish bias over the near-term has been side-lined, we remain convinced we have seen a multi-month low.

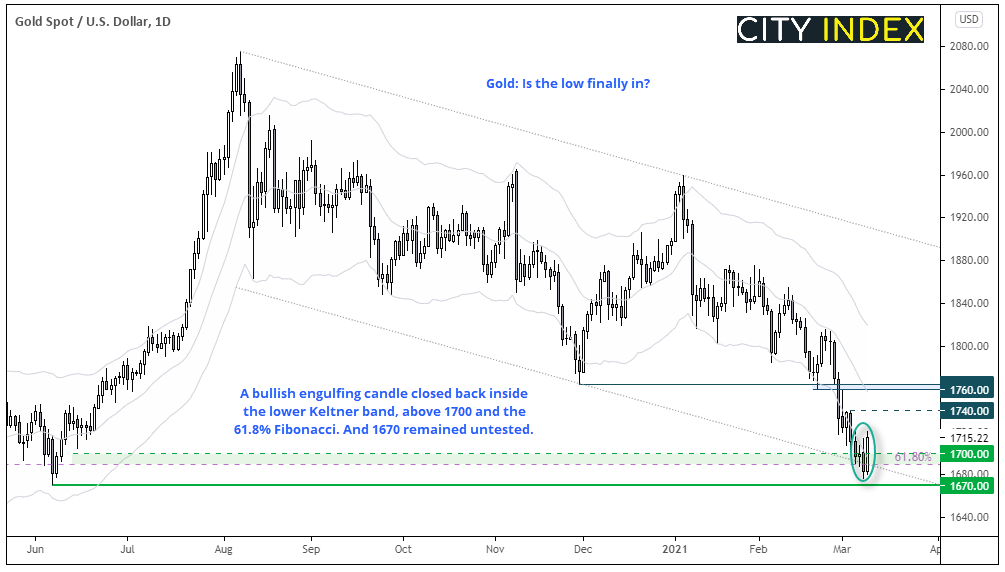

Commodities: Gold bugs fight back

Bulls have regrouped and regained strength after an all-too-easy break below 1700 on Monday. 1670 held as support (and was in fact untested) and gold now sits at a 3-day high above 1700 with a bullish engulfing day.

That we have seen a false break beneath the lower channel, reversal back above the lower Keltner band and 1670 support remain untested suggests the low could finally be in place.

- Bulls could seek bullish setups above 1700

- 1740 and 1760 are now bullish (counter-trend) targets

- Further out, we’ll monitor gold’s potential to top around 1760 for swing trade shorts. Whilst a break above 1760 suggests we may have seen the end of the correction from the all-time high

- A break below 1670 signals a deeper correction from its all-time high

Elsewhere in commodities, silver also posted a bullish outside day also has found resistance around $26, where the 10, 20 and 50-day eMA’s reside. Platinum is also perking up after a correction from recent highs, but the 10- and 20-day eMA’s are capping as resistance. WTI and Brent trade lower for a second consecutive session as part of a much-needed correction after posting solid returns over recent weeks and months.

The OECD raised growth forecasts for 2021

The OECD (Organisation for Economic Co-operation and Development) raised their forecast for global growth to 5.6% from 4.2% for 2021. And, thanks to the ginormous stimulus package, US growth has been upwardly revised to 6.5% from 3.2% previously. The Eurozone also received a modest upgrade to 3.9% from 3.6% and the UK’s has been raise to 5.1% from 4.2% previously.

Separately, Eurozone’s Q4 GDP was downwardly revised to -0.7% QoQ versus -0.6% previous. Germany’s exports rose 1.4% in January, so much better than the -1.2% forecast. Imports however fell -4.7% allowing the trade surplus to rise to 22.2 billion versus 16.4 billion forecast.

You can view all the scheduled events for today using our economic calendar, and keep up to date with the latest market news and analysis here.

- At 09:00 AEDT RBA Governor Dr Philip Lowe is scheduled to speak at the Australian Financial Review business summit.

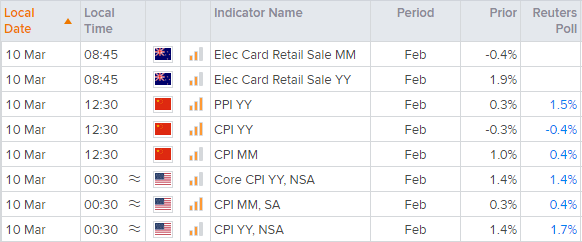

- Inflation data for China and the US are the main economic calendar events for today. Production prices are expected to have risen by 1.5% YoY for China in February, an CPI to rise by 0.4% Mom in February compared to 1% in January.

Latest market news

Yesterday 08:33 AM

Latest Gold articles

April 1, 2024 01:09 PM

March 28, 2024 10:30 AM

March 26, 2024 11:24 PM

March 26, 2024 12:00 PM